Covered Bonds

-

Fitch downgraded the ratings of 45 European banks on Tuesday, after it stripped out its assumptions of sovereign support, leaving three Italian banks below investment grade.

-

The European Central Bank has expressed concern about extreme rates volatility. But until it stops buying and allows the private sector to become re-established, its true mission as liquidity provider of last resort will remain in conflict with its determination to expand its balance sheet.

-

NordLB reopened a four year public sector backed Pfandbrief on Wednesday in a move which locked in exceptionally cheap funding. But because the deal was largely placed with captive German savings banks, it offered little clue about the state of demand for euro covered bond benchmarks.

-

The dollar market hosted benchmark covered bond issuance this week as Australia and New Zealand Bank and DNB Boligkreditt issued deals under 144A documentation, in the same size and tenor and at the same spread.

-

Benchmark euro covered bond issuance from a core borrower is expected soon after Rabobank and Swedbank reopened the senior market. Meanwhile, DNB Boligkreditt followed ANZ into the dollar 144A market on Wednesday with a similarly sized deal, in the same tenor and at the same price.

Benchmark euro covered bond issuance from a core borrower is expected soon after Rabobank and Swedbank reopened the senior market. Meanwhile, DNB Boligkreditt followed ANZ into the dollar 144A market on Wednesday with a similarly sized deal, in the same tenor and at the same price. -

The European Central Bank has expressed concern about extreme rates volatility. But until it stops buying and allows the private sector to become re-established, its true mission as liquidity provider of last resort will remain in conflict with its determination to expand its balance sheet.

-

The dollar market continued to sustain covered bonds on Wednesday as DNB mandated leads for a five year, a day after ANZ issued $1.25bn in the same tenor. The Australian bank got better execution than would have been achieved in euros and could have priced even tighter. The excellent result is testimony to the issuer’s long absence and to the depth of demand evident across the dollar fixed income market.

-

NordLB reopened its four year public sector backed Pfandbrief on Wednesday in a move which locks in cheap funding. But the 10bp yield offers little buffer in a market characterised by rate volatility.

-

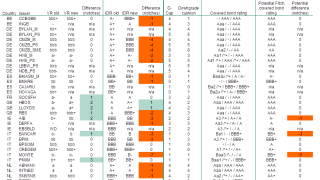

On Tuesday evening Fitch downgraded a swathe of European bank ratings, as it no longer gives any benefit to systemic state support. The downgrades were not expected to have much impact on covered bonds, but a few programmes may be hit. The most extreme case is likely to be Banca Monte dei Paschi di Siena (BMPS), whose July 2024s widened 50p.

-

The Bank Recovery and Resolution Directive was supposed to be universally good for covered bonds because they are excluded from being bailed in. But on Wednesday and Thursday Moody’s and Fitch took opposing views on Allied Irish Banks due to the implementation of their methodologies that take account of the same new regime.

-

The European Central Bank has expressed concern about extreme rates volatility. But until it stops buying and allows the private sector to become re-established, its true mission as liquidity provider of last resort will remain in conflict with its determination to expand its balance sheet.

-

Torrid market conditions have kept issuers away from the euro benchmark market since April 29, forcing borrows to consider alternative currencies. On Tuesday, Abbey printed a £500m three year sterling deal, and even though the deal was not subscribed, bankers felt the sterling market was still open. Separately, ANZ has mandated leads for the second dollar benchmark from Australia this year.