Italy

-

Intesa Sanpaolo has succumbed to perennial investor demand for long dated peripheral issuance from a national champion and issued a €1.25bn 10 year bond. Though the funding margin is slightly negative, it is much better than even three months ago. More importantly, the deal is remarkable for its long duration.

Intesa Sanpaolo has succumbed to perennial investor demand for long dated peripheral issuance from a national champion and issued a €1.25bn 10 year bond. Though the funding margin is slightly negative, it is much better than even three months ago. More importantly, the deal is remarkable for its long duration. -

Banca Monte Dei Paschi di Siena’s secondary covered bond spreads are holding firm following another downgrade, but Spanish spreads are weakening after their recent rally. Peripheral borrowers could still bring successful benchmarks, but compression between covered and senior levels means there is less incentive to use valuable collateral, syndicate bankers told The Cover.

-

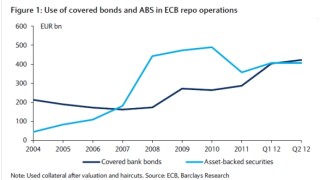

The increase in retained issuance will have a lasting impact on the primary covered bond market and could reduce benchmark supply to ‘showcase transactions’, Barclays analysts warn.

-

Standard & Poor’s cut its rating on another pair of Cédulas programmes this week, but the stellar result for Bankinter and UniCredit showed single-A rated trades can still find a stampeding demand. UK buyers bought more than expected in both deals, as syndicate leads pointed to a new class of accounts that could support peripheral transactions.

-

Bankinter on Thursday swiftly followed peripheral peer UniCredit’s success from the day before. The Spanish borrower launched a blow-out three year benchmark trade 20bp inside initial price thoughts, as traders struggled to keep up with a big spread rally in peripheral paper.

-

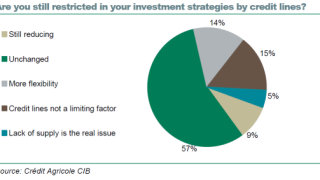

Investor sentiment towards Spain and Italy has improved since August, according to a Crédit Agricole survey. However, most buyers’ credit lines are unchanged, which means many still cannot take advantage of remarkable relative value.

-

Investors are cash-rich and covered bond spreads look set to remain fairly stable – ideal conditions for covered bond issuance. However, deal flow is set to remain quiet as most issuers are well funded, and those that could do deals are about to enter blackout period.

-

Norddeutsche Landesbank could open books on a debut dollar covered bond as early as Tuesday morning, said syndicate leads on Monday. But the outlook for a first sterling trade from Deutsche Pfandbriefbank is more uncertain.

-

Sampo Housing Loan Bank on Wednesday mandated for the sixth seven year covered bond benchmark of September, and should price the trade on Thursday. Despite a renewed appetite for risk in the wider market, covered bond supply remains consigned to safer names, but a successful auction for the Spanish sovereign could pave the way for further Cédulas.

-

Intesa Sanpaolo has become the second issuer to price a deal through its own government, following UniCredit’s historic trade in August.

-

After a six month absence Banco Sabadell returned to the covered bond market on Tuesday with a two year cédulas. Though it looks like the borrower will successfully raise its target €500m in line with guidance, bankers on the deal warned that the depth of demand for peripheral paper had become too thin to realistically consider another deal until after Wednesday’s German court ruling on the legality of the European Stability Mechanism.

-

Three European borrowers mandated covered bond deals on Monday, taking advantage of what could end up being only a brief funding window in the wake of the European Central Bank’s announcement last week that it would support peripheral sovereign debt markets.