-

The inchoate additional tier one asset class is highly complex and comes with many risks, and recent volatility shows it may also be prone to panic attacks. One way to help ensure it remains liquid, correctly priced and, most importantly, as stable as possible is to give investors the ability to accurately hedge their AT1 investments. But that doesn't seem likely any time soon.

-

Until you look closely, stress testing sounds great. With the abject failures of the 2011 stress tests fresh in their minds (Dexia has been bailed out twice since passing the test with a 10% capital ratio), the European Banking Authority stress testing teams, and those of national regulators, will pull out all the stops to make the 2014 tests credible.

-

The Securities and Exchange Commission has tried to cut the risk of runs in the money market fund industry by introducing liquidity fees and redemption gates. But as the Federal Reserve has just pointed out, by doing so it has done the opposite of what it intended, and made the funds more like banks.

-

The US Federal Reserve told 11 banks last week that they had failed utterly to draft so called living wills — plans for how they would raise capital in a crisis and how they could be resolved in a hurry if they go under. It was right, they had failed. But the whole concept of living wills is shonky.

-

The UK’s Financial Conduct Authority has decided that if you don’t understand what you are buying, you had better have a lot of money. This week the City watchdog banned the sale of contingent convertible bonds (CoCos) to retail investors for one year, arguing that issuing banks have an “unusually broad discretion” to halt the payment of coupons on the bonds.

-

Russia is now subject to its toughest economic sanctions since the end of the Cold War. With the US and Europe effectively closed to them, Russian borrowers are searching for other options. Asia is top of their list, but they are unlikely to find the support they want.

Russia is now subject to its toughest economic sanctions since the end of the Cold War. With the US and Europe effectively closed to them, Russian borrowers are searching for other options. Asia is top of their list, but they are unlikely to find the support they want. -

Borrowers of the world form a queue, Blog accidentally discovered the world’s greatest funding official this week.

-

As the final moments of the dramatic FIFA World Cup drew to a close on Sunday night — with Germany’s 1-0 victory against Argentina sealing their country’s place in the annals of history as the 2014 world champion — fixed income dealers across Europe were still frenetically tracking down and trading, not bonds but Panini stickers.

-

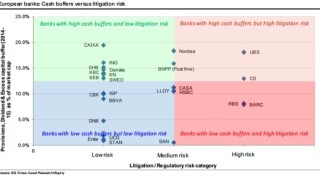

So that’s what a crisis feels like. We’d almost forgotten. European stocks down nearly 4% in the past week, Portugal’s CDS spread shooting from 157bp to 218bp. Banks’ newly minted CoCo tier one bonds dropping three percentage points in a day.

-

More than half a decade after the crisis, one bank has seen fit to make sure its compliance professionals actually know what compliance is and how to be a professional at it.