Covered Bonds

-

The European Commission (EC) could be ready to lift the amount of covered bonds that can be used to fill Liquidity Coverage Ratio (LCR) requirements from a maximum of 40%, to a new higher limit of 60%, according to head of the Danish Mortgage Bankers Federation. The outcome could be known within a few days.

-

Dexia Kommunalbank is expected to return to the market for the first time in three years, following an announcement on Monday that the Pfandbrief issuer will conduct a roadshow starting in two weeks. The marketing exercise follows the publication of its end of year results in which the state-owned entity articulated its orderly wind down plans, which benefit from a large and unused liquidity facility

-

Credit sentiment is positive, and it seems unlikely that the European Central Bank would take anything other than an accommodative stance at next week’s policy meeting, but bankers are getting cautious that valuations are becoming overstretched, particularly in those markets which have until now been considered safe havens.

-

Compagnie de Financement Foncier (CFF) came to market with its second Obligation Foncière of the year on Tuesday, matching the previous deal’s €1bn size — but this time in a 10 year maturity, rather than five year tenor.

-

Bank of Montreal became the sixth Canadian bank to issue legislative covered bonds when it sold its first deal in the format on Tuesday. The transaction was priced at the tight end of the range of Canadian deals and encountered some price sensitivity but was still comfortably oversubscribed.

-

Italian banks' repayments of liquidity drawn under the European Central Bank’s long-term refinancing operation (LTRO) have been slower than in most other European countries, said Fitch on Wednesday. Analysts say Italy’s smaller banks are going to be increasingly incentivised to term out European Central Bank liquidity with publicly syndicated covered bond issuance, but with stress test results due in October, time is running out.

-

The forthcoming covered bond criteria change from Standard & Poor’s is unlikely to result in a substantial modification in credit ratings, bankers said. Covered bond ratings should improve relative to senior unsecured ratings, but senior unsecured ratings may fall as the rating advantage of sovereign support is removed.

-

The conditional pass through covered bond (CPTCB) has potential to become more widespread, said bankers in the aftermath of Moody’s detailed overview of the structure that was published this week. They noted that a new issuer is currently considering employing the structure, backed by a varied pool of international assets.

-

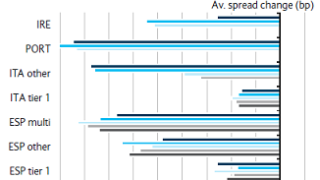

The more modest year-to-date tightening of Irish covered bonds relative to other peripheral jurisdictions has created a value opportunity, says Barclays research, which recommended buying Irish covered bonds versus Irish government bonds. However, traders say limited liquidity in the secondary market for peripheral names means that the trade idea will be difficult to executive in practice.

The more modest year-to-date tightening of Irish covered bonds relative to other peripheral jurisdictions has created a value opportunity, says Barclays research, which recommended buying Irish covered bonds versus Irish government bonds. However, traders say limited liquidity in the secondary market for peripheral names means that the trade idea will be difficult to executive in practice. -

Jochen Hartlieb has joined IKB Deutsche Industriebank from Bayerische Landesbank.

-

After issuing its second covered bond of the year on Tuesday, Crédit Foncier de France is set to return to the capital markets and fund its residential mortgages with an RMBS, the first sale of the product from France since 2006. But in contrast to covered bonds, the RMBS is driven by capital considerations with the leads confirming that the issuer intends to place all of the subordinated notes.

-

Italian banks' repayments of liquidity drawn under the European Central Bank’s (ECB) long-term refinancing operation (LTRO) have been slower than in most other European countries, said Fitch on Wednesday. Analysts say Italy’s smaller banks are going to be increasingly incentivised to term out ECB liquidity with publicly syndicated covered bond issuance, but with stress test results due in October, time is running out.