Spain

-

Deutsche Genossenschafts-Hypothekenbank has hired banks for a mortgage Pfandbrief, which is pencilled in for Tuesday. It may have company from Commerzbank, which The Cover understands is also eyeing Tuesday for Europe’s first ever SME structured covered bond.

-

Standard and Poor’s announced on Thursday that it had revised its categorisation of all Spanish covered bond programmes from Category 1 to Category 2, thereby lowering the maximum rating uplift between an issuer and its covered bond programme from seven notches to six.

Standard and Poor’s announced on Thursday that it had revised its categorisation of all Spanish covered bond programmes from Category 1 to Category 2, thereby lowering the maximum rating uplift between an issuer and its covered bond programme from seven notches to six. -

Issuers looking for rehabilitation in the capital markets and wanting to wean themselves off central bank funding must be careful to ensure they issue strategic deals that have a high chance of performing. This should lower their long term cost of funding and enable greater market access.

-

After three senior euro bond issues this year, BBVA this week chose to extend the duration of its liabilities with the issuance of its first covered bond of the year. At 100bp through the sovereign, BBVA was the first Spanish bank to borrow significantly cheaper than the government. However, at €2bn the deal size was too large and led to a dismal secondary market performance.

-

BBVA’s surprise five year follows a pattern set by Intesa and suggests that other issuers, such as Banco Santander or Caixa Geral de Depósitos, could look to extend the duration of their funding with a covered bond.

-

BBVA has become the first Spanish borrower to smash through the sovereign floor with the imminent pricing of its five year Cédulas Hipotecarias. The deal follows last week’s impressive funding from Intesa Sanpaolo and illustrates the continuing bid for higher yielding secured debt.

-

Spain’s government was due to pass a decree on Thursday that would suspend evictions of homeowners in financial difficulty, as the country works on changes to its mortgage law. The effect on Cédulas performance is likely to be limited, however, given the low threshold for assistance.

-

Standard & Poor’s has cut BNP Paribas ratings and lowered its outlook on four other French covered bonds issuers because of rising risk in the French banking system. Meanwhile, Moody’s downgraded CIF Euromortgage’s covered bonds after taking the same action on the issuer.

-

Banca Monte Dei Paschi di Siena’s secondary covered bond spreads are holding firm following another downgrade, but Spanish spreads are weakening after their recent rally. Peripheral borrowers could still bring successful benchmarks, but compression between covered and senior levels means there is less incentive to use valuable collateral, syndicate bankers told The Cover.

-

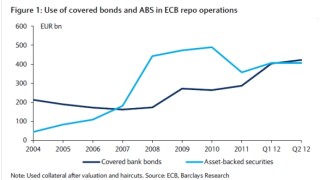

The increase in retained issuance will have a lasting impact on the primary covered bond market and could reduce benchmark supply to ‘showcase transactions’, Barclays analysts warn.

-

Standard & Poor’s cut its rating on another pair of Cédulas programmes this week, but the stellar result for Bankinter and UniCredit showed single-A rated trades can still find a stampeding demand. UK buyers bought more than expected in both deals, as syndicate leads pointed to a new class of accounts that could support peripheral transactions.

-

Bankinter on Thursday swiftly followed peripheral peer UniCredit’s success from the day before. The Spanish borrower launched a blow-out three year benchmark trade 20bp inside initial price thoughts, as traders struggled to keep up with a big spread rally in peripheral paper.