“Thanks to globalisation, policy decisions in the US have been largely replaced by global market forces,” said former chair of the Federal Reserve Alan Greenspan, ahead of the 2008 US presidential election.

“National security aside, it hardly makes any difference who will be the next president.”

It is a complacent quote that Adam Tooze, professor of history at Columbia University in New York, likes to use to illustrate how myths have been busted since the crisis.

Politics still shape the markets as much as vice-versa. International relations cannot be separated from finance. Italy is clearly proving this, and the fallout is buffeting the entire EU.

The Five Star Movement and the League formed an unlikely coalition after the country’s inconclusive March election. The former believes in greater wealth redistribution, while the latter has traditionally sought to protect the financial interests of the rich north. But both are united by Euroscepticism, in one of the EU’s founding member states.

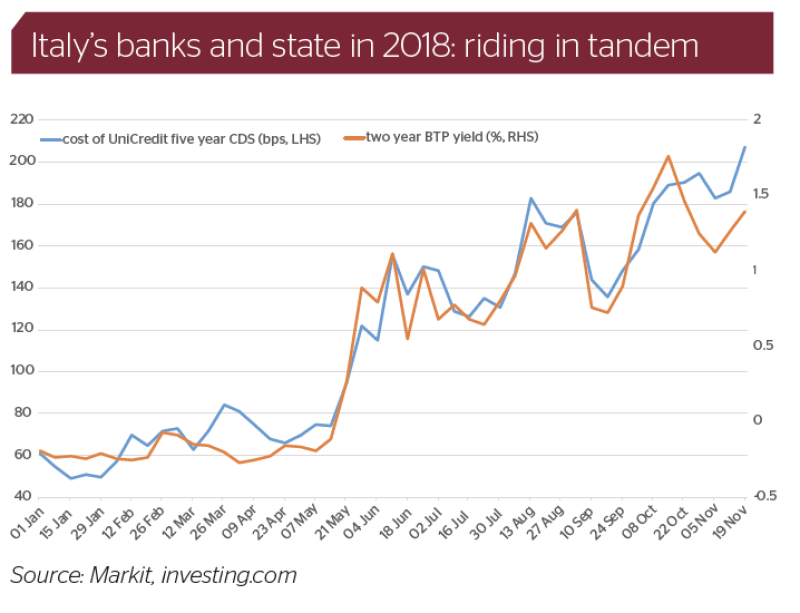

Matters came to a head when Italy’s draft 2019 budget proposed a deficit target of 2.4% of GDP. The European Commission rejected this and the two sides have failed to find a compromise. The conduit for this spat spilling over into the markets has been a jump in BTP spreads and renewed fears about the sovereign-bank doom loop.

For the broader EU, the Italian problem is a symptom, as well as a cause of a lack of progress on integration, notably in ways that would protect against a further financial crisis. A bitter taste of missed opportunity already hangs in the air.

Will politicians get out of their funk before the next crash?

The 2019 Italy crisis?

Italy and the EU head into the new year at loggerheads. The Commission has said an “Excessive Deficit Procedure” is warranted, potentially leading to some kind of disciplinary action.

It is hard to see a political solution in the short term: not much meat can be stripped from the budget without impeding the government’s promises, says Luigi Scazzieri, research fellow at the Centre for European Reform think-tank in London. “My assessment is that this fight will increase,” he says.

More cynically, the League has made political capital out of the deadlock, ahead of European Parliament elections in May.

“The budget is mostly an advertising exercise in the run up to 2019 European elections,” says Alberto Gallo, head of macro strategies at Algebris Investments.

With neither side giving in, the market is getting ever more anxious.

“Large and lasting increases in risk premiums on government securities hinder the reduction in the debt-to-GDP ratio, affect the value of household wealth, curb lending to the private sector and make borrowing more costly, and worsen the liquidity and capital positions of banks and insurance companies,” warned the Bank of Italy at the end of November.

Opinion is divided on how bad the proposed fiscal expansion in Italy would be. Many see low growth as the problem, but this is set against a backdrop of high public debt in a one-size-fits-all eurozone monetary union about to end QE.

“At low rates of growth the arithmetic that underpin the public debt dynamics become extremely sensitive to small changes in bond yields,” says Neil Shearing, group chief economist at Capital Economics, in a note.

For Gallo, the problem is the attitude that the budget conveys. “The budget deficit itself is not a huge number but the issue is that it’s done in an antagonistic way,” he says. “It’s been done without taking into account investors’ reactions.”

Change from within

Some suspect that the EU is more than happy to let bond investors do the dirty work of bashing Italy until it capitulates.

“If the ECB was just acting like an ordinary central bank, and managing Italy’s public debt pile, the possibilities for a crisis would be much moderated,” says Tooze, who published Crashed, a history of the financial crisis, this year.

“It’s because the ECB actually has the option not to intervene that we are in the situation that we are,” he adds.

Early December saw the beginnnings of a potential rapprochement bewteen the two sides. But an awful lot of ground still separates them.

Italian deputy prime minister Matteo Salvini’s calculation may be that the EU will change from within to adopt a more nationalist bent. The election in May will be “a common sense revolution”, he told reporters in October.

His comments look either misguided or misleading. While big traditional parties are losing ground, pro-EU groupings are still set to win more than 60% of seats based on polls, and far from all the other members of parliament would be anti-EU.

More broadly, the proportion of people who think the euro is a good thing for their country is at 64%, its highest level since the Eurobarometer survey on the topic began in 2002.

What’s more, there is no indication how, once inside the gates, the different barbarians might work together to forge a new Europe. Nationalists tend to dislike cross-country co-operation, after all.

Policies that Italy might want, such as greater sharing of refugees arriving on its coasts and loosening budgetary restrictions, would be resisted by the hard right in northern Europe.

So the nationalists are unlikely to change Europe’s direction. But they can press down on the brakes, including when it comes to initiatives to make Europe more financially and economically resilient.

Negative feedback loop

And this is of upmost importance to investors.

“When thinking about the outlook for Europe’s economy, we should focus less on the latest quarterly growth numbers that are grabbing the headlines and more on the structural challenges that remain at the heart of the eurozone,” says Shearing.

The banking union is regarded as key in making the eurozone more crisis-proof. It could also lead to more cross-border private sector integration, in the form of bank M&A.

The overarching framework has taken great steps when it comes to supervising and resolving banks. But it has floundered on the issues of reducing and sharing risk: diminishing it through cleaning banks’ balance sheets and distributing it through a European deposit insurance scheme (EDIS).

Italy’s current financial stress is a result of the inability to complete the Banking Union: under the sovereign-bank doom loop, the nation state guarantees banks’ deposits and the lenders hold large amounts of government exposure. The credit quality of both weakens in tandem in a vicious cycle.

That stress will also hinder progress. Thanks to the new government, other countries will trust Italy less on risk reduction. “It’s not going to be perceived as serious,” says Scazzieri.

The increased riskiness of the banks will also deter neighbours from embracing EDIS.

“We’re caught in a dangerous half-way house which continually reaffirms the unwillingness of the northern side to engage in more risk-sharing,” says Tooze.

Another blunted policy initiative is French president Emmanuel Macron’s common eurozone budget. This could have supported countries hit by crisis, for example through targeted investment or benefits. He had floated a size of several percentage points of the eurozone’s €11.2tr GDP.

But this is set to be heavily diluted. The latest proposal is to incorporate it as part of the EU budget, and German chancellor Angela Merkel has suggested a size in the tens of billions instead.

BBC Europe

A group of directors and fellows at think-tank Bruegel in Brussels have proposed a different direction of travel to deal with tensions over integration.

In a “bare bones-plus club” (BBC) Europe, all member states would stick to a common base: a treaty framework, council, commission, parliament and court. But beyond this, they could sign up to four additional groups, relating to: economic and monetary union; migration, asylum and Schengen; security and foreign policy arrangements; and any other policy areas.

But economic and monetary policy, which includes the banking union, cannot easily be separated from other areas.

Other world powers combine foreign and economic policy, say Silvia Merler, Simone Tagliapietra and Alessio Terzi, also fellows at Bruegel. US president Donald Trump uses tariffs and sanctions as foreign policy tools. China’s Belt and Road Initiative is both a project of finance and of international relations.

The EU itself is mixing together environmental and finance policy through measures to boost green investments.

“Failing to recognise that policies cannot be easily compartmentalised, a ‘BBC EU’ would likely be even more unprepared for… challenges and get the short end of the stick,” say Merler and co.

This suggests that the markets must judge the EU’s political unity. And one question jumps out: is the recent bout of nationalism as much of a threat to Europe as the pro-Europeans in the north who refuse to put their money where their mouths are?

“I don’t think the Euroscepticism that is now very visible is really all that new,” says Tooze. “The problem is the old one of a lack of comprehension, will and vision in the mainstream.”

In this light, investors should focus on how the governing Christian Democratic Union in Germany moves on Europe after Merkel steps down.

“The next financial crisis probably is not coming tomorrow so the question is how much time do we have and do politicians have the right sense of urgency,” says Gallo.

The clock is ticking.