Spain

-

Following the June 5 ECB announcement Bonos have rallied strongly, while Cédulas have reacted to a lesser extent, leaving clear performance potential, a Barclays research note published on Thursday argues. But what is nice in theory is more difficult in practice, traders said — large blocks of Cédulas are difficult to source without pushing up prices.

Following the June 5 ECB announcement Bonos have rallied strongly, while Cédulas have reacted to a lesser extent, leaving clear performance potential, a Barclays research note published on Thursday argues. But what is nice in theory is more difficult in practice, traders said — large blocks of Cédulas are difficult to source without pushing up prices. -

Covered bond secondary markets opened on a much firmer footing on Friday, with dealers and clients singling out higher yielding weaker credits, particularly in the periphery, where offers are hard to find. The move came after Thursday’s stimulus package from the European Central Bank, and after Standard and Poor’s upgraded several Spanish banks.

-

BBVA returned to the covered bond market for the first time in over a year on Wednesday with a 10 year Cédulas that attracted a fairly granular book. The coupon paid was the lowest ever for a 10 year in the history of the Spanish Cedulas market.

-

Non performing loans in multi-Cédulas deals are continuing to rise according to Moody’s. And Bank of Spain data released last week showing that the trend maybe levelling off, understates the actual level by as much as half. See The Cover's interactive chart for more.

-

Spread widening in periphery covered bonds are a correction rather than a trend reversal, said Commerzbank’s research team this week.

-

Declining Spanish covered bond issuance has resulted in higher levels of overcollateralization, said Moody’s on Tuesday. This is credit positive because bondholders are better protected.

-

Spanish bank Kutxabank took advantage of improving conditions after a dismal open on Monday to issue the country’s fourth covered bond of the year. Following Swedbank and Bank of Austria last week with a seven year tenor, the deal is the first such tenor from Spain this year and a clear indication of where the sweet spot on the curve lies.

-

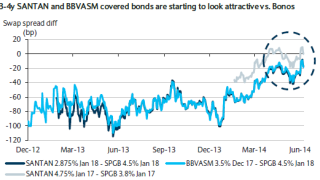

Many Portuguese covered bonds could have their ratings upgraded soon, after Moody’s raised the Portuguese sovereign rating last Friday. Banco Santander Totta’s most recent deal, which is a strong candidate for upgrade, was trading 8bp tighter from last week on Monday, but this was due to ECB rate cut hopes, and not credit upgrade hopes.

-

The covered bond market was in good shape on Wednesday as bankers reported renewed interest in peripheral names and the multi-Cédulas sector. The primary market is expected to pick up next week as Scandinavian and German issuers line up.

-

The recent correction lower in Multi-Cédulas following Standard & Poor’s rating downgrades last week has almost run its course. Though there is a slight risk that month-end portfolio re-balancing will provoke further near-term losses, the longer range picture is fundamentally and technically well supported, bankers told The Cover on Wednesday.

-

Moody’s announced a positive rating action on CaixaBank on Friday, reflecting declining asset-quality pressures, and an improvement in its earnings. The news comes as its most recent deal has performed well, and amid growing expectations that the worst is behind for the Spanish economy. With the interest rate outlook likely to remain constructive and Cédulas likely to stay technically squeezed, the sector’s performance outlook has not looked this good in years.

-

Banco Popular Español (BPE) returned to the covered bond market on Tuesday to issue only the third Cédulas of 2014, and the issuer’s largest covered bond in three years. Though by no means the most attractive spread seen this year, the triple digit pick-up enticed a broad audience of real money investors.