Covered Bonds

-

Yorkshire Building Society issued its first euro issuance in four years and the second only UK deal in euros on Wednesday. Bankers said it offered a generous spread to fellow UK names but that it was justified.

-

BBVA returned to the covered bond market for the first time in more than a year on Wednesday with a 10 year Cédulas that attracted 115 investors into the book. The coupon paid was the lowest ever for a 10 year in the history of the Spanish market.

-

Yorkshire Building Society issued its first euro issuance in four years on Wednesday morning, a deal that bankers said offered a generous spread to fellow UK names.

-

OP Mortgage Bank returned for the second time this year on Wednesday to issue a €1bn five year covered bond. Though it was the tightest spread for a Finnish transaction seen in the last five years and priced with a negligible new issue premium, it still attracted a robust level of oversubscription.

-

BBVA returned to the covered bond market for the first time in over a year on Wednesday with a 10 year Cédulas that attracted a fairly granular book. The coupon paid was the lowest ever for a 10 year in the history of the Spanish Cedulas market.

-

Banco Santander Totta surprised the market on Tuesday, announcing a mandate and setting initial price thoughts for a new five year benchmark of undetermined size.

-

The widely anticipated public sector-backed Pfandbrief from Dexia Kommunalbank on Tuesday had been expected to go well, given the juicy spread that was likely. But the level of oversubscription was the highest of any German deal this year and even put competing issuance from Portugal into the shade.

-

Danske Bank’s first covered bond of the year offered an attractive spread relative to its Nordic peers, which made it a relatively straightforward sell. But even so, the final level was just one third of Danske’s differential against Sweden a year ago.

-

Danske Bank has mandated joint leads for a euro seven year benchmark, which is expected to be priced on Tuesday. The Danish bank had been expected to make a deal announcement some time ago, but decided to hold back after some tightly priced core covered bond deals failed to garner a sizeable book.

-

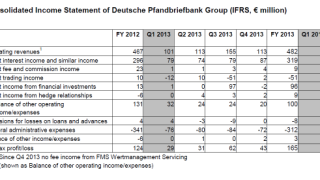

Deutsche Pfandbriefbank (Pbb ) reported a 31% pre-tax rise in profit on Monday, boding well for its privatisation — in marked contrast to Depfa plc. Pbb has launched two Pfandbrief deals this year and is likely to return to markets at least once and possibly twice this year, it confirmed to The Cover on Monday. For the time being, however, the covered bond market is expected to trade sideways as participants await news from the European Central Bank.

Deutsche Pfandbriefbank (Pbb ) reported a 31% pre-tax rise in profit on Monday, boding well for its privatisation — in marked contrast to Depfa plc. Pbb has launched two Pfandbrief deals this year and is likely to return to markets at least once and possibly twice this year, it confirmed to The Cover on Monday. For the time being, however, the covered bond market is expected to trade sideways as participants await news from the European Central Bank. -

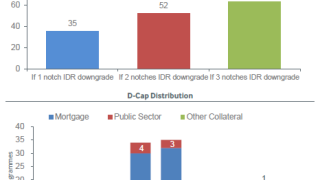

The ratings of covered bonds programmes could withstand a downgrade of the issuer’s rating by two notches on average, up from one notch in mid-March, said Fitch on Monday. But that analysis follows a Moody’s announcement in which it placed 81 European banks on negative outlook due to “systemic support for unsecured creditors being increasingly at risk” following the implementation of the Bank Recovery and Resolution Directive (BRRD). The upshot is that an improved covered bond rating cushion may prove to have little effect on covered bond ratings as issuer ratings are more likely to be downgraded.

-

Non performing loans in multi-Cédulas deals are continuing to rise according to Moody’s. And Bank of Spain data released last week showing that the trend maybe levelling off, understates the actual level by as much as half. See The Cover's interactive chart for more.