Derivs - Equity

-

The Basel Committee has published a final standard for calculating regulatory capital for banks’ exposures to central counterparties, which will take effect on January 1, 2017. The interim capital requirements that were published in July 2012 will continue to apply until 2017.

The Basel Committee has published a final standard for calculating regulatory capital for banks’ exposures to central counterparties, which will take effect on January 1, 2017. The interim capital requirements that were published in July 2012 will continue to apply until 2017. -

Interest in early redemption bonus structures is increasing as investors opt for products with shorter maturities to participate 100% in the positive performance of equity underlyings.

-

Holders of accumulators referencing the China H-share market are seeing immediate benefits from a plan to tie the Shanghai Stock Exchange more closely with the Hong Kong Exchange.

-

Philippe El-Asmar, head of global equities distribution and head of distribution Asia Pacific at Barclays in Hong Kong, will leave the firm at the end of April.

-

UBS has seen its exchange-traded note program assets more than triple in less than 18 months. The program had approximately USD1 billion at the end of 2012 and now has USD3 billion.

-

Paul J. Andersson, the ex-managing director and global head of pan-Asian equity derivative and convertible sales at Citigroup in Hong Kong, has joined Mizuho Securities.

-

Institutional investors in France, Italy and Switzerland are increasingly showing interest in structured notes on volatility target underlyings, driven by current low yields in fixed income markets and attractive OTC budgets.

-

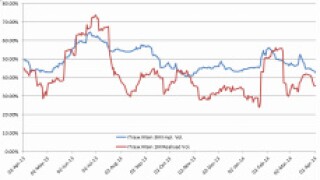

German asset managers are rolling credit default swaps on single names in the iTraxx Main into longer dated maturities to gain from the steepness of the curve.

-

The China Financial Futures Exchange plans to introduce a China volatility index and launch futures and options trading on it once the bourse completes the introduction of CSI 300 options later this year.

-

Total trading volume in VIX futures during March 2014 increased 20% year-on-year, according to data from the Chicago Board Options Exchange.

-

Credit Suisse has launched structured notes on its Risk Appetite HOLT Relative Value USD Index. The so-called ProNotes offer investors 100% participation in the positive performance of the underlying.

-

Total cleared contract volume in equity options and futures in March 2014 increased 14% year-on-year, according to data from the Options Clearing Corporation.