Denmark

-

A European issuer is about to bring the first three year Maple bond in two years, after several moving parts moved into place to make the deal possible.

A European issuer is about to bring the first three year Maple bond in two years, after several moving parts moved into place to make the deal possible. -

Henrik Stille, covered bond portfolio manager at Nordea Investment Management in Copenhagen talks to The Cover about the fixed income rout, the rates outlook, what it means for covered bonds and how he managed to beat the index and deliver a solid return.

-

Landesbank Hessen-Thüringen Girozentrale (Helaba) issued a €1bn Pfandbrief on Wednesday at a final spread that was deeply through mid-swaps but got a strong response as it was able to offer a positive spread to Germany, where yields are negative. At the same time, Danske Bank issued this week’s only euro benchmark. As it was not eligible for the covered bond purchase programme it offered a quite attractive spread.

-

The International Monetary Fund’s recommendation that Danish banks reduce reliance on short-term funding and limit lending on variable rate, as well as interest-only mortgage loans, is credit positive for Denmark’s credit institutions, said Moody’s on Monday.

-

Danske Bank opened books on Wednesday on a triple-A rated five year euro benchmark, its second euro deal of the year coming soon after its seven year sterling transaction early last week. A solid book build blew away Tuesday’s concern that a soft credit market and a series of upcoming potentially disruptive events may have turned the deal sour.

-

Danske Bank has mandated leads for a five year euro benchmark, its third benchmark this year and second in euros. The deal is expected to be launched on Wednesday.

-

The sterling FRN market picked up on Monday as Barclays was set to price the largest ever covered bond in the domestic currency and Danske Bank was poised to price a benchmark. The two borrowers follow Nordea Eiendomskreditt which attracted robust demand last week.

-

Nykredit Realkredit opened the Danish auction season on Monday with the sale of Dkr800m of two year covered bonds and Dkr7bn of one year bonds that are structured with a maturity extension trigger. Despite the triggers, the one year portion was oversubscribed multiple times and priced a long way inside swaps which Nykredit was very satisfied with.

-

Danske Bank’s first covered bond of the year offered an attractive spread relative to its Nordic peers, which made it a relatively straightforward sell. But even so, the final level was just one third of Danske’s differential against Sweden a year ago.

-

Danske Bank has mandated joint leads for a euro seven year benchmark, which is expected to be priced on Tuesday. The Danish bank had been expected to make a deal announcement some time ago, but decided to hold back after some tightly priced core covered bond deals failed to garner a sizeable book.

-

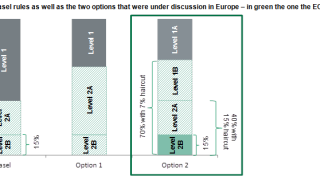

Covered bonds rated AA- or higher will be elevated to a Level 1 asset in Liquidity Coverage Ratio (LCR) according to an internal document being circulated at the European Commission. This backs up a press release from the Danish government last Friday. The improved structural bid is most likely to affect bonds lower rated bonds previously ineligible for the LCR, said analysts.

-

A new draft recommendation from the European Commission (EC) that appeared on the Danish government’s website on Friday says covered bonds which meet certain criteria can be considered extremely liquid assets and can fulfil up to 70% of bank liquidity buffers with a 7% haircut.