Germany

-

Berlin Hypothekenbank has mandated joint leads for a European roadshow to market the first Green Pfandbrief.

-

HVB returned to the covered bond market for its first and only mortgage-backed covered bond benchmark of the year on Tuesday and enjoyed a solid reception. The choice of tenor, deal size and timing all played important roles in the deal’s success.

HVB returned to the covered bond market for its first and only mortgage-backed covered bond benchmark of the year on Tuesday and enjoyed a solid reception. The choice of tenor, deal size and timing all played important roles in the deal’s success. -

The decision to remove Heta exposure from Pfandbriefe collateral pools and add substitute assets has strengthened the position of investors and has demonstrated the importance that the German banking industry places on the reputation of the Pfandbrief product, said Moody’s on Monday.

-

Sentiment improved across the board on Monday, and especially in the covered bond market where Commerzbank issued an oversubscribed seven year tap which it increased from the minimum size during bookbuilding. The increase made a stark contrast to last week’s deals and suggests scope for another transaction on Tuesday. Despite a very supportive technical backdrop, the second quarter outlook is less certain with concern over Greece set to mount, said bankers.

-

Deutsche Bank was awarded the biggest ever single quota for the Renminbi Qualified Foreign Institutional Investors (RQFII) scheme on March 26, its Rmb6bn ($966m) taking the total allocated size of the programme to Rmb330bn at 111 firms.

-

WL Bank can usually be counted on to succeed where others are less fortunate but on Wednesday the German issuer tempted fate with its decision to price a 12 year benchmark. With this deal seven of the last 10 covered bonds have had maturities of 10 years or longer, where demand is more limited and more sensitive to price.

-

Clearstream, the international central securities depository of Deutsche Börse Group, is making further progress in its Asia strategy by opening offshore renminbi cash correspondent bank (CCB) accounts with Chinese banks based in Frankfurt, Luxembourg and Singapore.

-

The euro/dollar exchange rate’s correction following last week’s Federal Open Market Committee meeting provided an ideal opportunity for LBBW to tap its March 2018, Reg S dollar benchmark on Monday. In the meantime, Aktia Bank announced plans to open books on Tuesday for a €500m seven year, which is expected to benefit from Moody’s recent change in its rating methodology.

-

Germany’s Deposit Protection Fund (DPF) will provide a guarantee on the exposure that Duesseldorfer Hypothekenbank (DuessHyp) has to Austria’s Heta Asset Resolution, according to a statement published by the German Association of Banks (Bundesverband deutscher Banken) on Sunday.

-

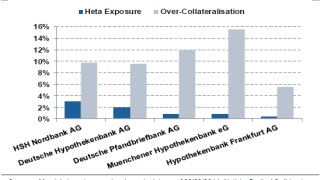

German banks have a larger exposure to Heta Asset Resolution — the bad bank of Hypo Alpe Adria — than Austrian banks, said Fitch on Thursday. Despite this, Fitch thinks losses should be manageable. Research from NordLB, also released on Thursday, shows the distribution of this risk across German Pfandbriefe cover pools.

-

Deutsche Kreditbank closed the spread gap to its higher rated peer, Muenchener Hypothekenbank (Muhyp) on Thursday when it priced a 12 year mortgage Pfandbrief. The ambitious price was justified by the high quality book and comfortable level of oversubscription. Meanwhile Aareal Bank is out with guidance on its first RegS dollar benchmark, which will be priced later today.

-

Fitch put Duesseldorfer Hypothekenbank’s (DuessHyp) BBB- rating on Watch Negative and downgraded its Viability Rating (VR). The bank urgently needs capital, which should ultimately be available from the German government, said the ratings agency. It may be the latest example of the fallout from the Austrian state of Carinthia’s decision not to honour the guarantee of Heta Asset Resolution's unsecured bonds.