Securitization and technological innovation are in many ways natural bedfellows. Ever since 1971, when Freddie Mac issued the first conventional loan securitization, the market has constantly looked for new areas of exploration in which securitization could serve a purpose. Indeed, as one banker told GlobalCapital, the industry has always been at the “nerdier” end of the capital markets.

Away from mortgages, the market now has a range of thriving asset classes — from office buildings and auto loans, to credit cards and equipment leasing. But the continued development of the securitization industry, particularly since the global financial crisis in 2008, has only been possible thanks to the broader evolution of technology.

What’s more, the securitization market’s ability to regain trust since the crisis is closely tied to technological advances, a banker in New York told GlobalCapital.

He says that, looking back at the global financial crisis and comparing it to the present day, having greater transparency on the underlying collateral and its performance characteristics has helped move the market forward. Previously, the lack of data perhaps contributed to a “sense of a lack of liquidity in our market” and made it look “opaque”.

The proliferation of data that has enabled greater transparency in securitization has tended to come from the originators as they’ve improved the information they hold on consumers to make better credit decisions. Nigel Batley, an independent consultant and representative at structured credit manager Lord Capital, believes this has played a large role in making securitizations easier.

“You’re getting better performing credit,” he said. “Because machines are fundamentally very clever, much quicker and they give you better, more consistent outcomes in terms of your credit assessment of a portfolio.”

The New York-based banker said that some of the improvements from loan originators came from issuers producing vast amounts of data to build investor confidence in their products. This then quickly snowballed to become “a standard that didn’t exist before”.

“I remember there being a big question about how was an investor ever going to actually use all this data,” he said. “Of course, technology has allowed investors to process what was an unthinkable amount of information just five or six years ago.”

Crucially, the ability to process data has made market participants across the securitization ecosystem more comfortable with what they’re lending to or investing in.

Fintech and non-bank lenders have also contributed to pushing consumer lending technology, and have dragged the bigger players along with them too.

A lawyer tells GlobalCapital that one bank found, as it was trying to expand its corporate lending, that its own loan approval processes took at least four weeks. Meanwhile, the “fintech guys” were doing the same processes in two days, so the bank decided to either buy the fintech firm or partner up with them.

“Banks aren't standing still on this,” the lawyer says. “They are investing very heavily in the fintech companies themselves and all their technology, or in developing their own rival technologies to try and keep pace.”

The lawyer adds that things will get “interesting” as the fintechs and non-bank challengers evolve and get to a critical mass in the coming years, which could see some firms breaking out of their “challenger firm“ label — or get folded into banks.

“They’re quite conservative,” he says. “They don’t have huge losses on their books and they’re not trying to lend in an aggressive way.

“Then the question becomes: how do they expand? Either the technology is good enough to give them the expansion route, or they have to look at the way in which they’re lending and go down the credit spectrum.”

Accidents waiting to happen

Fintechs have been able to drive forward the technology behind consumer credit decisions, and they have been — as Batley says — “encouraged” by regulators such as the Financial Conduct Authority (FCA) to do so. In turn, this has meant the data given to investors of securitized products is much improved.

But super-speedy credit decisions have also brought problems.

Buy-now-pay-later (BNPL) securitizations had been tipped to become an area of the market that was ripe for expansion, but with numerous lenders in the sector coming under stress, those hopes have been dimmed.

San Francisco-based lender Affirm Holdings’ share price collapsed from $176 in late 2021 to around $20 by May 2022 as fears grew over the sustainability of such business models in a rising rates environment. Meanwhile, Swedish BNPL company Klarna reported losses that quadrupled in the first half of 2022, to $581m.

One investor told GlobalCapital that the lack of regulation surrounding these sorts of companies likely led to them holding bad debts.

“I suspect they make very quick credit decisions,” he said. “As a result of being regulated, they’ll have to be much more responsible about what they do going forward [and] I think that’s a positive move because I think lending people money that they could never afford is not actually good for anybody.”

Speaking more generally, another UK investor says he was concerned that the technology creating quicker approvals was “an accident waiting to happen”.

“I do worry about some of these guys that say they will give you a mortgage decision within X number of seconds or X number of minutes,” he says.

He adds that greater automation on house valuations before the global financial crisis had contributed to the massive losses that were made in the US subprime market.

“We always need some regulatory help,” he says.

Blockchain: a new frontier

Away from loan origination evolution, finding a successful use for blockchain technology in the capital markets is a task that has proved elusive, and securitization is no different.

However, there is hope that securitization and blockchain can work well together and that securitization perhaps stands to gain the most of any sector thanks to its inherent complexity.

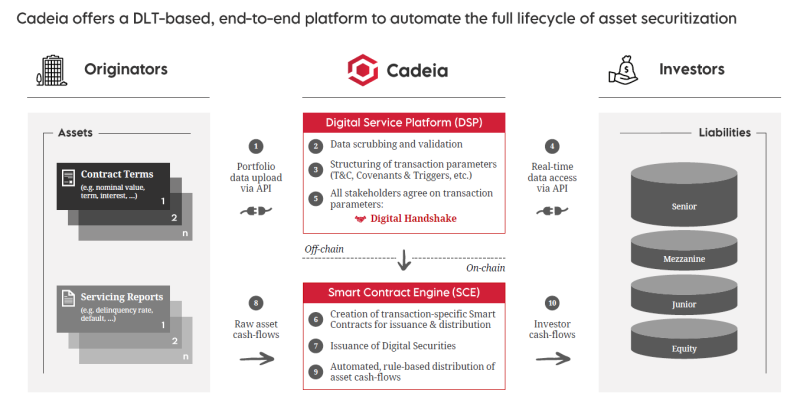

Cadeia is a German fintech start-up seeking to “revolutionize” the securitization market through digital end-to-end processing and data-transfer, using blockchain technologies like distributed ledger technology (DLT) and smart contracts.

Rolf Steffens, co-founder of Cadeia and a former managing director in structuring at Deutsche Bank, Merrill Lynch, and HSBC says the current system is opaque, slow and inefficient.

“Once you’ve executed, if a single covenant is breached all transaction participants start turning pages in the info memo trying to figure out what the people who closed the transaction many years ago have agreed,” he says.

It can take weeks or even months for performance reports to be recreated, communicated to investors, trustees and other parties to see who is owed what, Steffens says.

“Then it arrives at each individual investors' desks, [and they] then try and understand whether the report makes sense.

“It’s completely contrary to what digitalization can and should provide today."

Cadeia, through its use of DLT and smart contracts on their platform-as-a-service, has already created “rule-driven cashflow distribution” that makes the allocation of funds post-transaction agreement completely digital and automated over the entire transaction life cycle — from structuring to issuance and post-issuance servicing, including a full audit trail.

While Cadeia has executed a transaction, DLT and smart contracts are a long way from being commonplace.

“We are many, many years away from that,” says the lawyer.

“It has to happen a bit more in the mainstream debt markets first… In the structured finance space, we’re going to sit at the back of the queue,” despite securitization being particularly “intensive”.

Batley also has concerns over the environmental impact of using blockchain technology.

“It is power hungry and therefore it’s not very environmentally friendly,” he says. “Blockchain does burn an awful lot of electricity every time you have a movement and update every computer in the system.”

It also brings a broader question for the future of fully automated contracts and transaction executions: who is responsible if something goes wrong?

“The reason why you trust companies is because you have a human being actually checking the process, and that company has a liability, a responsibility to make sure certain things happen in a certain way,” says Batley.

He adds that establishing liability is going to be yet another hurdle to making blockchain technologies a constant feature of the securitization and the capital markets.

Clearly, there is a long way to go, and as one banker told GlobalCapital, market participants need to be taken on a blockchain journey that goes beyond their initial curiosity and proves that the technology works — before the real challenge of completing transactions with all the various stakeholders can begin.