Learning Curve

-

While market capitalisation weighted indices and portfolios have been incredibly popular in recent years, data show that their equally weighted brethren can have an edge with lower concentration risk and better performance.

While market capitalisation weighted indices and portfolios have been incredibly popular in recent years, data show that their equally weighted brethren can have an edge with lower concentration risk and better performance. -

To make trading algorithms useful for derivatives execution, measurement of their effectiveness must be carefully tailored to each user, writes Yuriy Shterk, head of derivatives product management at Fidessa.

-

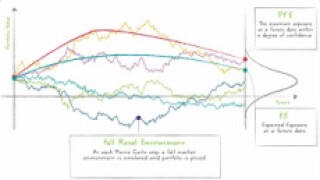

Risk management is, by nature, evolutionary, but the 2008 financial crisis marked an inflection point that changed the paradigm for the industry. It ushered in an era of greater regulatory scrutiny, with risk management emerging as a leading priority for financial firms and policy makers, who pledged to establish new rules that would enhance market stability and mitigate the likelihood of another financial meltdown.

-

Progress on global derivatives reform is at a critical juncture. The goal of enhanced transparency, identified by the G20 following the 2008 crisis as crucial to the supervision of the financial system, remains only partly addressed because of a number of practical and legal barriers that limit data sharing across jurisdictions. As a result, the cross-border identification of systemic risk remains challenging for macroprudential authorities.

-

2014 continued to be an active year for financial regulation in the EU, with a push to finalise much of the outstanding primary legislation on the regulatory reform agenda and to move towards implementation of regulation already in place. The derivatives market will be particularly affected by the new regulatory landscape and the market will face many new challenges into 2015 and beyond, which we consider further below.

-

In today’s regulatory environment there are numerous know-your-customer checks that need to be performed and accurate client and counterparty data checks that need to be made to ensure global regulatory obligations are met. Not only do firms need to make substantial changes to their internal processes to meet these requirements, they must ensure that the counterparty and client data they hold is accurate from the outset and then efficiently managed on an ongoing basis. Legal entity data management is far from a simple task, however, and with a swathe of risk management and investor transparency requirements due to enter into force over the coming years, firms need to give this critical activity the appropriate consideration.

-

The introduction of T+2 has marked another milestone in the effort to reduce systemic risk for firms trading European securities. But what about other asset classes, such as derivatives? The inconvenient truth is that the world of derivatives, which some view as a much riskier investment choice, lags a long way behind equities in terms of operational efficiency. Here Steve Grob, Director of Group Strategy at Fidessa, looks at the reasons why and suggests how derivatives market practitioners can not only learn from their equity counterparts, but leapfrog ahead of them.

-

Six years on since the global financial crisis, Europe has made great progress in transposing the G20’s regulatory framework to reform the over-the-counter derivatives market into law and incorporating that workflow into the single market project. The G20 Leaders Summit in Brisbane in November is an opportune time to reflect on this transit and what remains to be done as the industry seeks to restore the integrity of the global financial system.

-

As pressures for timely reporting of OTC transactions mount on both sides of the pond, Ian Salmon of ITRS Group explores the challenges that this presents, while explaining why the sell-side requires a fresh approach to avoid heavy fines and reputational damage.

-

The next five years will continue to be a time of adjustment as sell- and buy-side firms get used to the realities of the financial markets, post-crisis. Change will be the only constant – and with change, comes opportunity.

-

IFRS 13 “Fair Value Measurement” became effective 1st of January 2013. The International Accounting Standards Board (IASB) issued IFRS (International Financial Reporting Standards) 13 in May 2011 to improve the consistency of fair value measurements. IFRS 13 establishes a single source of guidance for fair value measurements for all financial instruments. It clarifies the definition of fair value in general as an exit price and enhances disclosures about all fair value measurements.

-

Years ago, the motivational guru Tony Robbins came to visit my office, searching for the attributes of successful options trading. I was nervous about making a good impression. After all, he was the expert on success who wrote the book on getting the edge. What advice could I possibly offer? During the interview, it occurred to us both that the “secret sauce” of trading is similar to the required attributes of any profitable business. It must have a definable and consistent “edge”, it must be hard for others to harvest (even if the basic business concept is easy) and it requires relentless discipline.