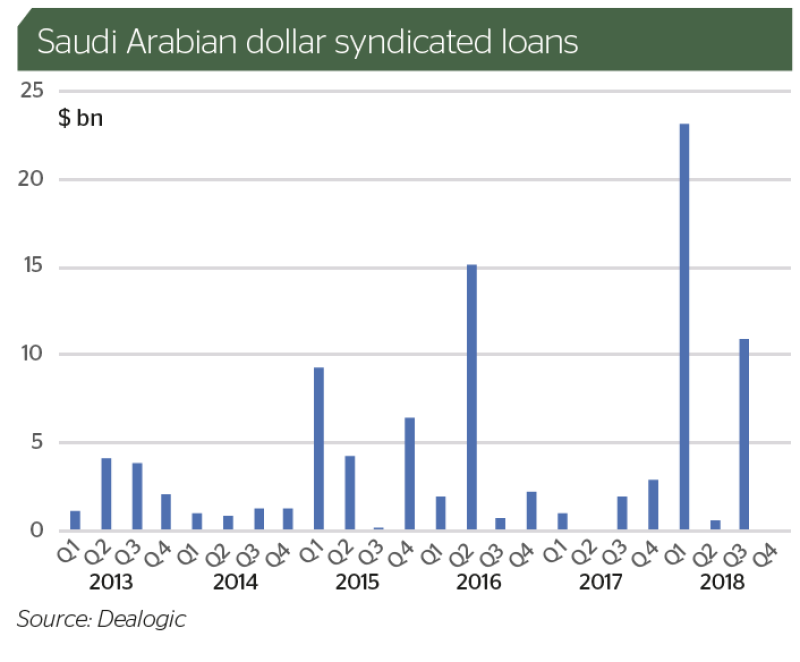

Few countries have burst on to the world stage in as a spectacular a way as Saudi Arabia has over the last year in the syndicated loan market. Borrowers in the Kingdom signed loans totalling a record $37.2bn in 2018 — almost half the $83.9bn of loans in the whole Middle East region in the same period. Remarkably, the country became the 15th biggest syndicated loan market globally in dollar terms, just behind Singapore and Hong Kong, according to Dealogic.

Such an appetite to borrow has delighted banks, which otherwise have had slim fare to live on. Syndicated lending in EMEA ex-Middle East (in which 97% of volume is in the six Gulf Cooperation Council countries) fell in 2018, and many loans desks missed their year’s budgets by around 20%.

“Saudi Arabia has contributed significantly to volumes this year — next year will likely be more of the same,” says Nicholas Voisey, managing director of the Loan Market Association (LMA) in London. “The MENA region remains attractive for lenders because of reduced activity in other countries and regions such as Russia and Africa.”

The LMA held its second Middle East syndicated loans conference in November, and attendance was well up on the previous years. Anecdotal perhaps, but indicative of banks’ growing interest in the market.

Despite the big volumes, it has not all been plain sailing in the region. There have been some major incidents that are widely regarded as having delayed even bigger lending to Saudi. Banks had been eagerly anticipating a $50bn loan for the national oil company Saudi Aramco to finance its acquisition of a majority stake in Sabic, the petrochemical firm, from the sovereign wealth fund Public Investment Fund (PIF). But the loan was postponed after Saudi Arabia was internationally condemned for the murder of journalist Jamal Khashoggi at its Istanbul consulate in October.

“It made lenders stop and think,” said a senior loans banker at a bank that is a relationship lender to Saudi. Lenders repeatedly decline to go on the record when discussing Saudi, pointing to the sensitive nature of the claims against the state and the expectation of lucrative business in the pipeline.

“Economically,” the senior banker continued, “it still makes sense to lend to Saudi, so I’m sure any deals being discussed will be achievable, but it made it tough to move forwards with business for a little while.”

Bastion of bonds

It is not just loans desks that have been dependent on Gulf business. The Middle East has never been as important to the CEEMEA bond market as it was in 2018. With two regular issuers — Turkey and Russia — on ice because of political problems that have provoked sanctions from the US, the Gulf has seemed this year to be an island in stormy waters.

The GCC has accounted for $72.8bn of bonds printed in 2018 up to late November, 42% of the $173bn total in CEEMEA. That is the highest ever proportion, though the volume of GCC paper was actually lower than in 2017.

That readjusting of the balance of business has been partly responsible for a shuffling of banks at the top of the CEEMEA league tables this year. For example, according to Dealogic, Standard Chartered was seventh for CEEMEA bonds in 2016, fifth in 2017, and in 2018 rose to second.

As a bank that does not focus on central or eastern European clients, it has, and continues to be, slightly unfair to point to Standard Chartered’s position in the CEEMEA league tables as a measure of its success compared to its peers. But the fact that it does not do this business but is still second placed points to the boost in volumes from the regions it concentrates on. Standard Chartered’s stellar rise up the league tables has been because of its dominance of the Middle East business — in a Dealogic table of GCC issuance this year it is top, with an extraordinary 16% market share.

While it is inevitable that other banks will try to nip at its heels, Standard Chartered says it is not yet seeing evidence of increasing competition, through either fees or lending.

“Every major bank is already set up in the GCC, so there haven’t been any major changes in the competitive landscape this year,” says Khalil Belhimeur, executive director, bond syndicate for EMEA at Standard Chartered Bank in London. “There are of course some banks that have deeper relationships with clients, so there is some differentiation. GCC fees tend to be in line with other EM jurisdictions, so I can’t see that reducing, especially as GCC issuers do demand a certain level of credibility from their bookrunners.”

Pricing to stay tight

The link between lending and bookrunning a bond remains strong in the region, and can be seen in the pricing dynamics of some of the major loans signed.

Saudi Arabia, for example, signed its $16bn five year conventional and Islamic loan in March at a margin of 75bp over Libor. PIF followed just after the summer with its own $11bn deal at the same margin. Those funding costs partly reflect banks’ desire to be close to the borrowers.

“If you lend, you’ll be invited to pitch for a bond and you’ll be given an opportunity to sit at the table,” says Belhimeur. “But it doesn’t necessarily mean you’ll be put on the trade.”

Even without the carrot of potential bond mandates, however, the huge amount of demand to lend in the Gulf’s loan market means borrowing costs are likely to stay low for the foreseeable future. “Money needs to be put to work and this will keep terms competitive,” says Voisey at the LMA.

Cash available to lend is only set to rise in the region, with a technical bump that is expected to bring in billions of dollars. Saudi Arabia, Qatar, the United Arab Emirates, Bahrain and Kuwait will become eligible for the JP Morgan emerging market government bond indices, starting from January 31, 2019. Oman is already in. That will trigger automatic investment from passive investors that track the indices. Bank of America Merrill Lynch estimated there would be around $30bn of inflows into the region’s debt as a result.

“The Middle East is likely to be an outperformer next year, given the upcoming inclusion of the GCC into the JP Morgan EMBI index family,” says Nick Darrant, head of CEEMEA syndicate at JP Morgan in London.

But with many funds able to front-run the change, investors say the effect on spreads is likely to be limited next year.

“It’s been known for a while that it’s going to happen, so a lot of funds are prepared and positioned for it,” says Okan Akin, corporate credit research analyst for CEEMEA at AllianceBernstein in London. “A lot of that effect will be offset by the massive volume of bonds expected from the Middle East in the first quarter — we expect that about 50%-60% of the total volume for the year will get done in that quarter.”

Oiling the markets

The markets in the region are intimately linked to the price of oil, which rose as high as $86.29 a barrel for Brent Crude in October, before selling off sharply, largely because of rhetoric from US president Donald Trump about what he considers to be high prices. Brent Crude was trading at $59.38 a barrel on November 29. Analysts at the LMA conference reckoned oil would trade at $70-$90 in 2019.

“The thing about this part of the world is that the markets are so correlated to the oil price,” said the head of loans at a Gulf lender. “If it strays lower, it will put more pressure on fiscal budgets, whereas if it goes higher it will encourage more investment that requires financing. The whole sentiment next year will be down to where the oil price is.”

For new debt issuance, this could go both ways, as although investment might be put on hold if oil is cheap, Gulf sovereigns will need to make up the oil revenue they are missing out on by borrowing money.

“Some sovereigns have felt that they didn’t need to issue in 2018 because the oil price was high,” says Akin, “but with oil down at $50 a barrel, that changes.”

Bond bankers expect volumes in 2019 to be similar to 2018 or marginally higher. Some sovereigns — which typically issue jumbo multi-billion dollar bonds each time they tap the markets — did not issue in 2018, such as Kuwait and Abu Dhabi. They are expected in 2019.

Local bid convergence

One dynamic that seem to be weakening, though, is the traditional willingness of local investors to buy bonds at levels well inside where international investors are comfortable.

“Local banks have been feeling more full on risk,” says an EM syndicate manager in London. “We’re not seeing the local banks anchor trades as much as they were before. Towards the end of this year we were seeing levels creep wider and leads on some new issues weren’t able to move guidance much.”

The head of debt capital markets for the region at one bank says: “Local demand is getting smarter and they’re not running out to buy everything any more. Local accounts don’t want to be offering to buy at levels 20bp inside where the internationals are buying — there’s been a convergence with international investors on price. If they are willing to buy a tightly priced bond, they’re putting in much smaller tickets.”

The widening of bond spreads has not yet made much difference to the loan market, which is traditionally encumbered in its response to pricing fluctuations. However, there is growing pressure for this to change.

“There is a significant gap between where people price loans and where they price bonds,” says the head of loans at the Gulf bank. “I don’t know how long that can be sustained.”