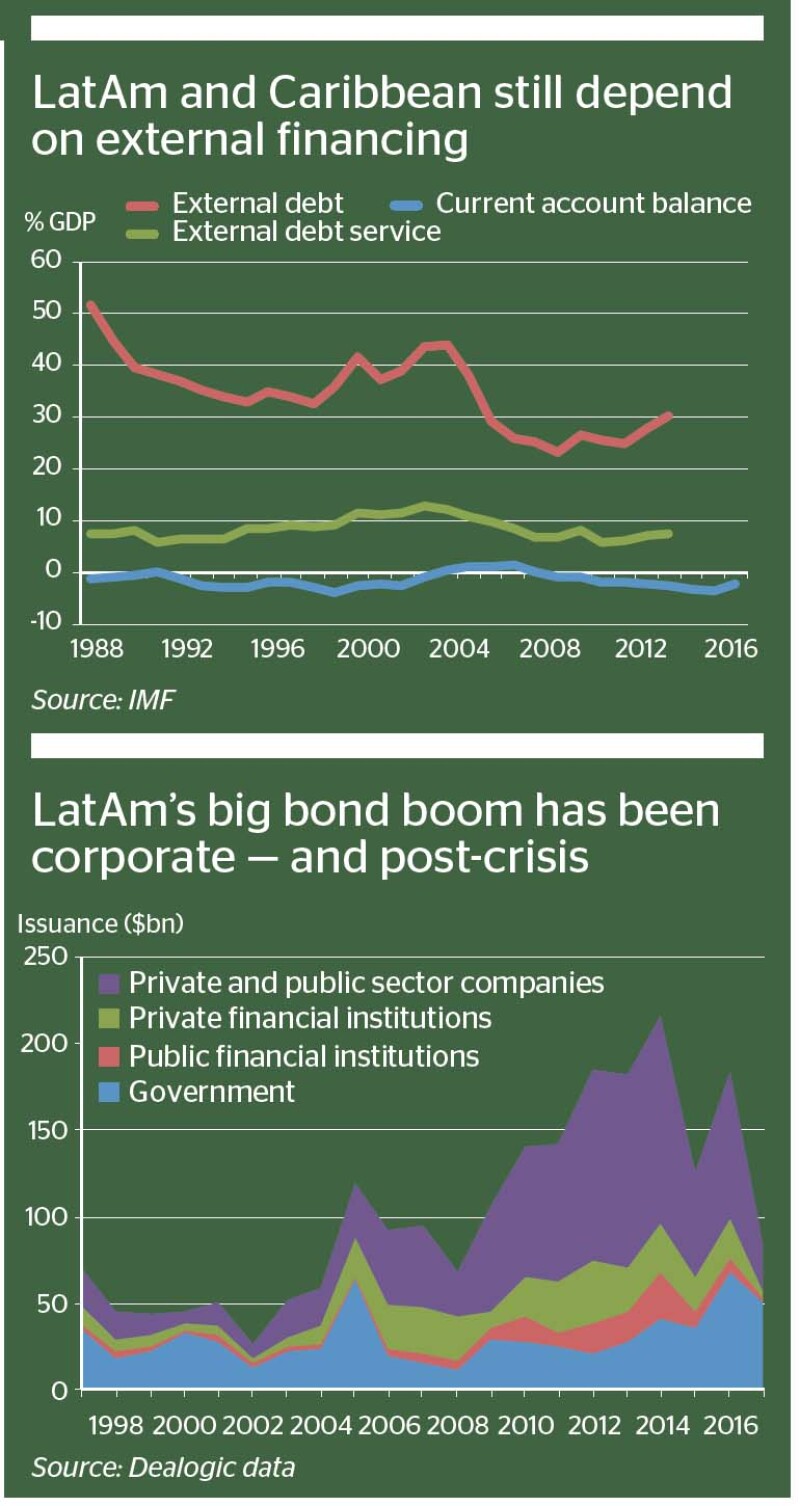

Argentina’s return to international markets in 2016 gave the clearest possible sign of the Latin American bond market’s potency. A country that kicked off the millennium with the largest sovereign default in history, revived with a $16.5bn bond issue in April 2016 — at the time the largest ever in emerging markets.

International markets lapped up $35bn of Argentine debt issuance in 2016, and this year has continued in the same vein as sovereigns, provinces, banks and corporates have all issued in a range of structures, currencies and maturities. All this suggests LatAm bonds are in great shape.

“The growth in the Latin American bond market has been astounding, with high levels of issuance even as fundamentals have not been as strong,” says Matthew Dukes, director in LatAm DCM at Deutsche Bank. “Investors have shown they are willing to sponsor compelling stories, such as Argentina, and the market has gained resilience.”

Max Volkov, head of LatAm DCM at Bank of America Merrill Lynch, highlights that the market comes back “bigger and stronger from each shut down”.

The question is, however, how much of this success is due to a better market, or is it just piggy-backing on an unprecedented era of low global rates.

Perhaps both arguments are right. Latin America — alongside all emerging markets — has benefited from monetary easing in developed countries. Yet temporary circumstances can lead to lasting change.

Dukes says that a key part of the market’s growth has been inflows into ETFs, which he calls a “double-edged sword”. When trouble hits, he says, the exit door for this “tourist” money is very narrow — leading to higher price volatility.

But this money has “helped to grow the capacity of the market, which overall has been positive”, he says. And there are plenty of positives that go beyond today’s exceptional global monetary conditions.

“Latin American issuers have generally become more astute,” he says. “Frequent borrowers are issuing larger deals, improving reference points for future deals, and using complex trades such as switches to more efficiently manage liabilities.”

Both Dukes and Volkov say further growth of the market will be a function of economic growth in the region. “New issue volumes of late have been high but significantly driven by refinancing; overall, there has been less money being raised for new investment,” says Dukes.

Volkov is “relatively confident that in 10 years we will have more issuers, a greater variety of corporates, and more local currency issuance”.

Picking on the small man

Nothing to worry about then? As with anything in Latin America, often the hidden narratives are more compelling.

“The LatAm bond market functions reasonably well at the issuance stage, in that governments and corporates issue at yields that reflect their creditworthiness,” says Graham Stock, head of EM sovereign research at BlueBay Asset Management in London. “However, away from the larger deals, the secondary market can be very illiquid — meaning that only a few bonds trade frequently and many more might take a while to price properly.”

Bonds in Latin America are subject to the tyranny of the indices: those big enough to be in the JP Morgan indices enjoy far better liquidity than outsiders.

Herein lies a cruel irony. The LatAm bond market’s growth has made record-breaking deals possible and unprecedented levels of cash available to finance borrowers, but it has restricted access to the region’s smaller companies.

“The market is not as strong as it used to be for smaller borrowers,” says Dukes at Deutsche. “In certain situations in recent years, investors were trapped in credits and couldn’t get out of them. Index eligibility size has become very important to improve liquidity.”

A minimum size of $300m is ideal. As Volkov points out, a new issue of $300m or more will attract an average of 130-150 investors. “In smaller deals there’ll be half the number of accounts, generally placing smaller orders,” he says.

This is not just a function of the indices; it is also collateral damage from the rise in assets under management at the largest EM bond managers.

“In the early 2000s we’d easily be able to get away a $125m deal and attract names that today are the real big name investors,” says Volkov. “By now, though, these funds’ assets have become huge — they’ve quadrupled in some cases. This means they have to focus on the larger, more liquid names, and smaller companies may not be on their radar screen.”

Closer to home

Where does this leave smaller companies? Perhaps there is a clue in a reason that Dukes gives for lack of smaller deals in recent years. He says another problem for smaller issuers is that many do not have significant dollar revenues, and were thus hit by the correction in EM FX markets that began in 2013.

These issuers did not necessarily need dollars, but needed the size and tenors that the dollar market could offer them.

In an ideal world, these companies would have financed themselves locally. But, as Stock at BlueBay says: “The market that needs most development is the local currency corporate bond market.”

Given low liquidity, lack of infrastructure, and the combination of currency and credit risk, this is easier said than done. But there are reasons for hope.

Few people know the challenges like Carlos García Moreno, CFO at América Móvil since 2001 and previously Mexico’s director of public credit.

Latin American countries have made important developments in expanding sovereign local currency markets, he says, highlighting Mexico’s progress over the last 20 years as the “most remarkable”.

“The pension funds were established in 1997, the government then developed a full yield curve, and international investors were attracted to the market,” says García Moreno.

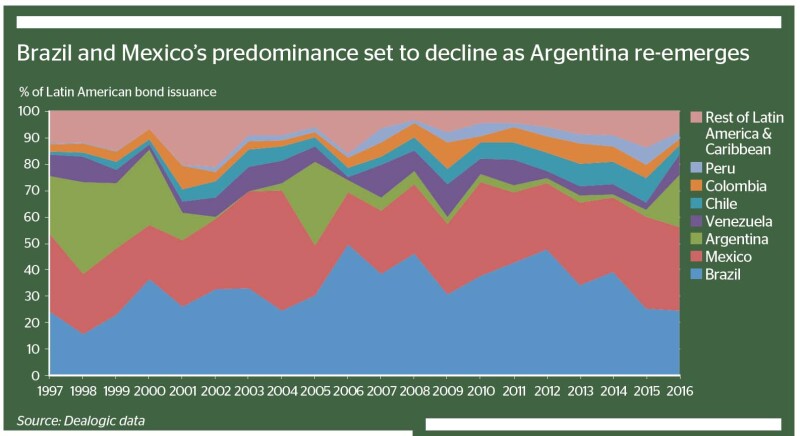

Indeed, according to an IMF and World Bank staff note in December 2016, four Latin Americans make the top 10 EM countries by foreign participation in local sovereign bond markets: Peru, Mexico, Brazil and Colombia — way ahead of larger markets such as China and India.

In the region’s best countries, therefore, the “original sin” of overloading on dollar debt is a thing of the past.

Volkov acknowledges the “remarkable progress” of Mexico, and that other LatAm jurisdictions are working to make their local markets Euroclearable. He says this will ease access to local markets.

Corporate local currency bonds have “not spread into the main EM universe”, says Volkov. But the progress in the sovereign universe is promising.

“Corporate markets tend to follow sovereign markets, so as larger institutional investors come in and liquidity improves, that market should grow,” he says.

García Moreno agrees that facilitating corporate issuance in local markets is the next stage. “There is much to be done to improve the functioning of the market: better oversight of market players; sufficient liquidity; more information on the market,” he says. “But I’d like to think that in the next 10 years we will see meaningful progress.”

As in sovereign markets, Mexico again leads the way. América Móvil has done some innovating of its own, and since 2012 has sold peso-denominated títulos de crédito extranjeros. These instruments, registered bonds with the SEC in the US and Mexican regulator, CNBV, allow the firm to sell the notes to both domestic and international investors.

“By bringing together the local and international investor base, we think we’ve found a very efficient format for peso issuance,” says García Moreno.

Not many companies have the clout of América Móvil, however, and the CFO says the ministry of finance must play the “central role” in the development of local markets, helped by entities such as pension funds and insurance companies.