Covered Bonds

-

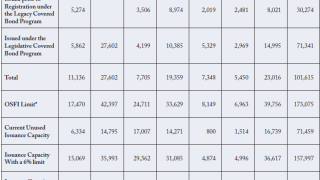

The Canadian covered bond issuance cap of 4% of total bank assets is lower than most other countries and should be raised, according to Finn Poschmann at independent Canadian research institute, C.D. Howe.

The Canadian covered bond issuance cap of 4% of total bank assets is lower than most other countries and should be raised, according to Finn Poschmann at independent Canadian research institute, C.D. Howe. -

Banca Popolare di Milano (PMIIM), has mandated leads to market a covered bond from its newly structured shelf, which is rated A2 with Moody’s only.

-

Danish covered bond auctions this week attracted strong demand, especially in the five year tenor where yields are double what is available in the eurozone.

-

Banco Popolare (BPIM) has obtained the approval of investors to remain the account bank on its own covered bond programme, even though this will result in those covered bonds being downgraded to a sub-investment grade rating.

-

Standard and Poor’s has implemented its new rating method for Spanish multi-Cédulas programmes and announced a series of rating upgrades, downgrades and affirmations on the 32 deals it rates. The rating action should lower capital charges on some weaker deals.

-

The Danish summer auctions, which began on Monday, have attracted very good interest, especially in the five year tenor, which looks attractive on an outright yield and spread basis, particularly compared to what is on offer in the eurozone.

-

Depfa ACS Bank has only one rating remaining after Standard & Poor’s became the second agency to withdraw its covered bond rating this week. Analysts suggest this could result in forced selling of Depfa’s covered bonds if Moody’s follows suit, but they still believe that the bonds will be paid out in full.

-

Austrian covered bonds have been largely unaffected by the reinstatement of the State of Carinthia’s guarantee and the ensuing downgrade by Moody’s of the state to B3, according to analysts at LBBW.

-

Credit Suisse has bulked up its covered bond team with a new hire who will join FIG syndicate.

-

Banco Popolare has obtained the approval of investors to remain the account bank on its own covered bond programme, even though this will result in those covered bonds being downgraded to a sub-investment grade rating.

-

The Bank of Scotland has become the first bank to not win approval to switch some of its covered bonds from a hard to a soft bullet repayment.

-

The Dutch mortgage market, one of the largest in Europe, could be poised for radical transformation that stands to change the way loans are originated and funded. Bill Thornhill reports.