To understand some of the market dynamics and sentiment, CSC, a provider of specialized administration services to alternative asset managers, collaborated with GlobalCapital to survey 180 market participants in securitization from 31 countries, across all sides of the market—issuers, investors, arrangers, service providers, and others.

Some messages came through loud and clear. Extraordinary central bank interventions across the developed world have left fixed income yields at rock bottom and intensified the “reach for yield.” It’s no longer sufficient in fixed income portfolios to simply clip coupons. Investors must leave their comfort zone, move down the credit curve, and take a view. Carry is no longer sufficient.

This theme was repeated in several of the sub-asset classes on which we questioned market participants. In U.S. consumer ABS, bond buyers are tempted by subprime auto ABS, especially in the mezzanine part of the capital structure. Esoteric ABS, especially whole business, proved popular, while European ABS buyers also flagged mezzanine bonds as a buying opportunity.

US and European ABS volumes (USD) hit by pandemic (Source: SIFMA/AFME)

But greed is balanced with fear. Consumers and businesses around the world have already suffered deeply from the impacts of the Covid-19 pandemic. As cheap government loans and salary support schemes roll off, the scale of the devastation will become clear, and plenty of borrowers—corporates and individuals alike—will struggle to service their debts.

There are some obvious losers, such as hotel or retail commercial mortgage-backed securities, though these asset classes were not our primary focus in the survey. Respondents told us aircraft ABS looked unattractive, but there are certainly some funds running distressed or special situations strategies that are actively looking for opportunities in the sector. At the right price, buyers emerge, looking to take advantage of the structural protections built into securitized products and source money-good exposures at dislocated price levels.

How other parts of the securitized products universe will deal with the COVID fallout is not yet clear.

Prices in much of the consumer universe have rebounded to pre-Covid levels, helped in part by optimism about vaccine rollouts.

But in both the United States and Europe, participants were concerned about the prospects for marketplace lending. The sector has always struggled with a perception that it creates “adverse selection”—that is, borrowers who struggle to get credit elsewhere turn to the lending platforms as an alternative.

Whether or not those concerns are valid, survey respondents considered it the riskiest asset class within consumer ABS on both sides of the Atlantic. We assume they’re referring largely to unsecured personal loan ABS, originated through marketplace platforms—which even in good times would be some of the riskiest assets used to back consumer ABS.

Again, though, securitizations give investors options. While market participants responding to the survey saw better value in mezzanine and subordinated positions for auto ABS, perhaps staying senior in the stack is a better move for marketplace loans.

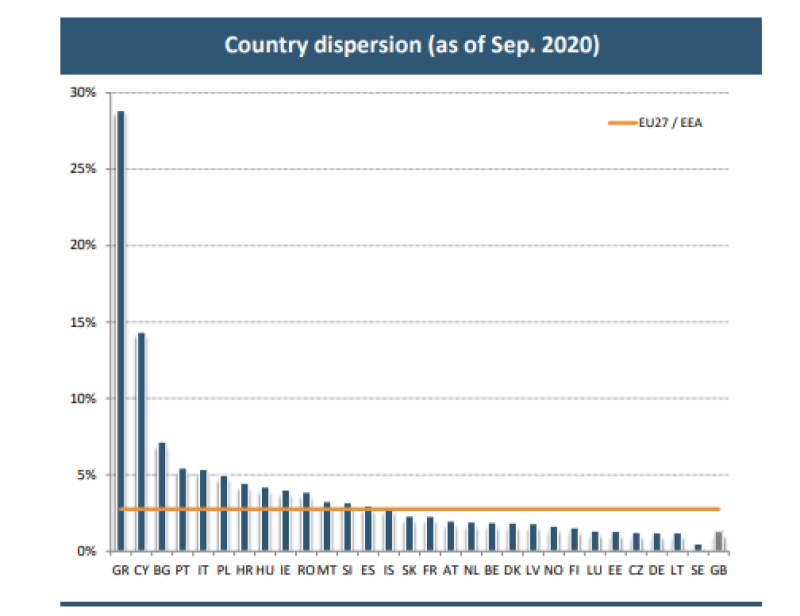

When credit goes bad, it can still end up in the securitization market, perhaps packaged as a nonperforming loan (NPL) deal. We asked respondents about the European NPL market outlook. The sale of existing NPLs slowed in 2020, but 2021 is widely seen as the year when banks will be forced to clean balance sheets and sell off some of their newly defaulted exposures.

Survey respondents saw an increase coming, but a relatively modest one, with supply up between 1% and 24%. The sale of NPLs doesn’t always mean securitization of NPLs; and it’s most likely to emerge in countries like Italy and Greece, which offer government guarantees to encourage securitization.

European NPL ratios set to increase in 2021 (Source: European Banking Authority)

The outlook for nonperforming commercial real estate divides opinion, however. Hard assets and strong security packages have made real estate-backed loans a mainstay of the most recent NPL cycle in Europe, but the COVID crisis might change that.

Investors cannot assume that real estate will bounce back, as it has in previous cycles. Even after “normality” has been restored, it’s not clear that office work or shopping habits will ever be the same again.

Thanks to all our survey respondents for their insights and for taking the time to complete it.

Experience matters

CSC supports issuers, investors, arrangers, originators, and advisors across all asset classes. Clients entrust us with their SPV management, independent director needs, trustee and agency commitments, accounting requirements, and more across the United States, Europe, and Asia-Pacific. Commercial and agile in our thinking, our team brings innovative ideas to client interactions. With more than 120 years of independent ownership, we stand alone for long-term stability amid a turbulent marketplace.

Methodology

The data is based on a market study conducted by GlobalCapital during August and September 2020. A total of 180 responses were collected across 31 countries in Europe and North America, spanning mid- and senior-level executive positions and four core stakeholder types: issuer-sponsor, service providers, investors, underwriters-arrangers-bookrunners-structurers, and other.

About the survey

The Global Securitization Market Survey flagship report, “Securitization Markets Weigh Up an Extraordinary Year,” was prepared by CSC and GlobalCapital.