Spain

-

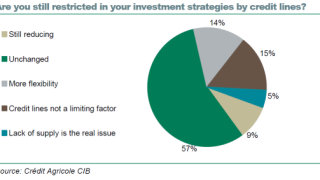

Investor sentiment towards Spain and Italy has improved since August, according to a Crédit Agricole survey. However, most buyers’ credit lines are unchanged, which means many still cannot take advantage of remarkable relative value.

Investor sentiment towards Spain and Italy has improved since August, according to a Crédit Agricole survey. However, most buyers’ credit lines are unchanged, which means many still cannot take advantage of remarkable relative value. -

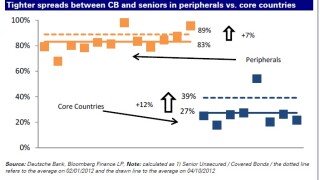

Core covered bonds are performing poorly, with low coupons putting investors off, according to Deutsche Bank analysts. Higher yielding peripheral paper could benefit as a result, but the prospect for fresh benchmark trades from southern Europe remains uncertain.

-

Investors are cash-rich and covered bond spreads look set to remain fairly stable – ideal conditions for covered bond issuance. However, deal flow is set to remain quiet as most issuers are well funded, and those that could do deals are about to enter blackout period.

-

Nearly a quarter of Spanish mortgages could be in negative equity, Moody’s has warned, but with Cédulas collateral marked at historic levels, investors have little transparency on the value of their claim. An updated covered bond structure is fully warranted, but unless it was legally enshrined, the benefit would be negligible, reports The Cover.

-

Banco Santander Totta got only a derisory take up for its RMBS to covered bond exchange — the first time a bank has offered such a swap. Meanwhile, analysts and lawyers dashed hopes for the tendering of low priced Spanish multi-Cédulas, saying that such exercises would be technically infeasible.

-

The transfer of assets to the proposed Spanish Asset Management Company (AMC) could hit Cédulas noteholders, as it would reduce overcollateralisation. However, as issuer defaults would become less likely, covered bondholders would stand to benefit.

-

Norddeutsche Landesbank could open books on a debut dollar covered bond as early as Tuesday morning, said syndicate leads on Monday. But the outlook for a first sterling trade from Deutsche Pfandbriefbank is more uncertain.

-

Despite growing concerns that a Spanish bad bank will cause collateral pools to shrink, there is a growing sense of confidence that real money Cédulas investors will not become forced sellers as bonds hold the investment grade rating threshold and the ECB dampens systemic risk fears.

-

Markit is expected to unveil a new tradable liquid covered bond index in October or November. Though it may not necessarily be actively traded, it should provide a more useful measure than the existing index, as it will help investors to gauge more closely their performance in relation to the most relevant parts of the covered bond market.

-

Deutsche Hypothekenbank Hannover mandated for its second benchmark covered bond of the year on Monday. The borrower is expected to price the seven year mortgage backed trade on Tuesday, taking the number of deals in that maturity year to date to almost double that of 2011.

-

Spain’s CaixaBank launched a novel covered bond tender offer on Friday. The borrower will buy back at par up to €2.11bn of floating rate bonds from retail clients but participating bondholders must keep the funds in a new deposit account for at least a year after the exchange.

-

Sampo Housing Loan Bank on Wednesday mandated for the sixth seven year covered bond benchmark of September, and should price the trade on Thursday. Despite a renewed appetite for risk in the wider market, covered bond supply remains consigned to safer names, but a successful auction for the Spanish sovereign could pave the way for further Cédulas.