Euro

-

The outlook for peripheral covered bonds is still positive, and despite the disappointing result achieved by Bank of Ireland on Wednesday, bankers expect further supply.

-

Bank of Ireland has priced the third covered bond from Ireland this year and, in contrast to BNP Paribas which issued a 10 year deal on Tuesday, it paid a decent 3bp-4bp new issue premium for the seven year offering. Despite that, it was the issuer's least subscribed deal since 2012.

-

The Spanish government has published a new securitization law which is expected to allow issuers to structure covered bonds backed by a segregated pool. The move could spur issuers to consider conditional pass through structures backed by a broad range of assets, said analysts at Moody’s and Société Générale.

-

Until recently, green covered bonds were always more of a theoretical discussion than one that had taken root. But on Monday, the asset class took a giant leap forward as Berlin Hyp issued its €500m seven year Grüner Pfandbrief, a transaction that was placed with many new types of investor. The deal could be just what the central bank-oppressed market needs.

-

BNP Paribas made an opportunistic move to price the first 10 year covered bond in over a month on Tuesday via an intraday execution. Strong demand and a book that was twice covered allowed the issuer to increase the size of the deal to €750m from €500m and enabling pricing almost flat to BNP Paribas’ existing curve.

-

The assets of distressed Austrian bank Oevag will be divided between a bad bank and Volksbank Wien-Baden. Unlike the case of Kommunalkredit however, all of the bank’s outstanding covered bonds will be transferred to Volksbank. Analysts say this indicates the Austrian regulator is returning to a more traditional and investor friendly method of bank splitting.

-

Berlin Hyp on Monday reaped the rewards of its extensive roadshow and attracted the highest oversubscription of any German covered bond issued this year at the tightest spread for the tenor. The astonishing result was achieved with the help of Green and SRI investors that bought 48% of deal. The transaction sends a strong signal to other covered bond borrowers that Green covered bonds diversify funding, suggesting they have a bright future.

Berlin Hyp on Monday reaped the rewards of its extensive roadshow and attracted the highest oversubscription of any German covered bond issued this year at the tightest spread for the tenor. The astonishing result was achieved with the help of Green and SRI investors that bought 48% of deal. The transaction sends a strong signal to other covered bond borrowers that Green covered bonds diversify funding, suggesting they have a bright future. -

UK covered bond programmes have the highest foreign exchange gap according to Moody’s. But the fact UK issuers have issued predominately issued in sterling this year shows they are attempting to reduce this exposure.

-

Berlin Hypothekenbank is readying the market’s first Green Pfandbrief and is likely to launch the bond on Monday or Tuesday next week. Analysts expect there to be a minimal spread difference between the borrower’s green and conventional curves.

-

UniCredit Czech and Slovakia has set the final spread for the first covered bond to be backed by a mix of Czech and Slovakian mortgages. The bond has been expected since the borrower first met investors on a roadshow in November.

-

Turkish banks finally look set to become a feature of the covered bond market this year as Akbank lines up its first euro-denominated benchmark. The bank still needs to finalise its cross currency swap arrangements, a funding official told The Cover, but a deal could emerge in a matter of weeks not months.

-

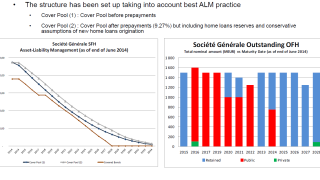

Société Générale issued and retained over €5bn of covered bonds, spread over eight deals with maturities between six and 15 years on Monday. The supply provides contingency backstop liquidity for the bank, and forms a normal part of its liquidity management activity.