Germany

-

Deutsche Kreditbank has mandated leads for its second deal of the year and the third 10 year issued from Germany this year. Meanwhile, there is speculation that several Canadian issuers could return to the euro market.

-

The widely anticipated public sector-backed Pfandbrief from Dexia Kommunalbank on Tuesday had been expected to go well, given the juicy spread that was likely. But the level of oversubscription was the highest of any German deal this year and even put competing issuance from Portugal into the shade.

-

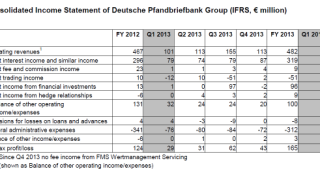

Deutsche Pfandbriefbank (Pbb ) reported a 31% pre-tax rise in profit on Monday, boding well for its privatisation — in marked contrast to Depfa plc. Pbb has launched two Pfandbrief deals this year and is likely to return to markets at least once and possibly twice this year, it confirmed to The Cover on Monday. For the time being, however, the covered bond market is expected to trade sideways as participants await news from the European Central Bank.

Deutsche Pfandbriefbank (Pbb ) reported a 31% pre-tax rise in profit on Monday, boding well for its privatisation — in marked contrast to Depfa plc. Pbb has launched two Pfandbrief deals this year and is likely to return to markets at least once and possibly twice this year, it confirmed to The Cover on Monday. For the time being, however, the covered bond market is expected to trade sideways as participants await news from the European Central Bank. -

Sovereign bond market volatility continued to buffet markets on Thursday and, after the slew of FIG issuance in the last week, there was a degree of supply indigestion. But covered bond bankers did not think there was much to be read into the lacklustre execution of this week’s German and Australian deals. The two issues were solid trades, but for idiosyncratic reasons lacked the sparkle of earlier deals.

-

The prospective amendment to the German Pfandbrief Act to give the German regulator authority over minimum overcollateralization (OC) may prove a credit positive, said Fitch on Tuesday. But the proposals are too thin on detail for any concrete rating action on programmes to be taken.

-

The covered bond market is in danger of losing a swathe of real money investors who have been put off by low returns and declining issuance. But a rich new stream of demand from bank investors looking to fill their liquidity buffers could fill the vacuum in time. However, these buyers should be more interested in looking at the nascent floating rate format and not the fixed rate market that until now has prevailed.

-

After a long string of syndication success stories this year, the covered bond market finally saw some investor pushback on Tuesday when Landesbank Hessen-Thueringen (Helaba) issued a tightly priced two tranche Pfandbrief. The outcome gives ammunition to those that are concerned valuations have become overstretched. However the funding was very cheap, attracted exceptionally strong international demand and was placed with high quality accounts.

-

Landesbank Hessen-Thueringen (Helaba) mandated leads for a dual tranche triple-A rated public sector Pfandbrief on Monday, for launch on Tuesday.

-

Depfa Bank plc will not be sold to an unrated entity, but will be transferred to the German government’s wind-down institution for Hypo Real Estate Holding, FMS Wertmanagement (FMSW). The issuer’s covered bonds tightened by around 60bp on Wednesday from Tuesday’s open as uncertainty over its future was removed.

-

A prospective amendment to the German Pfandbrief Act will give the German regulator the authority to decide on the minimum level of overcollateralisation (OC) that Pfandbriefe issuers require. This will be decided on a case-by-case basis, could well be above the current legal minimum and will give stronger investor protection than private contractual commitments.

-

Depfa ACS covered bonds were unchanged on Thursday as the names of the failed bank’s preferred bidders emerged. The buyer’s strong rating suggests the covered bond rating is safe, and even if a sale is not agreed, the German government’s continued ownership means the rating is protected. As such, the covered bonds which have the highest rating in Ireland, should be trading tighter than all other Irish deals.

-

Credit sentiment is positive, and it seems unlikely that the European Central Bank would take anything other than an accommodative stance at next week’s policy meeting, but bankers are getting cautious that valuations are becoming overstretched, particularly in those markets which have until now been considered safe havens.