Covered Bonds

-

With deleveraging nowhere near finished and loan growth in most European banking sectors sluggish, covered bond bankers are struggling to see an end to dwindling supply and tightening spreads. The Cover goes in search of anything that could buck the trend.

-

The French covered bond legal framework is in the process of being redrafted with an updated and improved law expected to emerge, possibly before summer, said panellists at the European Covered Bond Council’s plenary session in Paris on Thursday.

-

Banking union, the single supervisory mechanism and the single resolution fund should theoretically sever the sovereign-bank link, said representatives of the European Commission, the European Central Bank and the European Banking Federation at the European Covered Bond Council’s plenary session in Paris. However, the authorities did not actually know who ultimately had the responsibility to grant or take away a covered bond bank’s license which left delegates wondering who would ultimately be responsible for covered bond supervision.

-

Hypovereinsbank followed Bayerische Landesbank (BayernLB) on Wednesday with a similarly sized deal of the same tenor. But with a marginally lower rating, and hence a wider spread, it was able to attract an incrementally larger book.

-

Leading industry figures have told The Cover they expect a legal overhaul of the Polish covered bond law to mean increased volumes from the sector, as the reforms should raise LTV limits, allow soft bullets, and mandate minimum OC, according to an exclusive English translation of the text obtained by The Cover. The law change is supposed to encourage Polish banks to term out their funding by making covered bonds a more attractive funding source.

Leading industry figures have told The Cover they expect a legal overhaul of the Polish covered bond law to mean increased volumes from the sector, as the reforms should raise LTV limits, allow soft bullets, and mandate minimum OC, according to an exclusive English translation of the text obtained by The Cover. The law change is supposed to encourage Polish banks to term out their funding by making covered bonds a more attractive funding source. -

Banco Popular Español (BPE) returned to the covered bond market on Tuesday to issue only the third Cédulas of 2014, and the issuer’s largest covered bond in three years. Though by no means the most attractive spread seen this year, the triple digit pick-up enticed a broad audience of real money investors.

-

NIBC Bank returned to the covered bond market on Tuesday to launch its second conditional pass-through covered bond (CPTCB). The unreconciled book suggested that the issuer attracted greater scale of demand from a wider group of buyers compared to its first deal. The growing acceptance of this innovative product at a much tighter spread bodes well for future use of this structure.

-

The European Banking Authority (EBA) has acknowledged that Danish and Norwegian banks do not have enough local currency assets to meet their liquidity coverage requirements (LCR). While local currency covered bonds could become a viable alternative, the EBA does not make this recommendation in its latest paper.

-

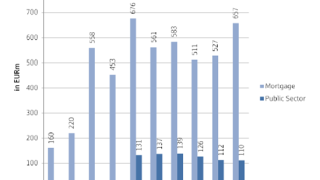

Bayerische Landesbank returned to the covered bond market on Tuesday with a 10 year €500m public sector Pfandbrief, the longest dated issue from Germany this year and highest yielding for its Triple A rating. Despite the borrower’s problems with its Hungarian subsidiary, legal troubles in Austria and the repayment of state aid, the transaction enjoyed a stellar response. It attracted one of the highest oversubscription levels for a German deal, which was testimony to the strength of the Pfandbrief brand and the quality of the issuer’s cover pool.

-

The closer the EU’s bank resolution rules come, the better for the covered bond market, as it is excluded from any possible bail-in plans. But despite the assurances that covered bond investors will escape a bail-in, nobody knows exactly how (yet). Uncertainty remains over covered bonds and liquidity too, with increasingly strident briefing and counter-briefing on whether to count covered bonds in the top class of regulatory liquidity. Owen Sanderson reports.

-

With deleveraging nowhere near finished and loan growth in most European banking sectors sluggish, covered bond bankers are struggling to see an end to dwindling supply and tightening spreads. Tom Porter goes in search of anything that could buck the trend.

-

The bastion of the covered bond market is imposing greater transparency requirements on issuers, but the greater immediate challenge for banks is smooth deal execution in a stiflingly tight spread environment. Joe McDevitt reports.