France

-

Société Générale was set to price a five year covered bond inside its own curve on Thursday after gathering in €3bn of orders. The deal clearly benefitted from a lack of supply in that maturity this year and comparison with more liquid deals from Belgium this month.

-

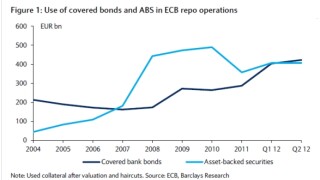

The European Central Bank aims to tighten repo eligibility for covered bonds and has announced a set of rule amendments. Despite some confusion in the interpretation of these changes, the move may reflect a growing concern that covered bonds have overtaken ABS in the ECB's collateral framework.

The European Central Bank aims to tighten repo eligibility for covered bonds and has announced a set of rule amendments. Despite some confusion in the interpretation of these changes, the move may reflect a growing concern that covered bonds have overtaken ABS in the ECB's collateral framework. -

Jean-Philipe Berthaut, BPCE’s deputy chief executive and head of group funding, told The Cover it was a good idea for the French issuer to start 2013 funding with its €1bn seven year covered bond on Wednesday.

-

Dexia group plans to dispose of its French municipal financing entity Dexia Municipal Agency (DMA), it revealed on Thursday, when releasing third quarter earnings. In outlining its new structure, it clarified that Dexia Credit Local (DCL) would no longer be a shareholder.

-

Standard & Poor’s has cut BNP Paribas ratings and lowered its outlook on four other French covered bonds issuers because of rising risk in the French banking system. Meanwhile, Moody’s downgraded CIF Euromortgage’s covered bonds after taking the same action on the issuer.

-

The increase in retained issuance will have a lasting impact on the primary covered bond market and could reduce benchmark supply to ‘showcase transactions’, Barclays analysts warn.

-

Bankinter on Thursday swiftly followed peripheral peer UniCredit’s success from the day before. The Spanish borrower launched a blow-out three year benchmark trade 20bp inside initial price thoughts, as traders struggled to keep up with a big spread rally in peripheral paper.

-

As part of a long term shift in its funding strategy, France’s Crédit Foncier is to start issuing RMBS alongside covered bonds. It is set to begin with a private placement in the coming weeks.

-

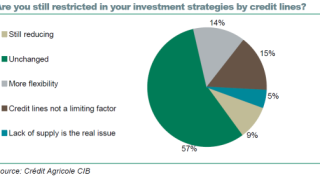

Investor sentiment towards Spain and Italy has improved since August, according to a Crédit Agricole survey. However, most buyers’ credit lines are unchanged, which means many still cannot take advantage of remarkable relative value.

-

Core covered bonds are performing poorly, with low coupons putting investors off, according to Deutsche Bank analysts. Higher yielding peripheral paper could benefit as a result, but the prospect for fresh benchmark trades from southern Europe remains uncertain.

-

Investors are cash-rich and covered bond spreads look set to remain fairly stable – ideal conditions for covered bond issuance. However, deal flow is set to remain quiet as most issuers are well funded, and those that could do deals are about to enter blackout period.

-

French and German covered bonds have outperformed sovereign and agency debt from the same countries, and investors would now benefit from switching out of covered bonds, Barclays analysts have advised. But traders countered that a dearth of new issuance is preventing such profit taking, and will help keep core covered bond spreads tight in the short term.