UK

-

There are fundamental reasons for UK assets to be revalued upwards, analysts believe. The powerful majority achieved by Boris Johnson's Conservatives tilts the UK towards a Trump-like market-friendly, fiscally generous patch. But the reality of Brexit cannot be ignored for long.

There are fundamental reasons for UK assets to be revalued upwards, analysts believe. The powerful majority achieved by Boris Johnson's Conservatives tilts the UK towards a Trump-like market-friendly, fiscally generous patch. But the reality of Brexit cannot be ignored for long. -

The solid victory for the Conservative Party in the UK election has given investors a burst of confidence. But the rise in rates has proved short-lived and is unlikely to spark any supranational, sovereign and agency sterling issuance. Meanwhile, the outlook for the Bank of England has become slightly more hawkish.

-

Nerves in the foreign exchange market had been tense in the run-up to Thursday night’s UK election, with a rumour that Labour would win more seats than predicted sparking some volatility in the FX options market. But that was swiftly quashed when TV broadcasters’ exit poll showed a Conservative majority and brought volatility to a swift halt.

-

There were audible sighs of relief on equity capital markets desks on Friday morning as Boris Johnson delivered a hefty Conservative majority in the UK general election. Bankers are now prepping for a busy 2020 and a solid UK issuance calendar. A state block trade of Royal Bank of Scotland shares is among the most anticipated chunks of business for next year.

-

The Conservative Party’s strong win in Thursday’s general election is thrilling the UK’s financial sector and business world on Friday. Shares in UK banks and house builders — the very domestic sectors seen as most at risk of a hard Brexit or weak UK economy — have soared by 10% and more, while bond yields, especially for banks, have tightened sharply.

-

Capital markets are set for a surge of adrenalin on Friday after Boris Johnson’s Conservative Party secured a thumping majority in the UK’s general election, removing a huge weight of uncertainty about Brexit. With hopes also leaping of a US-China trade deal, government bonds, equities and sterling will all move in a risk-on direction on Friday — the only question is how far.

-

Sterling is set to take a bigger slice of the socially responsible bond market as a result of a number of initiatives, including reforms that are putting the pressure on UK pension funds to focus on environmental, social or governance (ESG) factors in their investments. Burhan Khadbai reports

-

Covered bonds performed well in 2019, but yields finished in negative territory and spreads ended at their tightest for the year. The implication is that, despite higher than expected ECB covered bond purchases and a renewal of its ultra-cheap TLTRO facility, investors will struggle to match 2019’s returns in 2020, writes Bill Thornhill.

-

Navigating the covered bond market will not be without its challenges in 2020. The Targeted Longer Term Refinancing Operation (TLTRO), European Central Bank deposit tiering and the Covered Bond Purchase Programme have collectively distorted the market, but added to this concoction is the impact of negative interest rates. Against this backdrop issuers, investors and investment bankers gathered in Munich in November to discuss the outlook for covered bonds. It is likely that new issue premiums will gradually tighten, but the path is unlikely to be smooth. January is typically the busiest month, but in 2019, issuers that funded this early paid the highest spreads. And, with the ECB expected to buy in the region of €4.5bn covered bonds a month, issuers will not feel compelled to move early. But the ECB monetary policy has unwelcome implications. Covered bonds have begun to lose value against government bonds, and this will extend if the ECB is unable to loosen restrictions on government bond purchases.

-

It was a year when the corporate bond market first had to get used to a world without QE — and then digest its return. Spreads tightened sharply after the summer following the ECB’s decision to restart its Corporate Sector Purchase Programme. But that did not mean all the best deals came after September. Far from it.

-

A rich variety of UK borrowers including a football club, two airports, the City and a clutch of FTSE 250 firms turned to US private placements in 2019. UK local authorities remained absent, but a surprise from the UK Treasury in October may be a game-changer

-

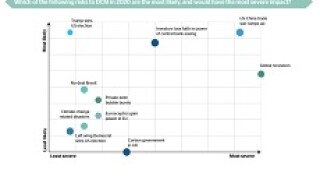

Markets go into 2020 fretting about a global recession and an escalation of tradetensions between the US and China, according to 25 heads of debt capital markets in the EMEA market, in Toby Fildes’ annual outlook survey. Respondents are mildly pessimistic on spreads and fees in the primary markets as well. But on the plus side, bankers are feeling hopeful about sustainability-themed bonds and almost unanimously believe issuance will top $270bn.