Euro

-

Nationwide Building Society’s third covered bond of the year had to offer an attractive new issue premium because there was considerable price sensitivity in the book. The deal illustrates that, despite a technical undersupply of covered bonds, there is a greater balance between supply and demand than perceived, especially for bonds ineligible for the European Central Bank’s purchase programme.

-

Commonwealth Bank of Australia (CBA) was set to price Australia’s first euro benchmark covered bond in single digit territory over mid-swaps on Tuesday. The deal, which was announced at short notice and which was slow to build early traction, nevertheless managed to attract new investors, though at 14%, bank demand was disappointing given the bonds are now eligible for their liquidity buffers.

-

The national central banks of France, Portugal and Spain were reported buying covered bonds issued by banks from their own jurisdictions on Monday, said dealers. The amounts were small and the purchases were price sensitive, they added. Offers in Banca Monte Paschi Siena’s covered bonds were unchanged as its shares came under pressure following reports it may need to raise €1.7bn in fresh capital.

-

On Friday Fitch put the AA+ rated covered bond programmes of Caffil and CoFF, and the public sector programme of BNP Paribas, on rating watch negative (RWN), following an identical action on the French sovereign earlier last week.

-

The legal document approving the European Central Bank’s third covered bond purchase programme was published on Friday and takes effect on Saturday, suggesting it would be permitted to start buying covered bonds from Monday. The ECB told The Cover that the legal act was a mere formality and comes as secondary markets have begun to stabilise after volatility earlier this week.

-

On Thursday the secondary covered market found itself caught between a tumultuous peripheral sovereign market and fevered anticipation of the ECB finally wading into the covered bond market. While traders reported light profit taking in Spanish and Italian names, the strong bid that was seen for periphery names over the last week has evaporated.

-

S&P downgraded a number of Cédulas Hipotecarias and upgraded one Cédulas Territoriales as it begins to implement its sovereign ceiling methodology. The new ratings are now broadly in line with the other agencies and were expected. The agency is expected to announce revisions to Italian covered bond ratings that are also likely to lead to two downgrades.

-

La Caisse Centrale Desjardins du Quebec (CCDQ) was back in the euro market on Wednesday with its second five year legislative covered bond of 2014, this time achieving a solid book and pricing at the tight end of guidance. The positive result was in contrast to its disappointing inaugural deal in March. Wednesday’s deal was priced at an expected 2bp pick-up over the stronger Canadian Imperial Bank of Canada’s (CIBC’s) five year trade last Wednesday.

-

Covered bond yields fell on Tuesday as Bunds rallied following a larger than expected fall in the ZEW business sentiment index and lower than expected inflation data. The European Central Bank (ECB) could be poised to commence buying on Wednesday after its scheduled meeting. Since the ECB is likely to be targeting the spread to government bonds, Pfandbriefe are likely to be on the bank’s shopping list, as they look more attractive than peripheral bonds versus their government bonds.

-

Goldman Sachs has not given up on its Fixed Income Global Structured Covered Obligation (Figsco). Despite bad publicity, the market has moved in Goldman’s favour since the deal was first announced.

-

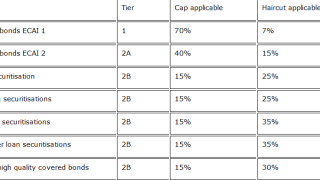

The final text of the European Commission’s (EC) Delegated Act on the Liquidity Coverage Ratio (LCR) says that covered bonds that are not rated will be eligible for inclusion into category 2B. The announcement on Friday shows that the European Commission is keen to reduce reliance on credit ratings and should be another boon for the covered bond market.

The final text of the European Commission’s (EC) Delegated Act on the Liquidity Coverage Ratio (LCR) says that covered bonds that are not rated will be eligible for inclusion into category 2B. The announcement on Friday shows that the European Commission is keen to reduce reliance on credit ratings and should be another boon for the covered bond market. -

Canadian Imperial Bank of Commerce has priced the tightest ever Canadian covered bond issued in euros. The price discovery process was also notable for skipping out guidance and going straight from initial price thoughts (IPT) to final spread.