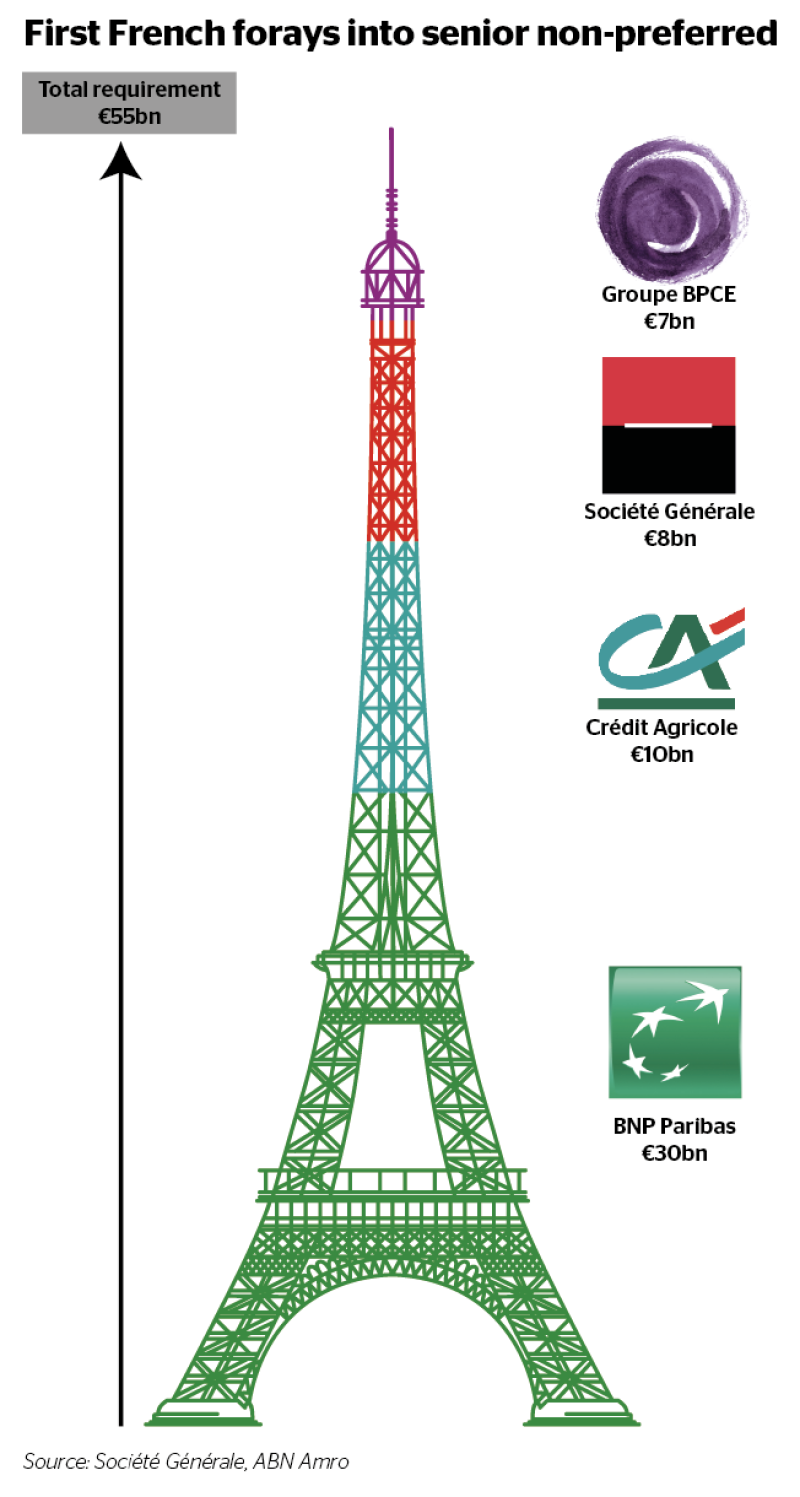

The creation of senior non-preferred debt in France means the country’s financial institutions can really start to build their loss-absorbing debt levels towards their requirements for total loss-absorbing capacity (TLAC) rules and Europe’s minimum requirement for own funds and eligible liabilities. But how much does each bank need to issue over the coming years?

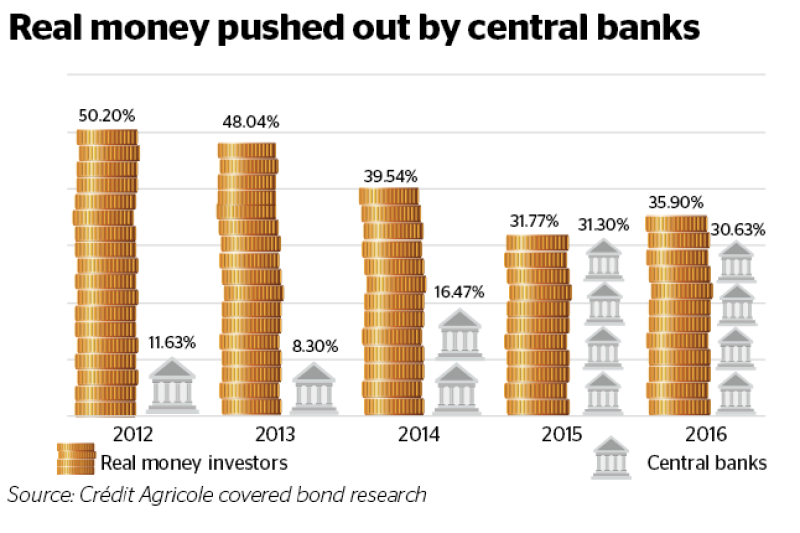

Since October 2014 the European Central Bank has been steadily buying more securities eligible for its covered bond purchase programme, helping issuers command much tighter pricing for new transactions. The resulting change in distribution by covered bond investor type has been stark. Real money investors — including asset managers and investors — have been squeezed out in the new pricing environment, while central banks have ramped up their purchases.

Amid tight budgetary conditions, including persistent inflation, volatile markets and geopolitical tensions, sovereign issuers in the EU face continuous pressure to fulfil borrowing requirements. Simultaneously, these same issuers are having to confront different challenges that range from the growing impact of hedge funds in their order books, and whether this is a good or a bad thing, how to convince new investors that their home currency, the euro, is an alternative to the dollar and how aligned EU capital markets should become and what form this should take. GlobalCapital assembled sovereign debt issuers to discuss borrowing requirements and how they are being met, what the diversification of their investor bases means for the products they offer and the benefits of harmonisation and simpler regulation in the EU.