Euro

-

BBVA has become the first Spanish borrower to smash through the sovereign floor with the imminent pricing of its five year Cédulas Hipotecarias. The deal follows last week’s impressive funding from Intesa Sanpaolo and illustrates the continuing bid for higher yielding secured debt.

BBVA has become the first Spanish borrower to smash through the sovereign floor with the imminent pricing of its five year Cédulas Hipotecarias. The deal follows last week’s impressive funding from Intesa Sanpaolo and illustrates the continuing bid for higher yielding secured debt. -

Intesa Sanpaolo’s €1.25bn 10 year OBG has underscored enormous appetite for risk and has sparked debate over whether the funding door might be open for other smaller issuers from Europe’s periphery and particularly from Italy. However, it seems borrowers that could do deals would rather wait and see.

-

Jean-Philipe Berthaut, BPCE’s deputy chief executive and head of group funding, told The Cover it was a good idea for the French issuer to start 2013 funding with its €1bn seven year covered bond on Wednesday.

-

Given the paucity of euro denominated supply and a lack of issuer diversity, the outcome of Belfius Bank’s — and Belgium’s — first covered bond was always likely to be good. But that should not diminish the extensive efforts the issuer made to address investors’ concerns with well-orchestrated marketing.

-

Standard & Poor’s has dealt a blow to the Dutch covered bond market by downgrading several of its banks’ issuer ratings, chiefly because of the country’s prolonged property market correction. But the move should only have a limited effect on the Dutch covered bond market, say analysts.

-

DNB Boligkreditt made a surprise return to the market on Wednesday, after half a year away, issuing a smaller than usual covered bond and taking advantage of the exceptionally strong funding conditions in the long end, where supply is scarce.

-

Bank of Ireland has priced its first covered bond in three years, attracting a heavily oversubscribed book that was broad and granular. The deal, that many may have considered impossible only a few weeks ago, pays further testimony to the continued bid for higher yielding assets and represents a strong endorsement of covered bonds.

-

Fitch and Standard & Poor’s have given Belfius Bank’s mortgage covered bonds an expected AAA rating for up to €2bn of issuance from its inaugural €10bn programme, ahead of the Belgian issuer’s debut covered deal, which is being marketed this week.

-

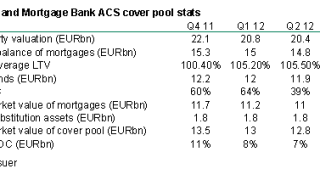

Bank of Ireland Mortgage Bank looks set to reopen the Irish covered bond market and has appointed joint leads for the first Asset Covered Security since the crisis. With Irish government bonds trading inside Spain’s and Italy’s, the deal should get more competitive funding.

-

Sparebank 1 Boligkreditt printed only the second seven year dollar covered bond since 2007 on Wednesday, pricing 2bp inside where Stadshypotek brought the first in September but with a modest new issue premium. Separately, the issuer explained that its covered bond encumbrance was at the lower end of the Norwegian spectrum.

-

Belgium’s KBC Bank plans to issue a covered bond this year, it said on Thursday, following publication of its third quarter results. Meanwhile Belfius Bank told The Cover it was also ready to bring its first deal before the end of 2012. The banks are free to launch the deals after the Belgian central bank gave regulatory clearance last week.

-

Dexia group plans to dispose of its French municipal financing entity Dexia Municipal Agency (DMA), it revealed on Thursday, when releasing third quarter earnings. In outlining its new structure, it clarified that Dexia Credit Local (DCL) would no longer be a shareholder.