Free content

-

As Europe’s economy regains its long lost momentum, private equity firms are at last expected to start putting more of their unprecedented mountain of dry powder to use in 2018. Signs are already there of PE firms making bigger bangs with leveraged buy-outs, and if that continues, levfin investors will cheer the flow of new debt that results. Victor Jimenez reports.

As Europe’s economy regains its long lost momentum, private equity firms are at last expected to start putting more of their unprecedented mountain of dry powder to use in 2018. Signs are already there of PE firms making bigger bangs with leveraged buy-outs, and if that continues, levfin investors will cheer the flow of new debt that results. Victor Jimenez reports. -

Banks will prioritise funding that helps meet their regulatory ratios in 2018, but covered bonds will continue to play a pivotal role because they provide the cheapest cost of funding. By Bill Thornhill

-

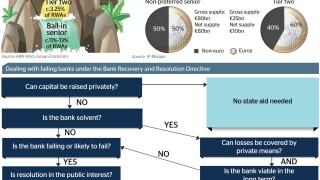

More than a decade after the financial crisis began, European banks are finally close to building new capital structures that should allow bail-ins to replace bail-outs. But with central banks promising to step away from financial markets in 2018, the last push could be the trickiest part of all. By Tyler Davies.

-

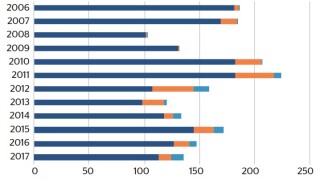

Having waited a while before testing the water, insurance companies are finally issuing all the debt capital securities described by the Solvency II regulations. But the future looks complicated, as growing calls for an insurance resolution framework threaten to overhaul the way firms are supervised in Europe. By Tyler Davies

-

Banks are now close to meeting their regulatory targets for issuing the new kinds of capital.They will turn their attention in 2018 to optimising their capital structures, writes Tyler Davies.

-

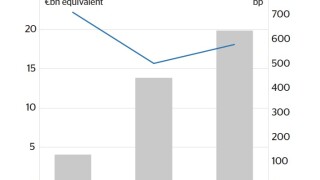

Technical factors suggest additional tier one (AT1) capital yields will continue to fall this year, even after a remarkably strong 2017. Ironically, the Banco Popular resolution, which burnt AT1 holders, actually made the asset class look more attractive in relative terms. Jasper Cox reports.

-

Canadian public sector issuers had a barnstorming year in the international debt markets in 2017, propelled by a strong economic performance by Canada and many of its provinces. But challenges loom — uncertainty over Canada’s trade relationship with the US, geopolitical instability and changing global monetary policy are just three of many concerns that borrowers, bankers and investors in Canada’s public sector bond markets will have to deal with this year. GlobalCapital met key market participants in Toronto in November to discuss the key issues.

-

Supranational and agency borrowers enjoyed enviable conditions in the bond market last year, with European Central Bank quantitative easing creating long end funding opportunities and a deep dollar market providing some big deals in the short end. But central bank actions could mean the environment is even better in 2018, writes Craig McGlashan.

-

The Swiss franc bond market’s twin maladies of low interest rates and unattractive basis swap levels, which have hobbled foreign issuance since 2015, are showing signs of regression. Arbitrage windows will open this year as the market’s health improves, and financial institutions are best placed to exploit them. By Silas Brown

-

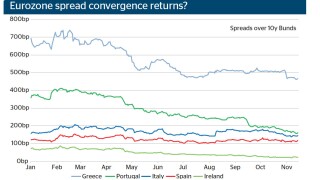

Thanks to quantitative easing, sovereign bond markets have been impervious to political volatility in recent years, getting through 2017’s shocks and surprises in serene style. But that could all be about to change as the European Central Bank starts to wind down its vast bond buying programme. Craig McGlashan reports.

-

Niche currency bond markets in 2018 will offer borrowers not just a chance to find arbitrage funding — and investors some respite from the brutally low yields in core markets — but possibly a slightly easier regulatory regime than that applied to core currencies, writes William Chambers.

-

Five years after being pushed on to trading venues in the US by the Dodd-Frank Act, over-the-counter derivatives players are beating a similar path in Europe, under the Markets in Financial Instruments Directive II. Most people think MiFID II has been a worse experience, and will make it harder for small players. But efficiency gains may follow. Ross Lancaster reports.