In the middle of November 2017, high yield bond markets suffered a brief sell-off that resulted in a spate of deals being pulled. It was a stark reminder of the volatility those eponymous high yields were supposed to compensate investors for. This year could see a lot more market spasms as central banks start to close off the supply of cash that has driven years of a come-one, come-all approach in capital markets.

The US Federal Reserve has committed to unwinding its $4.5tr portfolio of assets acquired through quantitative easing (QE) — a process which began in October — and the European Central Bank will start to taper its own €2tr programme in January from €60bn a month to €30bn.

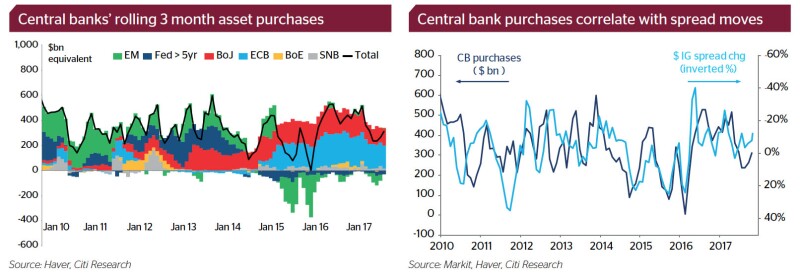

That change in the global pace of QE — a reduction of $48bn a month from the G4 central banks this year, according to BNP Paribas analysis — could threaten the long rally, into which issuers can seemingly sell what they want at ever tighter prices, that has come to define the QE era.

When that will happen is uncertain. But a consensus is forming that conditions will change in the coming year. “When the tipping point comes is not predictable, but it is highly likely it will occur in the next six months,” says Louis Gargour, founder and senior portfolio manager of LNG Capital.

How severe any shake-out will be in London is also unclear. The market has experienced volatility around QE tapering before, when the Fed first talked of tapering in 2013. But the world is different now. QE has crushed yields in all asset classes, forcing investors into new markets, or to look further down the credit spectrum and along the yield curve to earn returns. Similarly, the benign markets that QE and an era of cheap credit have created have increased the amount of money put into passive products that track an index rather than pick out individual credits.

BNP Paribas estimates that €1.3tr has been moved from euros into dollar products since the collapse of yields in euros in 2015 when the ECB began its QE programme.

“In particular there has been a very strong correlation between ECB and Bank of Japan balance sheet deployment and inflows into emerging markets,” says Robert McAdie, global head of strategy research at BNP Paribas.

Speed or size?

QE, according to central bankers, was intended to stimulate growth and inflation. It has certainly inflated asset prices, as almost any chart of bond yields over the past few years will tell you. But a disagreement between those central bankers and those in the markets is at the core of what happens next.

Central bankers and economists believe assets are expensive because economies are good, so a fall in QE will not lower their price. They think it is the total amount of QE that is important, rather than the pace.

But analysis from at least two banks spoken to for this article suggests that the pace has more influence, rather than the total stock of bonds central banks hold.

“We saw high correlation between the pace of G4 QE purchases and asset price rises; it was highest in high yield and emerging markets assets, then equities, then mortgage-backed securities,” says McAdie.

Matt King, global head of credit products strategy at Citigroup in London, agrees. “Markets are expensive because of an incredibly strong technical bid hoovering up all supply. There is a strong correlation between central bank purchases each month and asset prices.” Indeed, King wrote in November, “...what really disturbs us is how dismissive central bankers are of the [high correlations between QE flows and asset prices]. Several tell us they have shown them to monetary policymakers, but they are dismissed as ‘not fitting with the theory’...” No tantrums

If volatility is to rise as QE slows, what will that volatility look like? The nature of the risk of volatility has changed since the ‘taper tantrum’ of 2013 when Ben Bernanke spooked markets by reminding them that QE would one day end. As more investors have put their cash into passive funds, so more participants have similar positions and incentives, meaning it is less likely there will be enough buyers when the need to sell arises. “Day-to-day volatility is low,” says King, “but there is increased tail risk.” “A decrease in bond buying will not be down to a central bank communication problem like with the US taper tantrum,” says Gargour. “There will be a tipping point when everyone wants out of fixed income at the same time because they think they are not being adequately rewarded for the risk they are taking.” What will lead to that tipping point is not known but old favourites, such as geopolitics, seem to have lost their ability to scare, if 2017 was anything to go by.

If markets are awash with so much cash that they must invest regardless of geopolitical disruption, what of the sources of that money: the central banks themselves?

The Fed’s talk of tapering QE in 2013 shut some markets down entirely. But, as Gargour alludes to, the clarity of central banks’ forward guidance over monetary policy means there are likely to be few shocks at their future press conferences.

Instead, inflation is earmarked most often as the source of concern. If expectations of it rising increase quickly, then volatility will rise in tandem. “Spot and forward expectations of inflation are low,” says Sean Taor, RBC Capital Markets’ head of European debt capital markets, “but it won’t take much to knock that confidence.” “We think euro inflation will push higher and that market expectations of inflation will increase,” says McAdie.

Higher inflation expectations will make asset prices less attractive just as the central bank bond buying supertanker changes tack.

Citi data shows that net bond issuance — new issue supply less central bank purchases — has reached about zero. This year, Citi expects net supply to be about $1tr. It was about $4tr in 2007.

Fundamentally sound?

Central banks will hope their theory of solid fundamentals holds. “If the economic fundamentals have driven the rally, there should be no market vulnerability,” says King. “But if investors have been forced to buy at yields they didn’t like, then markets are more vulnerable.” Investor inflows into capital markets have forced more money into all sorts of assets — particularly corporate ones — regardless of the idiosyncrasies of particular credits or sectors. That possibly contributed to the situation last October when Italian supermarket chain Esselunga was able to issue bonds at a rate lower than the Italian government.

There is a feeling that central bank policy has stood in for, or supported, economic recovery. Investors have bought every dip knowing that there is a strong central bank buyer lurking about in the background with a ready bid. This year, the fundamentals will have to fend for themselves more.

That projection is not contentious, but what the market reaction will be is. At least no one is expecting markets to take a bath — if they did, central banks would surely intervene.

“There is only fear of investors underperforming in a continued rally,” says King, “not of losing money outright.”

Nonetheless, a reckoning could be approaching for all those who invested blindly. For just as QE unwinds, credit terms are loosening.

“Net debt-to-Ebitda in dollars is up at 2003 levels,” says McAdie. “Spreads should widen. There will be greater credit dispersion, with default rates up by about 1%. This is more likely to occur in consumer-related high yield sectors.” That means more idiosyncratic credit risk and more credit analysis needed, which will deter the ETF buyers and other investment tourists who have squeezed in alongside sector specialists to crush bond yields.

“It is non-dedicated investors — the private banks, high net worth individuals — who have invested via ETFs that are creating the most risk, due to the size of their investment relative to the underlying liquidity of the asset class,” says Gargour.

“There is risk in investment grade assets and in government bond yields,” says McAdie. “They are susceptible to outflows of tourist money that has flowed in.”

But the effect on yields of any tourist exodus will be tempered by sector specialists who see a buying opportunity. Similarly, selling of long-dated assets will suit insurance companies and pension funds with long-dated liabilities to fund.

Trickier course

Within corporate debt, it is the riskier end of the credit spectrum that is the worry for this year, once the pace of QE slows. “I am more concerned about the lower rated, higher risk assets — the ones that have moved the most during the QE era,” says Taor. “Valuations do not reflect the risk.” With regard to just how rich valuations have become, the end of November saw a case in point as Nordea — admittedly a highly rated bank — sold additional tier one capital at a record low coupon for the product. Nordea paid just 3.5%, beating the previous record for the product by a full 1.25%.

But the feeling is that there will be no violent reactions as QE slows — there is simply too much money in the system that needs to be invested. As investors will need to differentiate between credits, so the sell-side will have to be more discerning when bringing deals. “If there is a revaluation of asset prices,” says Taor, “then the change in sentiment will make windows of opportunity for issuance harder to spot.”