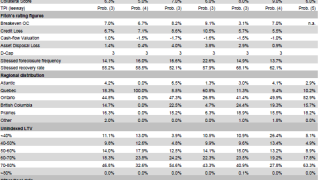

Canada

-

Royal Bank of Canada has priced its first Australian dollar covered bond of the year and the second in that market this year. The funding was close to what it could have achieved in US dollars and demonstrated the ability of the Kangaroo market to be strategically relevant to the global funding programmes of financial institutions, said RBC.

-

Toronto-Dominion Bank was set to price the first sterling denominated Canadian three year covered bond on Friday, which will be the seventh sterling covered bond this year and the third deal from a non-UK name. It is also the largest sterling deal issued by a bank outside the UK.

-

Bank of Nova Scotia was set to price the tightest and longest Canadian covered bond issued in euros on Wednesday. It was also the tightest spread for any non-German seven year seen this year, and at €1.5bn the largest in that tenor.

-

Nearly a year after registering its covered bond programme with the US Securities and Exchange Commission, Canadian issuer Bank of Nova Scotia filed its prospectus. The move is a likely precursor to a dollar issue.

-

Toronto Dominion’s first legally compliant covered bond stormed the market on Monday morning, raising €1.75bn – €750m more than any of the other five Canadian euro benchmarks that have been launched this year.

-

Toronto Dominion and BNP Paribas should be ready to launch the Canadian bank’s first legally compliant covered bond next week after announcing the prospective deal on Wednesday. The announcement was not a total surprise, given that the bank’s programme had been signed off by the regulator in late June. However it has removed uncertainty over timing, which bankers away from the deal commended.

Toronto Dominion and BNP Paribas should be ready to launch the Canadian bank’s first legally compliant covered bond next week after announcing the prospective deal on Wednesday. The announcement was not a total surprise, given that the bank’s programme had been signed off by the regulator in late June. However it has removed uncertainty over timing, which bankers away from the deal commended. -

Canadian Imperial Bank of Commerce recently updated its covered bond prospectus, giving rise to speculation that it could return to the covered bond market this year. CIBC is only one of two Canadian banks that have not issued in euros in 2014 and was last seen in the market in July 2013.

-

Toronto-Dominion Bank could become the next Canadian bank to issue a covered bond after it received regulatory approval from the Canada Mortgage and Housing Corp (CMHC) this week. The sign off comes weeks after Canada set out guidelines on the liquidity coverage ratio.

-

Royal Bank of Canada opened books on Thursday for its keenly anticipated inaugural covered bond of 2014. The deal builds its euro curve and establishes RBC as the benchmark Canadian issuer in euros. Though wider than its last five year, the 0.75% coupon was 0.5% below its last funding in this duration and shows the impact of the ECB's recent action.

-

Royal Bank of Canada could be ready to return to the euro covered bond market for the first time this year after emerging from blackout last week. It is one of only two Canadian borrowers that has not issued a euro benchmark this year, while Danske Bank’s research team believes Canadian issuance is set to pick up.

-

The Bank of Montreal (BMO) became the sixth Canadian bank to issue legislative covered bonds when it opened books for its first legislative deal on Tuesday. The transaction was priced at the tight end of the range of Canadian deals and encountered some price sensitivity but was still comfortably oversubscribed.

-

Bank of Montreal’s (BMO) covered bond programme was recently signed off by the Canadian Mortgage Housing Corporation (CMHC), giving rise to speculation that it could return to the covered bond market after Easter with a newly set up programme and a legally compliant covered bond deal. A still-favourable cross currency swap suggests it could become the fourth Canadian bank to issue in euros this year.