The Primary Equity Connect (PEC) will undoubtedly be revolutionary. The link, which will effectively allow Mainland investors to directly participate in Hong Kong IPOs, could bring immense change to the city’s equity market.

The leading upside is diversity. Hundreds of millions of new investors from China will clearly mix up trading in Hong Kong’s market. And in turn, more global companies looking to list will consider a market that has a buy-side of unparalleled depth. No doubt, issuers will be quick to recognise the potential of getting higher valuations and successful deals done.

Mainland buyers are starved of primary equity investment opportunities given that the China Securities Regulatory Commission has been slow to approve IPOs, with around 600 companies in the queue. In addition, Chinese investors are desperate for diversification and for them that will be the likely selling point of the PEC —exposure to opportunities they otherwise would not get.

In the long term, Chinese money needs to be put to work and Hong Kong will be a natural hub to facilitate that. It is just a question of how.

But while the above explains why it makes sense for the Hong Kong Stock Exchange (HKEX) and the Securities and Futures Commission to move ahead with a connect, the question of controlling these potential flows is one regulators should very much heed.

Dark history

The A-share market is dominated by mom-and-pop investors that are often equated with casino punters driven by momentum. One only has to think back to the summer of 2015 when China’s retail buyers flooded into the A-share market after an impressive rally, buoyed by the conviction that the government wouldn’t let the market drop.

But as investments became increasingly driven by margin lending, when sentiment turned the ensuing collapse erased trillion of renminbi from China’s stock market’s market capitalisation in a matter of days.

Things are certainly more stable now in China’s equities market. But it goes without saying that allowing Mainland money into Hong Kong IPOs could trigger a degree of volatility never experienced on the city’s exchange.

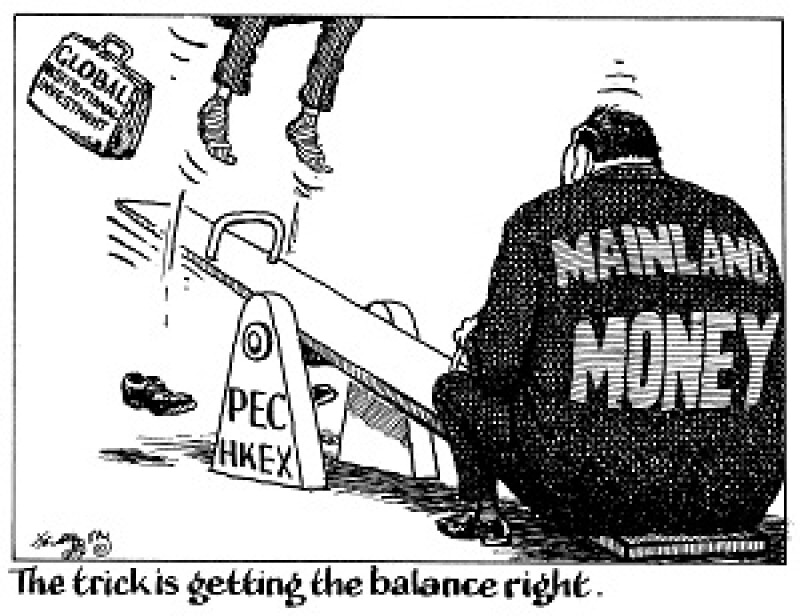

To battle this, the authorities will surely be considering a quota system, much like the one used for the existing Stock Connect system, which allows cross-border trading in equities. But quotas for a primary market connect are a different beast.

To impose a low quota for southbound investing would be missing the point of the whole exercise. HKEX could partially meet its goal of increasing the appeal of its market, but would be wasting the opportunity it has touted for at least the past two years. If wooing big international issuers to Hong Kong is one of the targets, as the HKEX has said publicly in the past, it will have to open the tap and let Chinese money in.

On the flip side, imposing a very high quota could very well mean that the Hong Kong exchange becomes dominated by China’s massive investor base — leaving very little room for global institutional investors.

If the IPO connect goes live, one way or another the Hong Kong regulator needs to be able to maintain its integrity and independence under increasing influence from Chinese investors, issuers and authorities. Only then it can become an even more attractive and credible destination for international issuers and issuers.

If done right, a successful PEC could easily cement Hong Kong’s position as the leading ECM market globally. But if it is not careful, it could just as easily mar the city’s reputation. There’s a lot at stake, and HKEX’s move is one everyone will be watching closely.