The Middle East faces a very tricky, even dangerous, 2018 — but you would not know it from its debt markets. War rages in Yemen. Qatar and its neighbours are at loggerheads, in an inter-Gulf feud without precedent. Saudi Arabia is purging its princes. And who knows how bad the strife between Saudi and Iran could get?

But bond and loan markets are placid. Volatility in Middle Eastern markets has increased, but few capital markets players seem to care. Some are even unsure whether recent events such as those in Saudi Arabia and Qatar are moving bond and credit default swap prices, or whether the Middle East is simply moving wider with the EMBI Global as emerging market volatility globally increases.

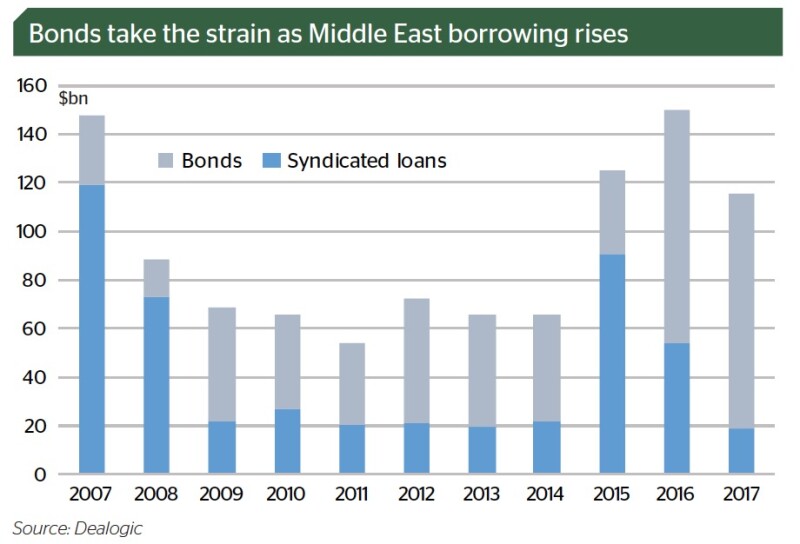

For investment banks active in the region, there is good news: overall borrowing in the region in 2017 came in at a much higher level than before the oil price fell in 2014. The feeling across the capital markets is firmly that although the region poses risks, it is also rife with opportunities for 2018.

All change for Qatar

One country where that optimism might not be so high is Qatar. This marks a significant change from five years ago when, in 2012, pink champagne regularly flowed in the City of London’s pubs in honour of the likes of Qatar and state-owned property developer Qatari Diar drawing order books in excess of $25bn — numbers which at the time were unheard of for EM bond deals.

Fast forward to the early days of 2018 and the political turmoil in the region has reined in debt capital market bankers’ enthusiasm about Qatar, once the jewel of the Middle East capital markets.

On June 5 last year, Saudi Arabia, the United Arab Emirates, Bahrain, Yemen, Egypt and Libya cut diplomatic ties with Qatar and installed hard-hitting sanctions over allegations of the emirate’s links to terrorist groups. That put debt markets in a quandary. Banks were unsure whether taking part in bond and loan deals for Qatari entities would affect their relations with their clients on the other side of the argument.

“There was a period over which banks didn’t know whether explicit support for Qatari borrowers would be negatively perceived by other regions in the GCC [Gulf Cooperation Council],” says a loans banker from a US bank. “Qataris also didn’t want to set a new price benchmark with the new perceived risk, so we haven’t seen anything in the loan market to come out of Qatar since.”

Qatari bond issuance has also shut down. But in mid-December a thaw appeared to be beginning, as Qatar National Bank and Commercial Bank of Qatar approached the international loan market.

Spreads up on squabble

But with Saudi and UAE banks not coming into loans or bonds for Qatari issuers, levels for new deals will probably be wider. “In the past Qatar has benefitted from regional demand for the UAE and Saudi,” says one head of DCM in Abu Dhabi. “That was important, not just in the selling of bonds in the primary market, but also the provision of a secondary market — international investors knew that at crisis points there would always be a bid for that paper at a good price.”

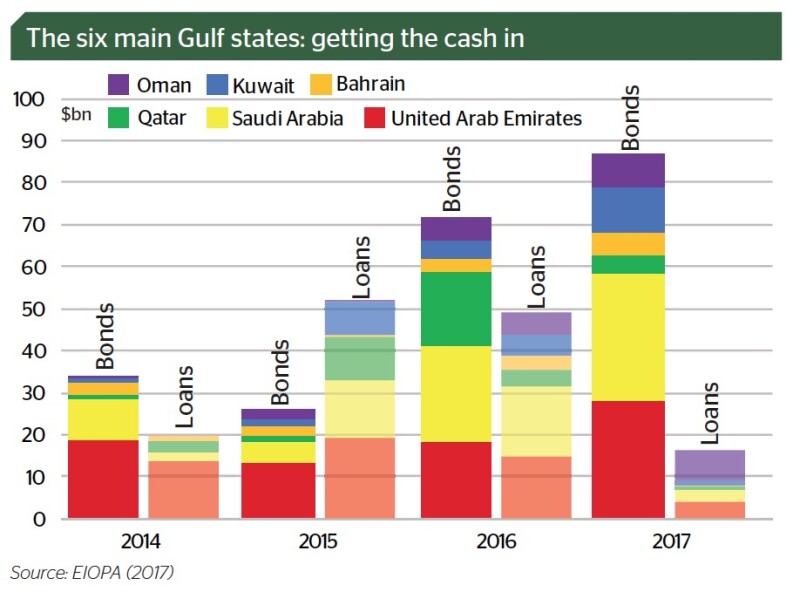

There had been much talk throughout 2017 of whether international banks would even be willing to arrange bonds for Qatar and its issuers, knowing they could incur the wrath of the UAE and Saudi Arabian governments for doing so. Up to November, Qatari entities had issued about $5bn of bonds in 2017, according to Dealogic. The top three bookrunners for bonds from that country were Standard Chartered, HSBC and JP Morgan. Meanwhile, Saudi Arabia, the UAE, Bahrain and Egypt accounted for $83bn of issuance, with the top three bookrunners JP Morgan, HSBC and Citi.

But increasingly banks seem to be brushing those concerns aside. Fadi Abu Aitah, treasurer at International Bank of Qatar, says international banks have been courting the bank as much as ever before, although its need for international funding appears to be low.

“Banks are still calling, visiting and marketing different products to us, but because our asset growth had slowed even before the summer, we are not much in need of this financing,” says Abu Aitah.

Getting back to normal

Indeed, now that the initial shock has died down, bankers in both the bond and loan markets are more optimistic about Qatar’s funding capability this year.

“People are more comfortable with the idea that you can do deals with both sides without marginalising the other,” says the loans banker from the US bank.

Raouf Jundi, head of loan origination at MUFG in London, agrees.

“I am confident Qatar will find a way to finance in the capital markets, as banks are taking the view that it is an inter-regional affair,” says Jundi. “Banks value stability and the country remains stable.”

Outside Qatar, DCM bankers are looking forward to a crop of corporate bonds appearing in 2018, which investors are eagerly eyeing in the hope of being offered higher yields than are available on the sovereign trades that have dominated the market over the last two years.

“The sovereign supply will continue to be there in 2018,” says Rajiv Shah, head of Middle East, Turkey and Africa capital markets at BNP Paribas in Bahrain.

“But we’re hoping for more corporates — both debut names and return issuers.”

Andy Cairns, group head of global corporate finance at First Abu Dhabi Bank, says that absolute volumes could be down this year, though, as so much sovereign issuance was done in 2017. By November, over $58bn had been printed, setting a new record for the region and easily usurping the previous year’s $42bn.

“Our expectation is for lower overall issuance this year,” he says. “Whereas corporate and financial institution numbers may be marginally up on 2017, this will be more than offset by a decline in activity from the big regional sovereigns.”

Unsinkable optimism

Saudi Arabia will be the key driver of volumes in 2018, having accounted for $22.7bn of deals in 2017 and $17.8bn in 2016.

November’s high profile arrests of 11 Saudi princes and dozens of senior officials and businessmen in Crown Prince Mohammed bin Salman’s attempt to crack down on corruption have given investors plenty to think about.

The Saudi government has tried to reassure investors that only personal accounts have been frozen and it is business as usual for companies. Moody’s has, however, pointed out that the “intermingling of individual and corporate activities ultimately could expose corporates to these individuals’ frozen accounts.”

Bankers are looking on the bright side, however. “That they’re cleaning up and making reforms in Saudi can be seen as a credit positive,” says Benny Zachariah, head of global loan syndications at Industrial and Commercial Bank of China in London. “Its Vision 2030 plan [a programme for investment and fiscal balancing in the country] is a big sign of Saudi’s ambition to grow and develop.”

The CFO of Saudi Electricity Co, Fahad Bin Hussein Al-Sudairi, agrees.

“In line with Vision 2030 international banks have a lot of focus and appetite for Saudi credit,” he says. The company signed a $1.75bn loan in August last year, which attracted 12 banks in total after the secondary syndication phase. “The appetite from the banks was tremendous,” he adds. “We had to trim the order book because of oversubscription.”

Growing chaos, growing interest

Despite the Qatari and Saudi flare-ups, bankers and investors are expecting increased interest from Asia in the region’s bond issues this year. “There’s been a decent amount of money sitting on the sidelines in this region,” says a portfolio manager in Dubai. “Liquidity has been low and any sell-off has been cushioned by investors thinking that any sell-off is a buying opportunity. And while the detail of the news has been interesting, the nature of the news is not shocking to investors already involved in this region. As a result, there has been very little rise in the risk premiums being demanded.”

Alex Karolev, head of emerging market syndicate at BNP Paribas in London, says the marketing strategy for bonds from the region — especially for Reg S-only deals — now typically includes some way of engaging with Asian investors.

“It wasn’t so common in the past, but now we’re advising clients to either add an Asian leg to their roadshows or to do an Asia-focused investor call,” he says. “As those investors continue to get bigger and diversify away from Asian transactions, this year we’ve seen more and more involvement from this investor base.”

He adds that this increased demand is across the board in the Middle East, not just confined to the strongest issuers.

This fresh appetite is one of the reasons the portfolio manager in Dubai says he is unconcerned by the political strife. His Middle East investment focus going into 2018 is largely on wider movements in the emerging markets, rather than political events within the region.

“There is an argument that could be made that we are being too complacent with regards to the situation within the Middle East,” he says. “But as the Middle East has drawn much more of a global following and a higher connectivity with the rest of the world has developed, the global market and the wider movements in the emerging markets will be much more of a driver of spreads.”

This dynamic of growing Asian involvement is being mimicked in the loan market, where volumes fell slightly last year. Chinese lenders are expected to become more prominent in Middle Eastern deals in 2018 as they seek higher returns than are available closer to home.

Deals such as United Telecom’s $600m loan in April 2017, which had 16 banks from China and Taiwan out of 25 on the deal, have shown the way.

Meanwile, Japanese banks are also still very much in the game. MUFG, Mizuho and Sumitomo Mitsubishi Banking Corp joined Saudi Electricity Co’s syndication in the primary phase and Bank of China joined in the secondary phase.

“We still continue to get sizeable support from Asian lenders,” says Al-Sudairi. “They have a good appetite for Middle Eastern credits.”

This rise in demand for Middle Eastern loans, coupled with a drop in dealflow, has led to pricing edging lower.

Abu Dhabi National Oil Co’s $6bn deal, signed in November, was priced below the average of what people thought possible, as it was seen as a relationship-defining transaction. The facility was priced close to 35bp over Libor for the three year tranche and 50bp over Libor for the five year.

“It’s become a borrower’s market,” says Zachariah. “If you don’t lend to a deal now, it’ll be a couple of years before you can do the deal.”

The Chinese government’s Belt and Road initiative is also tying the two regions more closely together. The initiative will see vast logistics and transport infrastructure networks built connecting Asia, Europe, the Middle East and Africa. There is a political push in China for banks — especially the state-owned ones such as ICBC and Bank of China — to finance some of the associated issuers in the Middle East.

“The Middle East is interesting for Chinese banks, as it is clearly important for the Belt and Road initiative,” says Zachariah. “As we start getting more involved in that space, you will start seeing our presence grow.”

Privatisation boom

The privatisation of government-related entities (GREs) in the region could also boost loan volumes. The private sector has traditionally been financed by local banks but privatised GREs are expected to be large enough that international banks will get in on the action. These companies could also push more investment and M&A, generating more loans and capital markets business.

“It’s a game changer if you have these big companies coming to the private sector,” says Jundi. “They will generate a lot of interest from the international financial sector.”

The Kingdom’s plan to privatise Saudi Aramco is drawing much attention, as has Adnoc’s IPO of its petrol stations, which was completed in December 2017. Oman Oil is also looking to sell some energy assets and list units on the local stock market.

This business will provide a welcome boost to the loan market. Last year up till November, there had been a 50%-60% drop in loan volumes compared with the same period the year before. Only $48.7bn had been raised across 80 deals.

Whether or not local banks will also benefit from the increased dealflow remains to be seen. The low oil price has eaten away at their deposits, so they have found it more difficult to compete in pricing. Some, such as Bahrain Islamic Bank, Rakbank and Warba Bank, came to the loan market for the first time last year to diversify their funding.

“There are only a handful of institutions in the Gulf [such as First Abu Dhabi Bank] that have comparable funding costs to those of international banks. That rules a lot of the other smaller players out of the market,” says the loan banker from a US bank.

But the lower oil price does mean that Gulf states have a renewed focus on diversifying their economies and increased investment in renewable energy projects for the first time.

“A lot of the Gulf international project finance transactions historically have been petrochemicals, pipelines and conventional power,” says Zvi Wohlgemuth, head of project, asset financing and CEEMEA loan syndicate

at Société Générale in London. “Whereas now we’re seeing a few renewables come to the market in the Middle East and we expect that to continue as sovereigns seek to diversify their power generation.” Abu Dhabi and Dubai both have solar development plans. Saudi Arabia is building a 300MW solar plant in Sakaka, which could require $250m of loans — the first of 60 greenfield projects the kingdom is planning over the next seven years.