UK

-

Greencoat UK Wind, a British closed-ended infrastructure fund with a focus on wind energy, completed a £260m oversubscribed IPO on Friday, seizing on appetite for UK infrastructure funds.

-

High redemptions, combined with deleveraging and a drive towards deposit funding has put net first quarter covered bond supply in 2013 on track to hit record lows, said Barclays analysts on Thursday.

-

Six UK banks drew £4.36bn between them from the Funding for Lending Scheme, the Bank of England revealed on Monday. Some of the biggest borrowers have also cut lending, according to data released by the BoE. This suggests that net covered bond issuance from UK banks will be negative in 2013, despite higher redemptions due next year than in 2012.

Six UK banks drew £4.36bn between them from the Funding for Lending Scheme, the Bank of England revealed on Monday. Some of the biggest borrowers have also cut lending, according to data released by the BoE. This suggests that net covered bond issuance from UK banks will be negative in 2013, despite higher redemptions due next year than in 2012. -

Sanjay Sofat, regional treasurer for Lloyds TSB in New York, is returning to London to head the bank’s senior funding team.

-

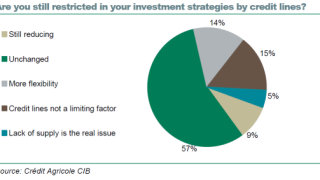

Investor sentiment towards Spain and Italy has improved since August, according to a Crédit Agricole survey. However, most buyers’ credit lines are unchanged, which means many still cannot take advantage of remarkable relative value.

-

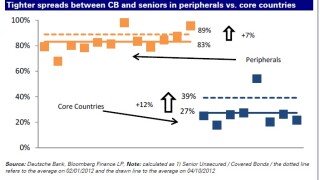

Core covered bonds are performing poorly, with low coupons putting investors off, according to Deutsche Bank analysts. Higher yielding peripheral paper could benefit as a result, but the prospect for fresh benchmark trades from southern Europe remains uncertain.

-

Norddeutsche Landesbank could open books on a debut dollar covered bond as early as Tuesday morning, said syndicate leads on Monday. But the outlook for a first sterling trade from Deutsche Pfandbriefbank is more uncertain.

-

SNS Bank has released guidance for its newly structured Hermes XVIII RMBS, just 15bp wider than where the bank priced a covered bond one month ago. The move follows Yorkshire Building Society’s Brass No 2 RMBS, which last week set the tightest spread for a UK RMBS since the onset of the financial crisis — and a level tighter than where sterling covered bonds trade.

-

OTP Mortgage Bank on Thursday launched the first euro covered bond from Hungary since November 2011, uncovering enough demand to increase a short dated floating rated trade. Meanwhile, National Australia Bank’s recent 14 year sterling offering has widened in the secondary market, after demand proved lacklustre for its attempted long end benchmark.

-

National Australia Bank opened books on an ultra long dated sterling benchmark on Wednesday hot on the heels of Commonwealth Bank of Australia, which became the first non-UK issuer to tap the sterling long end less than a week ago.

-

SSA and corporate markets were busy on Tuesday, keeping the primary covered bond quiet. But issuance should improve this week as investors filter back from holiday, said bankers, though they warned that as spreads have tightened a long way in a short time the market may widen after the initial flurry of deals.

-

After the drama and excitement of UniCredit pricing through BTPs, the European covered bond market has returned to normal — only to be outshone by senior unsecured, where three deals are on the way.