Covered Bonds

-

Well done Goldman Sachs, you’ve managed to devise a structure that has both the covered bond market and the ABS market talking at the same time. The covered bond market seems to have adopted the attitude that ‘imitation is the sincerest form of flattery, just don’t try to pass it off as a real covered bond’. The ABS market seem to have adopted an ‘anything the covered bond market can do..’ attitude.

-

Banks that have held a leading market share of the covered bond business are also dominant across all liquid fixed income markets. Being German helps, but those institutions that offer genuine added value in terms of trading and advisory services have performed consistently well. The Cover examines the driving forces between the winners and losers in covered bonds.

-

Since Goldman’s FIGSCO (Fixed Income Global Structured Covered Obligation) trade hit the screen, capital markets commentators, The Cover included, have been scratching heads and stroking beards about what it actually is.

-

Toronto-Dominion Bank could become the next Canadian bank to issue a covered bond after it received regulatory approval from the Canada Mortgage and Housing Corp (CMHC) this week. The sign off comes weeks after Canada set out guidelines on the liquidity coverage ratio.

-

Goldman Sachs may have been hoping that it could get away with calling its newly structured triple recourse hybrid a covered bond. Though it is being marketed to covered bond investors, FIGSCO is clearly nothing like a classical covered bond. But Commerzbank, NIBC and NordLB all encountered controversy when they successfully issued innovative deals, suggesting the clumsily named acronym may be a success – especially in an environment of furious yield chasing and a shrinking triple A universe.

-

The long end of the covered bond market has outperformed for many months, but even more so over the last two weeks. Bankers expect the rally to continue even though yields are now approaching their lowest in five years, and a point where major trend reversals have previously taken place.

The long end of the covered bond market has outperformed for many months, but even more so over the last two weeks. Bankers expect the rally to continue even though yields are now approaching their lowest in five years, and a point where major trend reversals have previously taken place. -

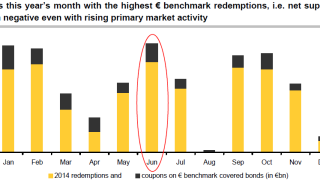

A week of no new issues in the covered bond market has confused some market participants, coming straight after the second busiest week of the year. But, at quarter end and with holidays around the corner, banks’ decisions over participation in the ECB’s targeted longer-term refinancing operations (TLTRO) programme — coupled with anticipation of a liquidity coverage ratio (LCR) announcement from the EBA— may be what is muting primary issuance.

-

A week of no new issues in the covered bond market has confused some market participants, coming straight after the second busiest week of the year. But at quarter end and with holidays around the corner, banks’ decisions over participation in the ECB’s targeted longer-term refinancing operations (TLTRO) programme — coupled with anticipation of a liquidity coverage ratio (LCR) announcement from the EBA — may be what is muting primary issuance.

-

Austrian covered bonds were steady on Tuesday after a swathe of Moody’s senior downgrades hit covered bonds, leading bankers to say its methodology has serious weaknesses. Separately, Standard & Poor's upgraded €27bn of multi-Cédulas in a move which analysts said would have little impact and could soon be reversed. The fact multi-Cédulas have outperformed Austrian covered bonds all year is due to the other factors.

-

A couple of issuers could be ready to launch covered bonds and the hope is they will do so before next week when Scandinavia is on holiday and many issuers head into blackout, said bankers on Tuesday. The focal point of primary chatter on Tuesday continued to be on Goldman Sachs’ new FIGSCO structure. In the secondary market peripheral covered bonds tightened, following in the wake of sovereign markets.

-

The covered bond market got off to a restrained start on Monday with syndicate bankers noting that some borrowers were looking at possible issuance this week, with a view to taking advantage of strong credit market conditions ahead of the summer break. Meanwhile, Goldman is on the road from Wednesday with its controversial hybrid FIGSCO issue.

-

Banks that have held a leading market share of the covered bond business are also dominant across all liquid fixed income markets. Being German helps, but those institutions that offer genuine added value in terms of trading and advisory services have performed consistently well. Bill Thornhill examines the driving forces between the winners and losers in covered bonds.