The quiet work of a little known expert panel over the last year has inaugurated a new phase in the history of multilateral development banks. Frannie Léautier, the group’s chair, spoke to GlobalCapital about why it was needed and what will happen next.

The central thrust of the panel’s report, commissioned by the G20 and presented to it in Bali last week, is that the MDBs could greatly expand their lending, using just their existing capital.

“Our panel was created before we were seeing this major crisis now, after the pandemic,” said Léautier, CEO of SouthBridge Investments in Kigali, who chaired the Independent Review of MDBs’ Capital Adequacy Frameworks. “Now with energy prices and climate risks that are multiplying, it couldn’t be better timing. My hope is that the report has impact, and the MDBs get the extra headroom they need.”

The multilateral development banks are pillars of development finance, of the international world order and of the bond markets.

Their prominence means they are often criticised by development advocates, activists in developing countries, and even Western governments, which jealously guard their dollars and want the MDBs at least not to impede their political interests.

They are rarely criticised in the bond market, where they are regarded as the epitome of stable, top quality credit risk, badged with triple-A ratings that endure undisturbed for decades.

Hidden strength

That contrast hides a secret, however. Those credit ratings are far more secure than they need to be — one expert calls them “quadruple-A”. This has come about because most of the development and government stakeholders do not understand the financial aspects of the MDBs.

Even the small numbers of experts, inside and outside the MDBs, who do understand them are tentative about suggesting changes, for a host of reasons.

The elephant in their room is how the rating agencies treat callable capital — the contingent capital, not paid in, provided by nation state shareholders, which makes up a large part of the MDBs’ capital.

The rating agencies are willing to treat much of callable capital as capital but the MDBs construct their internal capital adequacy frameworks as if the rating agencies are not. That means they are wasting up to three notches of rating headroom.

For many years, knowledge of this issue was confined to a few isolated experts. Among them are the analysts at S&P who estimated in 2016 that, other things being equal, the 19 MDBs the agency rated could have increased lending by two thirds, or $1tr, without losing their triple-A ratings.

But the subject was never properly investigated, nor even mentioned in important public debates about the MDBs.

Léautier (pictured) gives three reasons. The first is that the MDBs simply did not need the extra rating headroom available to them.

“Second is that their risk teams and boards have had a very cautious and conservative approach, which was needed at the time,” she said. “The third thing is that callable capital is a unique feature of MDBs. Not even the shareholders, credit rating agencies and key decision makers among the MDBs fully understand the ways it can be used.”

Time for change

That long silence came to an end on July 20 with the publication at the G20 finance ministers’ and central bank governors’ meeting of the report, Boosting MDBs’ Investment Capacity.

The detailed document, prepared by a panel of 14 development finance experts, centres on five recommendations, sketched in GlobalCapital’s report of the news on Wednesday.

In brief, they are:

1. Change the way risk tolerance is defined, with a thorough internal rethink rather than outsourcing this to rating agencies. Improve dialogue with rating agencies and remove specific leverage targets from the MDBs’ statutes

2. Give credit to callable capital in MDBs’ internal capital models

3. Use more financial engineering such as securitization and risk swaps

4. Give the rating agencies more clarity about the support MDBs enjoy from shareholders and their unique functions

5. Increase stakeholders’ and the public's access to data and analysis about MDBs’ finances and performance, to improve decision making. Raise coordination between MDBs

High backing

Just as important as these suggestions is the forum in which they have been developed and presented.

The report was commissioned a year ago, when Italy was president of the G20, by its International Financial Architecture Working Group, which promotes efforts to make the financial system more stable and resilient.

Since the 2008 financial crisis, the G20 has become the most powerful driving force in international financial policy. Although it has no formal regulatory or legislative powers, it has profound influence. Governments pay attention to what the G20 discusses and decides, and its recommendations tend to be implemented.

The increased regulation of banks since 2008 was driven by the G20, as was the Taskforce on Climate-Related Financial Disclosures.

Just getting the G20 to address the issue was a huge step forward. The main reason why this became possible, Léautier said, was “Just the size of the need. With multiple crises, the needs are so high that everybody is looking for solutions beyond business as usual.”

Little by little

But other trends have been gradually advancing, too. “There have been innovations by some of the smaller MDBs, and by bigger ones at smaller scale — they’ve shown they are able to crowd in private investment,” Léautier said.

The African Development Bank’s Room 2 Run securitization in 2018, in which it shed the mezzanine risk on $1bn of loans to banks, project finance vehicles and companies, freeing up capital for $650m of fresh loans, inspired many others to explore more creative financing, even though the US Treasury’s sour response to Room 2 Run put a lid on overt progress for several years.

The AfDB followed Room 2 Run with a transaction in which it shifted risk into the insurance market. There have so far been no losses on either transaction.

Now the Asian Development Bank is working with 22 insurance companies from outside its region, to provide credit guarantees for 24% of its non-sovereign lending portfolio, which would increase its capacity by $2bn.

Trade and Development Bank, the MDB owned by 22 southern and east African countries, has been transferring risk to the African Trade Insurance Agency for several years, and has recently had its rating outlooks raised by Fitch and Moody’s.

Meanwhile, some private investors have become interested in working more closely with the MDBs — not just buying their senior bonds, but taking more risk, and hence enabling the MDBs’ capital to go further.

The MDBs “have a very powerful model,” said Léautier. “They’re very good at due diligence and identifying risk, they enjoy very strong preferred creditor status. And they are leaders now in the ESG space. If a private investor wants to do good, MDBs are a very credible partner.”

ILX Fund has been established in the Netherlands with $750m from the country’s largest pension fund manager, APG, to co-invest alongside MDBs, directly in their loans.

Lively interaction

These trends, combined with prompting by some experts, have over many years brought some of the nations that own MDBs to the point of realising a rethink of their capital adequacy might be needed.

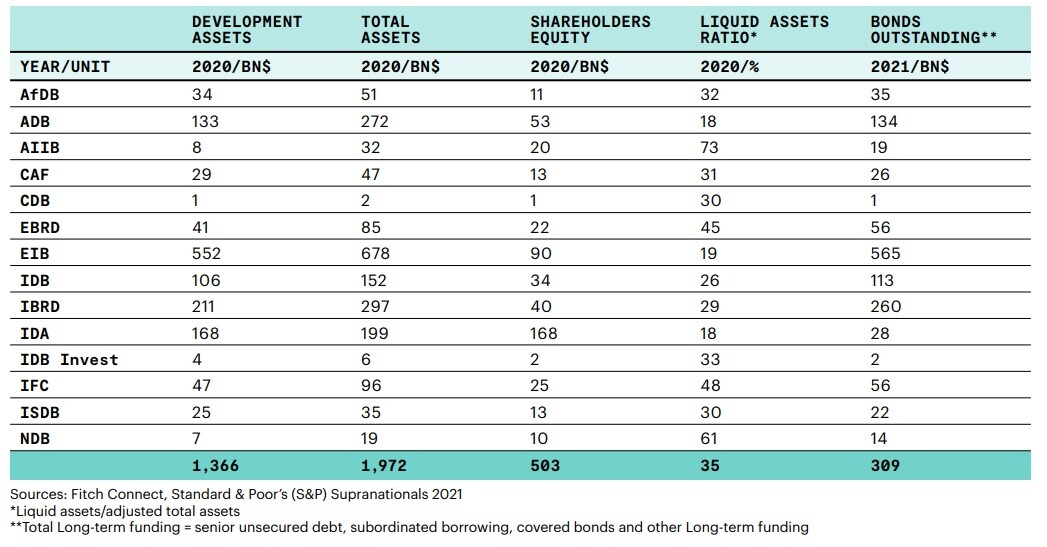

The 14 MDBs reviewed by the panel had a total of just over $1.3tr of capital, of which $1.2tr was callable.

Because they have accumulated reserves from profitable lending, to add to their paid-in capital, the group's shareholders' equity for the purposes of lending totalled $503bn, which supported $1.37tr of development assets and $606tr of other assets such as bonds held for liquidity purposes (see table below from the report).

The Italian G20 presidency appointed an independent panel and empowered it to research and reach its own conclusions. It included academics, former senior risk and finance officials at MDBs and former government officials such as Jinkang Wu, who used to represent China at the World Bank and Global Environment Facility.

Italy provided a secretariat for the panel, and the Rockefeller Foundation granted it use of its Bellagio centre for some meetings.

Support for the work has been carried on by Indonesia, which took over the presidency in December 2021, and will be by India, which assumes the role in December this year.

The panel’s way of working was interactive — there was lots of consultation and discussion with staff at the MDBs and with government officials who oversee them.

Crucially, these included the executive directors, which are appointed by countries or groups of countries to form the boards that run the MDBs on a day to day basis. For example, the World Bank has a board of 25 executive directors. Above that, its topmost board of governors, composed of finance ministers, meets only twice a year.

“We were very happy with the interest of the executive directors, and more sessions are being planned with them,” said Léautier. The MDBs, too, were “generous with their time,” she said, and the rating agencies were “quite open to listening and sharing ideas… they’re open to new ways of thinking about things.”

Countries convinced

The shareholders and MDBs had a chance to read the report before it was published.

With the governments, it has gone down well. “I was very pleased to see its report receive such a broad welcome from G20 members,” said Alessandro Rivera, director-general of the Italian Treasury, in a statement announcing the report. “These are important reforms that could lead to a step change in deploying MDBs’ resources to support vulnerable countries and tackle the daunting challenges we face.”

Senegal, Spain and the Netherlands — not G20 members — also gave welcoming statements, as did other G20 members including the US.

Alexia Latortue, assistant secretary for international trade and development in the US Treasury, thanked the panel for its “clear and thorough analysis” and said: “This report is an important input to us, and all shareholders, as we work on how the MDBs can respond effectively and with scale to multiple global challenges. We urge all shareholders and the banks to carefully consider these recommendations, and be bold in thinking about how to pursue reforms to increase ambition on development finance, given the immense needs.”

The response from the MDBs was much more cautious. Nine large banks — the World Bank Group, AfDB, ADB, AIIB, EIB, EBRD, IADB, Islamic Development Bank and New Development Bank — put out a brief joint statement: “We thank the Panel for its work on this report. We will consider its recommendations carefully as appropriate including those that have already been implemented by some MDBs. As highlighted in the report, there are complex interactions among the recommendations with potential trade-offs and risks that would need to be assessed according to the capital structure, mandates, and shareholding of each MDB, which vary across institutions. We look forward to discussing it among MDBs.”

Securing action

The history of international development is littered with worthy reports that get put on the shelf and never acted on.

Léautier believes the support already shown by the shareholders and MDBs, “plus the enthusiasm and excitement from civil society give a strong feeling that these [suggestions] will be implemented.”

Those involved are taking steps to ensure that happens. The International Financial Architecture Working Group, Indonesia and India are preparing a roadmap for implementation.

In this they can build on a detailed breakdown in the report of all its main recommendations, who they are addressed to, how complex they are to execute and how long they will take. A considerable number could be done in less than a year, the panel reckons, and nearly all in less than two.

“Each MDB would have to go through its internal governance structure and come up with measures,” said Léautier. “They would have to go about it differently — but there are a number of areas where we think they could work together.”

Mutual learning would clearly speed up progress, but speaking with a common voice to the rating agencies might help too.

Coordination necessary

That the MDBs should tackle these issues together could be not only advantageous, but essential.

“Those that innovate sometimes get penalised,” said Léautier. “Coordination has value — it shows the ecosystem [is changing] in a strategic way, so the rating agencies wouldn’t have doubts” — for example, that one MDB was experimenting unwisely or deviating from its proper purpose.

Even more than the rating agencies — which have a small number of very well informed specialists on the MDBs — maintaining a united front is likely to be crucial vis a vis bond investors.

Their trust is vital, and explaining change to them could be much harder if it is done piecemeal or in a confusing way.

To foster this coordination, the panel has recommended creating an MDBs Financial Forum, so all the main stakeholders can discuss capital adequacy frameworks and how to reform them.

A further attraction of unity, Léautier said, was “pricing. When you look at the pricing for Room 2 Run, a lot of the criticisms were that it was very expensive. But with every subsequent innovation, pricing improves. So going together could have benefits on the pricing side. If multiple [MDBs] do it multiple times, they could influence the price.”

In the Room 2 Run securitization, the AfDB paid a 10.625% annual premium to the IIFC Fund, run then by US hedge fund Mariner Investment Group and now by Newmarket Capital, and to Africa50, an infrastructure fund set up by African governments, for their guarantee of the mezzanine slice of loan risk.

Léautier also hopes that by working together, the MDBs could develop “toolkits”, prepared in advance and activated in case of disasters or regional crises to boost lending power for rapid response.

Stress and recovery

The need for development finance is ever-present but at the same time, it goes in cycles, sometimes becoming even more intense than usual.

This pattern holds important clues to why MDBs appear not to have pressed as hard as they could to maximise their lending and development impact.

“The MDBs keep very healthy buffers, which are arguably needed for counter-cyclical responses,” said Léautier. “Therefore they keep more [capital] than they need.”

They want to avoid becoming short of capital, or having to make a sudden rush to raise bond funding, just at a moment of crisis, which could raise their cost of funding, she said.

When crises come, “everybody is trying to respond” and staff are organised to deliver that, Léautier said, but “after it, everybody goes back to business as usual and the teams [formed for crisis response] get absorbed to do normal work.”

That normality is one in which “shareholders haven’t really pushed on risk appetite limits”. MDBs have to operate within capital constraints defined by their risk appetite statements, which are set by the shareholders. Yet the panel believe the shareholders have not paid sufficient attention to defining that appetite — their first recommendation is for shareholders to really think about it and set the limits carefully to “open up headroom”.

Rather than wrapping their credit ratings — and callable capital — in cotton wool as if they were fragile eggs, the MDBs should, the panel argues, have more trust in the robustness of both, but also manage them more dynamically.

“Our report argues that if the MDBs have to work hard to maintain their ratings, it makes them always ready for crises,” Léautier said. “The world has huge needs and we anticipate they will go even higher as climate risks multiply. If buffers get thin, [the MDBs] want loads more capital they can call in.”

Skilling up

The language of the panel’s interactions and report is polite, but its recommendations are strong. The committee is, after all, pointing out that the way MDBs have been run for decades is less than optimal.

“Shareholders may wish to look at the governance structure for their audit and risk committees, in particular so they can make decisions with full knowledge of capital adequacy,” said Léautier. “We propose that they should have that expertise.”

The audit and risk committees are committees of the boards of executive directors. Making sure their members are equipped with full understanding of how capital adequacy works at MDBs and of risk management could lead to better decision making.

The Asian Development Bank has already brought in independent members to its committee, while some of the others draw on analysis from consulting firms to strengthen their knowledge.

To help the banks’ owners, the panel plans to publish a glossary of terms relating to MDBs and a shareholders’ guide.

Gaining momentum

Léautier emphasises that the panel’s suggestions are “an interdependent set of recommendations, not a menu to choose from. When you do them together, you can do more.”

So far, there is still a long way to go to bring private capital into the riskier layers of MDBs’ balance sheets. But progress is speeding up.

“I believe the insurance and reinsurance industry has really evolved,” said Léautier. “It’s willing to do more with smaller MDBs [such as Trade and Development Bank] and could be willing to do things with larger MDBs.”

Another suggestion is that the Multilateral Investment Guarantee Agency, part of the World Bank Group, could play a bigger role, working with other MDBs.

These opportunities could contribute to the MDBs developing an originate to distribute model, as commercial banks have.

The panel also hope for progress in understanding of the MDBs’ preferred creditor treatment (PCT).

It is generally accepted that MDBs rank first in priority for repayment by developing world borrowers that are struggling to repay their debts.

Developing world governments, especially, understand this well — not least because the development banks are their cheapest and readiest source of funds. Defaulting on them would be self-defeating.

As a result, MDBs are almost always repaid, especially by government borrowers. Even private borrowers enjoy preferred treatment on obligations to the MDBs if there are convertibility problems.

But as the report points out, PCT "is informal, with no binding statutory or contractual status". Some critics have even suggested that the MDBs should lose their unique exemption from debt restructurings.

This makes it difficult for risk analysts, whether the MDBs themselves or the rating agencies, to give weight to the credit uplift from PCT.

The panel commissioned an external report on the value of PCT, which is still being prepared for publication. Léautier said this study would “hopefully be reviewed by the MDBs before it can be made available, but the preliminary analysis suggests that the rating agencies don’t give full credit to [the benefit of] PCT. So it could give a boost to ratings” if the study can help give the rating agencies a clearer understanding of the advantages PCT brings.

Using public data for four MDBs, the study has so far found that the probability of governments defaulting on MDB loans is 0.37%, compared with 1.13% for the same borrowers defaulting on bank loans and 1.37% for sovereign bonds. Loss given default is only 5%, compared with 50% for commercial creditors. The report will be completed when fuller data is available.

Money needed

“Our panel worked extremely well together,” said Léautier — and it has clearly acted as a catalyst to set a reaction going across the MDB sector.

The panel — like so many influential groups contributing to making finance markets more sustainable — worked pro bono. “I give my personal time to it because I care about it — I’ve been in three MDBs,” said Léautier. “So I will make myself available for work with the upcoming presidency of India.”

Indonesia and the IFAWG have asked Léautier to continue to support the roadmap for progress, and the panel is going to meet again in a year’s time to report on progress so far.

But to sustain the reaction it has started, a new force will have to take over — ideally the suggested MDB Financial Forum.

“We are working with a group of funders willing to create a fund to support implementation of the ideas in the report,” said Léautier.

Further out, the MDBs themselves may need more resources to put the report’s ideas into action.

“Many innovations required by shareholders are not always funded,” said Léautier. “We said shareholders should also look at the budget implications of reforms. If you’re going to shift risk to the private sector, you have to consider the skills needed to work on risk transfer. You need risk departments to be more dynamic if they are going to look at callable capital in different ways. You need people who understand guarantees and insurance… there is work for the legal department to negotiate contracts.”

The data analysis recommended by the panel could also require IT investment.

MDBs make enough money from their loans to cover staff and operational costs. But they are not free to increase these at will — they need to ask permission from their boards to enlarge operational budgets.

If their capacity to lend really can be increased by as much as the panel believe is possible, they may need extra staff, not just in central functions like finance and risk management, but out in the field, to source more loans.

“What shareholders ask MDBs to do keeps growing — it gets wider and wider,” said Léautier. “If they are going to get more headroom, they could use a bit of their reserves to make sure the MDBs are fit and ready to use that headroom. One thing we wanted to highlight is that there is a price to innovation.”