Covered Bonds

-

Covered bond issuance in June was the strongest since 2011 and issuance over the year as a whole is in line to meet the €130bn forecast that Barclays research analysts made in December last year, the bank said on Thursday. UK, Canadian and Italian issuance may bolster supply over the second half of the year other bankers and analysts said.

-

The Cover’s annual awards for the covered bond market will be held at the Garden Palais Lichtenstein in Vienna on the evening of September 25. The awards celebrate the most important achievements in our market — as decided by the market.

-

With €70bn sold this year, covered bond issuance should trounce last year’s €98bn total. Better still, with several countries returning to the market and regulations likely to improve conditions, this year’s progress should be sustained for years to come.

-

Bayerische Landesbank took advantage of an empty market to price what could be one of the last covered bonds before the summer lull kicks in. The €500m seven year Pfandbrief attracted a heavily oversubscribed and granular book that gained solid momentum from the start — in contrast to other recently issued Pfandbriefe.

-

Bayerische Landesbank took advantage of an empty market to price what could be one of the last covered bonds before the summer lull kicks in. The €500m seven year Pfandbrief attracted a substantially oversubscribed and granular book that gained solid momentum from the start — in contrast to other recently issued Pfandbrief.

-

Standard & Poor's upgraded BBVA’s mortgage backed covered bond programme from A to AA- after the European close on Tuesday, while Fitch upgraded UniCredit’s Italian programme from A+ to AA-. The upgrades take the programmes towards a level that gives regulatory benefits. UniCredit has most to gain.

-

Luca Bertalot, Secretary General of the EMF and ECBC, speaks to The Cover following Tuesday's EBA report.

-

The European Banking Authority published its first comprehensive overview identifying the key features and practices of a prudentially sound covered bond market on Tuesday. The report provides advice to other regulators on the conditions that would justify the market’s continued preferential risk weight treatment.

-

Canadian Imperial Bank of Commerce recently updated its covered bond prospectus, giving rise to speculation that it could return to the covered bond market this year. CIBC is only one of two Canadian banks that have not issued in euros in 2014 and was last seen in the market in July 2013.

-

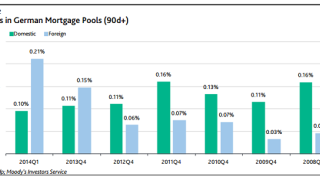

Arrears in foreign assets backing German mortgage Pfandbrief increased by 40% in the first quarter of 2014, according to Moody’s, although the share of foreign mortgages in Pfandbrief cover pools is on a steady decline.

Arrears in foreign assets backing German mortgage Pfandbrief increased by 40% in the first quarter of 2014, according to Moody’s, although the share of foreign mortgages in Pfandbrief cover pools is on a steady decline. -

Banca Monte dei Paschi di Siena’s (MPS) covered bonds’ outperformed the market on Monday after Moody’s upgraded them from Ba1 to Baa3 following the European close on Friday. The new rating more than halves the capital charge as the bonds move into investment grade territory, opening up demand to a much larger investor base. This swell of new interest should ensure that MPS outperforms the market over the summer.

-

Flows were mostly focused on buying of peripheral national champions on Monday, as the impending liquidity injection from the European Central Bank is expected to crimp supply prospects by more from these regions. This is especially the case in multi-Cédulus where RBS research picked 10 prospective deals that may outperform. In the primary market, talk was focussed on the wrapped collateralised debt obligation being marketed to covered bond investors until Tuesday by Goldman Sachs.