Three investment bankers have come to visit a European company to pitch to lead manage its first bond issue.

The one who knows the client best is the relationship manager. She has been quizzed several times by internal committees at the bank about when the firm is going to make a return on the loan facilities it has extended to the client. Working with her on the pitch for several months has been the debt capital markets originator.

Their effort has paid off: they have secured an invitation to the beauty parade from which the final syndicate will be chosen, and taken their head of syndicate with them to try to seal the deal.

Winning the mandate would mean hitting the level of return the relationship manager has been promising the bank’s credit committee.

The client has been charmed by the syndicate banker’s air of confidence and engaged with the pitch book that was carefully prepared. As the book closes, the originator asks “Do you have any questions?”

“I just have one,” says the treasurer. “How many bookrunners would you recommend?”

The originator and head of syndicate glance nervously at each other, as they quickly try to evaluate what the right answer is for them and for the issuer, and whether the two answers are the same. And will they be in line with what the other banks are pitching?

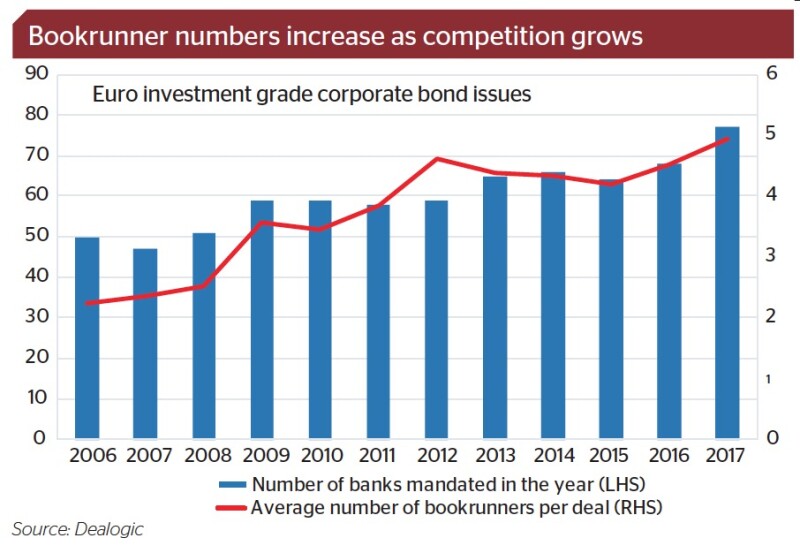

In 2006 the average number of bookrunners on a corporate bond issue was 2.25. By 2017 that had risen to nearly five.

This was originally driven by issuers. “The growth in the number of syndicate banks originally came about after the credit crisis,” says Marco Baldini, head of European bond syndicate at Barclays. “Changes in the market post-crisis drove corporates to adopt larger banking groups, as they sought to effectively diversify their risks.”

Suddenly, in 2008, companies found themselves in an unprecedented situation: they no longer felt able to rely on banks. Everything from loan facilities to derivatives counterparties was thrown into question. Spreading the love to more banks made sense.

Banks then began to welcome the move, as the cost of capital rose in the newly regulated world. They wanted to be paid for their capital, and for maintaining their commitments to the client through difficult times.

“After the credit crisis, interlinkages between loans and bonds grew much closer, as the focus on balance sheet return became a priority for banks,” says Baldini.

In 2006, a total of 50 banks were bookrunners on investment grade corporate bond new issues in euros. But in 2017 that had grown to 77, as more traditionally commercial banks added capital markets teams to their product suites.

This gives issuers a choice to make when selecting their syndicates.

On one hand they have investment banks, which have large, experienced capital markets teams, but lack big balance sheets to lend to companies. On the other are commercial banks, which have a much greater capacity to lend, and have added a DCM originator and syndicate person, but are not necessarily as knowledgeable or experienced as the investment banks they are now up against.

“It is about trying to find the right combination,” says Baldini. “One which has a good mix of smart advice, execution expertise and balance sheet commitment.”

For the company, is there a downside to having more banks working for you? It is not going to pay any more in fees for having more banks selling its deal. The same fee just gets split more ways, and hard luck to the banks.

But how many lead managers is optimal for the sake of the deal?

“This has all come about in the context of a market backdrop that has been one way in the last 10 years,” says Baldini. “However, there have been challenging windows within that period, and in those difficult markets you need the confidence of having an efficient syndicate group. If there is a difficult credit to sell, or complex messages to convey to investors, it can’t be as efficient with seven banks as with three. And there is less accountability with seven banks when things are not going well.”

The chasing pack

Baldini works for one of a handful of banks that are consistently close to the top of corporate bond league tables in Europe. Do others, outside that elite group, share his view?

“Issuers will always select one or two top five banks for confidence of execution,” says a syndicate manager at a Japanese bank in London. “If a transaction failed and the treasurer hadn’t appointed one of those top league table banks, he or she would likely face some serious questions internally. Those one or two banks give you the best idea of competing supply and market conditions in the run-up to a deal.”

But, he adds: “An issuer should definitely have a variety of syndicate banks. Sometimes I feel the larger banks are making recommendations based on the future pipeline and are not as aggressive as they might be to achieve the best deal here and now. We have a duty of care to an issuer to achieve the best outcome for its deal.”

His view on the optimal number of banks is higher than that of Baldini.

“On a regular issue I would say four banks is most efficient. It is the right amount to get good investor engagement and not too many banks to disrupt the process,” he says. “For larger and multi-tranche deals there is value in four to six banks to ensure all bases are covered.”

The average deal size has increased and in the last two years, particularly, the European market has hosted more multi-tranche deals. It seems natural to need more banks on such transactions. Doing one multi-tranche deal also means an issuer is likely to make less frequent visits to the market, which means fewer opportunities to repay its banking groups, which lend largely to get a bond mandate.

“If you were to analyse the returns banks get from financing corporates it would be a minimal return,” said the syndicate manager. “The only reason banks do the financing is for ancillary business, and they can then measure their overall [share of] wallet.”

Quality counts

“The wallet point is very important,” says Tom Bolton, head of corporate finance at Thames Water. He is responsible for the UK utility’s bond issuance. “There is always a high level view of how we’re rewarding the bank group overall. All the banks enter into those relationships by putting capital down and expecting ancillary business — primarily driven from DCM and swaps.”

Companies know very well they need to share out the goodies carefully among the banks in their group, to keep them sweet and make sure they stay loyal.

However, Bolton says it is not just a case of dividing up the business equally among the house banks. “Beyond the banking group element, there are two factors we consider, which is where banks can really differentiate themselves,” he says. “Firstly, we reward people for their platform. Are they investing in all the good things around salesforce, secondary trading, syndicate desk, etc. And then, just as importantly, the quality of the individual input — the focus we get, in terms of market intelligence and idea generation.”

Having gone through that process, Bolton agrees with the bankers’ view of an optimal syndicate. “Three or four bookrunners is optimal,” he says. “Beyond that you probably start to lose focus. The more people you have, the more difficult it becomes to co-ordinate calls and get a joined-up view.”

While the top 10 banks in the corporate bond league table have remained similar for the last decade, the next 20 positions have been reshuffled. Asian and Nordic banks have emerged into that area of the league table, at the expense of some core European banks.

“Without doubt, the top four or five European banks have the largest footprint with issuers and investors,” says a DCM banker at another Asian bank. “But beyond that, banks are trying to grow their businesses and become partners with their clients. Everyone is competing. The market is more competitive now than ever, and I’d like to think that means better and fairer.”