Volatility in global bond markets this year has pushed many Asian borrowers to the local markets for their financing needs. The region’s domestic debt markets have certainly held their own and proved resilient — but their success has also shown their limitations.

Asia ex-Japan G3 bond volume in the first half of 2022 fell 35% year-on-year, as market turbulence shut a key source of liquidity for many borrowers. But the local markets came to their rescue, witnessing a 30% surge in volumes during the same period, reinforcing the stability and necessity of domestic funding avenues.

It is no surprise that the second largest bond market in the world played a big role in lifting Asia’s domestic bond volumes. China’s onshore renminbi debt market has grown this year, as has the offshore renminbi, or dim sum, market. Dim sum volumes jumped 160% in the first half of the year compared to the same time in 2021, and the Hong Kong dollar market got a 35% boost.

The regional markets of Malaysia, Indonesia, India, Singapore, Thailand and Vietnam also saw higher bond supply and demand as rate volatility and geopolitical tensions rocked the dollar market.

This has proven, yet again, that Asia’s local currency bond markets are a reliable source of funding, especially when borrowers don’t have a natural currency hedge and global market issuance freezes. But the depth of liquidity in some of the markets leaves much to be desired.

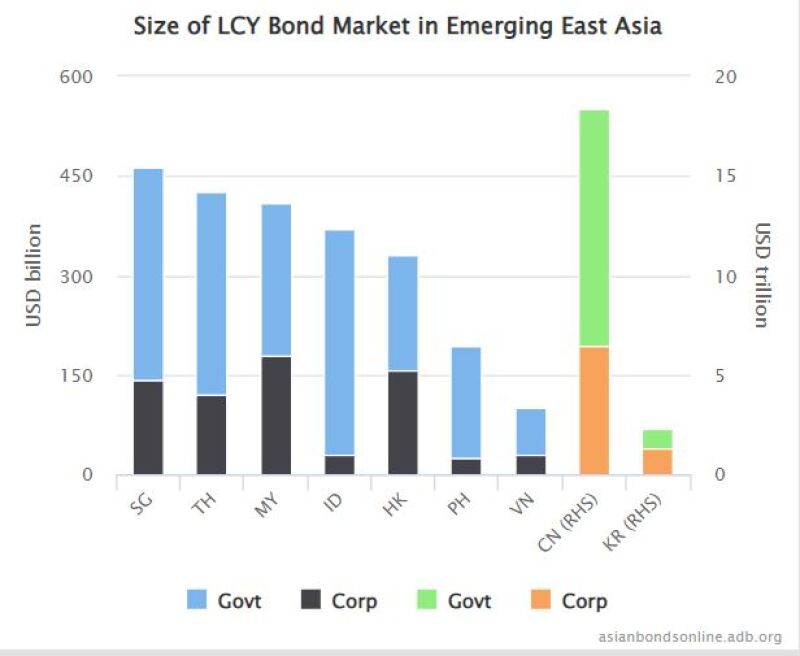

Government vs corporate bonds

It is well established that local bonds are a great alternative to bank finance. So to de-risk the banking system, it is critical to have a parallel, robust, corporate bond market. Deeper bond markets can offer longer term capital, meaningfully reducing the asset-liability mismatch in the financial system.

The bond market also taps into a wider investor base when compared to the bank market, ranging from asset managers and insurance companies to retail investors and other funds. This means it’s only natural that the debt markets should be among the first ports of calls for borrowers. Yet, the local markets in only a small group of Asian economies have proved their resilience and sophistication.

China is a good example to emulate regionally. It has one of the largest local corporate bond markets, as well as offshore market.

By the end of June, the country’s onshore corporate bond market stood at nearly $6tn of the total $18tn local market, data from the Asian Development Bank shows.

Except for South Korea, Hong Kong, Malaysia and Singapore, most regional onshore corporate bond markets remain shallow, and largely restricted to higher rated companies.

Also, government bonds continue to dominate. For instance, by the second quarter of 2022, total outstanding local sovereign bonds from emerging east Asia stood at $14.5tn — comprising 63.1% of total outstanding bonds from the region.

In the second quarter, governments from emerging east Asia issued $1.6tn of notes, up about 26% from the previous quarter. In contrast, private sector bond flow fell 4.9% to $812.6bn as companies put off borrowing amid rising costs and a weak economic outlook, shows the ADB’s latest edition of its Asia bond monitor.

In India, a key market being eyed by foreign investors for its inclusion in global indices, growth in the corporate bond market has been disappointing.

By June-end, roughly Rp39.58tn ($480.6bn) of corporate bonds were outstanding from 29,745 instruments, equal to an average size of Rp1.33bn, reflecting illiquidity in the secondary market, one of the deputy governors of the Reserve Bank of India said in a public speech in August. In contrast, some $1tn-equivalent from 100 government securities were outstanding.

If India can boast a deep government bond market, surely it should replicate that success in the corporate market?

India has made some efforts, ranging from introducing electronic bidding for primary deals to opening up to foreign investors. But it still hasn’t overcome some big challenges: borrowers’ preference for private placements, regulatory bias towards higher rated bonds and low retail participation.

Its move to push for the development of an offshore rupee bond market, also known as Masala bonds, has also failed to make a big-bang impact, with no issuance in the past couple of years.

With Masala bonds, the currency risk lies with investors rather than the borrowers. But at a time when the rupee has been under pressure, the market hasn’t been appealing to investors. Before that, the imposition of withholding tax and other regulatory quirks around use of proceeds and tenor restrictions hobbled the market’s growth.

Indonesia’s global rupiah bonds, or Komodo bonds, have also not found much success.

Dim sum surge

In comparison, the renminbi market has flourished. In the first half of 2022, dim sum volumes totaled about Rmb109.5bn ($16bn), versus Rmb91bn for the whole of 2021.

Chinese and Hong-Kong based borrowers have not shied away from consistently tapping these local currencies. On Tuesday, for instance, Hong Kong Mortgage Corp raised HK$8bn from a two year social bond and Rmb3bn from a three year social dim sum.

The resurgence of the dim sum market is laudable considering it had remained subdued for many years. The opening of the southbound channel of China’s bond connect programme —allowing mainland investors to access CNH and HKD bonds — was a catalyst.

Naturally, investors and issuers will flock to markets that will give them an edge, be it on size, price or maturity. The dim sum market has proved this, as has the Singapore dollar-denominated bond market which this year offered a decent arbitrage opportunity, attracting several European lenders to issue capital bonds.

The pool of private bank investors in the Lion City has become a driving force behind these deals. Singapore has been proactive in welcoming billionaires to open family offices in the city, attracting private wealth. GlobalCapital Asia was first to report in August that Indian billionaire and head of Reliance Industries Mukesh Dhirubhai Ambani had set up a single family office in Singapore.

The importance of Asia’s local currency debt markets is only likely to grow given rising dollar interest rates, global market volatility and international investors remaining in risk-off mode. Countries with vibrant onshore markets will reap the benefits.

But governments should be proactive in ensuring their markets remain self-sustaining — including by setting benchmarks in both short and long tenors for the corporate sector to leverage.

There will be foreign exchange risks to overcome, but by bolstering the local markets now, regulators can ensure some funding tools remain open for firms if global choppiness persists. That can only be a good thing.