Ireland

-

The subject of SME-backed covered bonds continues to provoke a sharp division of opinion within the industry. And it was a lively topic at the annual covered bond investor conference, held on Thursday in Frankfurt.

-

Sparkasse KölnBonn is set to announce a deal in the belly of the curve, somewhere in the region of five years, bankers told The Cover on Monday. Other issuers, possibly from Europe’s periphery, are also considering deals, said bankers, after further strong performance in the secondary market.

-

Since UniCredit’s groundbreaking covered bond deal last year, a plethora of issuers have priced inside their sovereign. This new financial order has led to a re-examination of how covered bonds are priced and whether sovereign risk has much bearing on covered spreads anymore.

-

Core and peripheral borrowers are waiting for a better market before bringing benchmark covered bonds. Safe-haven names are traditionally first to take advantage of returning stability. But southern European borrowers, which offer higher yields, juicers spreads and are less flexible over pricing, will find execution easier, said bankers.

-

Bank of Ireland priced a hugely successful €500m five year transaction on Friday, bringing its longest benchmark covered bond in over three years and radically repricing its curve relative to the Irish sovereign.

-

The Irish sovereign’s successful 10 year benchmark has paved the way for the country’s covered bond issuers to push out their curves and take advantage of investors’ thirst for yield, said syndicate bankers on Thursday.

-

Issuers looking for rehabilitation in the capital markets and wanting to wean themselves off central bank funding must be careful to ensure they issue strategic deals that have a high chance of performing. This should lower their long term cost of funding and enable greater market access.

-

Allied Irish Bank (AIB) has priced its first covered bond since the crisis. Vocal investors, who had demanded a wider spread were compelled to cave in to blistering demand and, rather than cut their orders, they were forced to inflate them.

-

Bank of Ireland has priced its first covered bond in three years, attracting a heavily oversubscribed book that was broad and granular. The deal, that many may have considered impossible only a few weeks ago, pays further testimony to the continued bid for higher yielding assets and represents a strong endorsement of covered bonds.

Bank of Ireland has priced its first covered bond in three years, attracting a heavily oversubscribed book that was broad and granular. The deal, that many may have considered impossible only a few weeks ago, pays further testimony to the continued bid for higher yielding assets and represents a strong endorsement of covered bonds. -

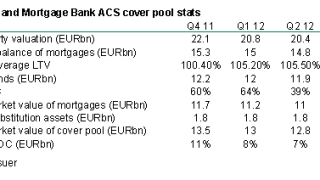

Bank of Ireland Mortgage Bank looks set to reopen the Irish covered bond market and has appointed joint leads for the first Asset Covered Security since the crisis. With Irish government bonds trading inside Spain’s and Italy’s, the deal should get more competitive funding.

-

Irish Finance Minister Michael Noonan has rejected a private members’ bill to adopt the Danish balance principle for covered bonds but he will investigate whether some elements of the bill could be rolled out.

-

SSA and corporate markets were busy on Tuesday, keeping the primary covered bond quiet. But issuance should improve this week as investors filter back from holiday, said bankers, though they warned that as spreads have tightened a long way in a short time the market may widen after the initial flurry of deals.