Just like every other citizen in Ukraine, those responsible for managing and financing the country’s economy had their lives turned upside down on February 24.

But ever since that fateful Thursday when Russia invaded, Ukraine’s finance ministry has been on the front foot, determined to win the economic war by waging a campaign of constant communication with the outside world — other finance ministries, investment banks, multilateral development banks, institutional investors and the financial press.

Keeping Ukraine’s economy and financial needs at the top of the news agenda has been a central plank of the country’s strategy of building support from allies all over the world, including the European Union, the US, Canada and the UK — support that has helped Ukraine not only resist Russia’s advance but knock it back in some parts of the country.

The financial battle has often been fought remotely — on television, in publications such as GlobalCapital, and via effective campaigns on social media, especially LinkedIn, where Ukraine has given regular updates of its military bond auctions and news about budgets and deficits.

On the road

In this sense, it has been a very modern financial war, despite regular power cuts making communications difficult.

But it has also been done the old fashioned way — in person. Officials, notably finance minister Serhiy Marchenko and head of debt management Yuriy Butsa, have spent much of the year on road trips to shore up diplomatic and financial support, lobby for debt moratoria and push for more cash, at times through innovative structures and diverse sources.

Often the journeys would involve driving from Kyiv to Poland, then flying to capital cities and financial centres across Europe and North America to attend conferences, including the IMF and World Bank annual meetings, and private talks with politicians, bankers and investors.

The journey from Kyiv to London, for example, typically takes the team 24 hours and involves driving along Ukraine’s hazardous roads, subject to missile attacks at any time.

Often accompanying the finance team this year have been investment bankers including Borys Matiash, a member of BNP Paribas’s emerging markets debt capital markets team in London who is also Ukrainian. He has seen how quickly and drastically conditions have changed for the country. Before February 24, Ukraine’s economy had been performing well.

Its economy had recovered well after the pandemic, growing by 3.4% in 2021, the budget deficit was falling towards a target of 3% of GDP and the national debt had shrunk from 67% of output in 2015 to 43% in 2021.

“The country had gone from strength to strength in building up a very functional and diverse financing toolkit across international and local debt markets, supplemented by concessional financing channels,” Matiash says.

Since the invasion, government revenue has fallen by 30% and expenditure has spiralled, both military and social.

“The government has had to focus its sights on the financial battlefield, to expand and diversify its funding toolkit, to ensure that the required financing was channelled to support the economy and social needs,” Matiash says.

In his view, Ukraine’s strong track record has helped it mobilise finance from international sources and gather support from investors for a debt moratorium.

“The goodwill and the image that Ukraine — as the economy and as the borrower — has managed to build within the last several years is outstanding,” Matiash says.

After the invasion, he says, “it took only a few days for the Ministry of Finance to get all its creditors on the global investor call on the following Monday, to give the entire bond market community a live update on the state of affairs, with reassurance, courage and unbreakable spirit.”

The following day, the first auction of military bonds took place. Matiash believes this is another example of how fleet-footed the ministry was in the early days of the war.

That proactivity “has exponentially grown ever since, in terms of diversification and expansion of financing channels through public and private sector, within and outside Ukraine’s borders,” Matiash says. “Despite unprecedented work and life conditions, the Ministry of Finance team has continued its proactive investor engagement, with uninterrupted communication channels and high frequency of investor updates... on both sides of the Atlantic.”

The following interview with Serhiy Marchenko and Yuriy Butsa took place in early November in London.

GlobalCapital: As the winter gets colder and the pressure on energy prices rises even further — along with high levels of general inflation — are you concerned that the international community will force you to sue for peace?

Serhiy Marchenko: In the middle of summer we had some concern that the level of support for Ukraine was beginning to fall. But in the beginning of autumn, when we successfully liberated part of our territory — first in the east, and then in the south — I saw that in the West, and specifically in the EU countries, they realised that supporting Ukraine is worthy.

It’s not just a charity act — it’s an act of self-preservation. They are protecting their countries through supporting Ukraine.

You know, if you compare the cost of our war — including all the international support that has been provided and pledged to us, such as the grants from the US and from the EU via its Macro Financial Assistance Programme, as well as other donors — with the cost of war for all countries in the world, then it is in fact a small amount of money.

I don’t overestimate this fact. We realise that there are cost pressures everywhere — oil and gas prices, general energy prices, food price inflation and the threat of recession — but this is the natural cost of war.

We urge countries all around the world to spend as much as they can to help us defeat Russia. If we do not defeat Russia, then the costs will be so much higher for the world. That’s why I think it’s natural to support Ukraine — it’s less costly in comparison with the effects of war for all nations. So I urge the international community to continue with its financial support — as well as help us get enough military support.

GlobalCapital: So what does the retaking of the city of Kherson represent? Do you see it as a major breakthrough in the campaign to force Russia out of Ukraine?

Marchenko: It’s a part of the process. It doesn’t represent a particular milestone to us — it is just part of our campaign to retake temporarily occupied territories back in the fastest possible way. It’s not the middle or the end and it’s not the start. It’s a process. Now we move on to take the rest of the Kherson region, as well as the other regions such as Donetsk and Luhansk.

GlobalCapital: You mentioned how the international support for Ukraine was energised by some of the rapid victories you have achieved. But does this not show that to keep the international community energised and committed to supporting Ukraine, you now need to keep on retaking ground?

Marchenko: Of course we should continue to show progress on the battlefield. This is without doubt. But it shouldn’t be at any cost, because the real cost of bringing back our lands is the lives of our soldiers and people. We don’t want to sacrifice these very precious lives by being too hasty in our efforts to recover our lands.

We need to be wise. We have shown that we can use very modern weapons that other countries have provided us with to destroy Russian military assets, including their logistics operations. That makes them weaker, without having to engage in close combat, which of course endangers a lot of Ukrainian lives.

I think we showed this with Kherson — the Russians, who had been weakened by our efforts, decided it was better to withdraw rather than engaging in close combat.

GlobalCapital: So what you are saying is that you want victory but it cannot be at any cost. So, when is an appropriate time to enter peace talks? Is it only after Russia leaves all of Ukraine’s territory or before?

Marchenko: Let me be clear: it’s when Russia leaves all of our territories, as they were in 1991. Only then can we negotiate with Russia.

But it won’t just be negotiation around peace or disputed territories. It will also be discussions around the cost of reconstruction and cost of damages — reparations. If they destroy parts of our lands, they should pay for them.

GlobalCapital: Increasingly, the international community is talking about a 21st century Marshall Plan to rebuild Ukraine. Is that a term you are using as well?

Marchenko: It’s a very familiar and very successful name and we are OK with it. But to be clear, we are talking about the Marshall Plan for West Germany, because there were several not so successful examples of Marshall Plans, I understand. So, yes, a Western Germany Marshall Plan is the best example for Ukraine.

GlobalCapital: What should this Ukraine Marshall Plan look like? How should it work?

Marchenko: For us it’s important to find a way how to better attract private investment. It shouldn’t just be made up of concessional financing or international financial institution support.

If you really understand the cost of our damages, the cost of reconstruction will be hundreds of billions of dollars and that will not be possible without private investment. So we are interested in creating the right kind of environment to attract this investment and to structure it in the best way.

GlobalCapital: Would one way be to create a dedicated supranational bank, let’s say a Ukrainian Bank for Reconstruction and Development — a bit like the EBRD or the World Bank — that is owned by the international community so that it can borrow cheaply and crowd in private sector investment? Is that a sensible approach?

Marchenko: I don’t think so. Maybe it could be one part of the solution. But again, the question is around creating sufficient conditions within Ukraine to be able to attract billions of dollars of private sector investment. It shouldn’t be one very easy solution, it should be about creating the right environment in Ukraine so that businesses see it as natural to invest.

GlobalCapital: I mentioned the supranational approach because private sector money wants return on risk and risk needs to be managed. So how would you balance that?

Marchenko: It is perhaps more fundamental than that. Security is absolutely crucial and a precondition of external investment. For example, it means that we should have a very strong air defence system, so that we can protect ourselves.

The first and most important thing could be the EU accession. Because being part of the EU society means having the necessary commitments around security and defence — this is a natural way of life for Europeans. Of course, legislative changes are needed and it could take some time for us to implement such structural reforms.

GlobalCapital: EU accession is crucial of course, but as Olaf Scholz, Germany’s chancellor, recently said, reconstruction will be an enormous task that Ukraine cannot manage alone or that the European Union cannot manage alone. You are going to have pull in global investment.

Yuriy Butsa: In my view, it’s not about creating one structure that miraculously can rebuild the country and has all the knowledge and capacity of the world in one place.

It’s more about a very bottom-up approach. For example, businesses know much better what they want and need than any government or multilateral institution. The EU free markets give them many more opportunities than government financing, so we just need to create the right environment for them.

In this context, access to the EU market is crucial, especially given the current environment where businesses want to build supply chains in other countries that have similar values. We can represent the perfect case for such investments by being geographically close and economically integrated with the EU.

It’s the same with physical infrastructure rebuilding. Nobody at the government level in the country knows better than the mayor of a town what is damaged there and what are the most pressing needs, whether the priority is a school or ambulances, for example. It is important to leave the decision-making in the place where it’s actually the most efficient — centralisation is not always the right answer, it’s more about an efficient level of co-ordination.

GlobalCapital: How are you dealing with the issue of deciding what to start rebuilding when the Russians can just destroy it again?

Marchenko: They can’t destroy everything because they don’t have the capacity to destroy everything. But we have no other choice but to repair what they destroy. They destroy, we will repair and so on and so on.

Our president has said we will have to live without Russian gas, without electricity, without water supply — but without any relationship with Russia as well. There is no doubt that it is going to be difficult and Russia will find ways to make us suffer — for example, with its air strikes targeted at our power infrastructure. But we will survive.

Butsa: As a personal story, I have that Keep Calm and Carry On poster in my office — it was a present given to me before the war started. But on the day the war started I took a selfie with it and sent it to everyone who was asking me if I was OK. So, the poster found its true purpose and that’s how we manage things — by keeping calm and carrying on.

GlobalCapital: You have introduced a moratorium on your bonds. How was that received?

Butsa: Well, it’s not a moratorium; we got consent from our investors to postpone repayments for two years. It’s not quite the same thing.

GlobalCapital: Does that moratorium include the MDBs?

Butsa: It doesn’t include MDBs because of their status as preferential creditors, but it does include all the official bilateral debts and Eurobonds.

GlobalCapital: But looking at the numbers of your existing debt, the moratorium and the amount you will need in the future, don’t you think that actually what you really need is a debt jubilee?

Butsa: Look, it’s a question of what you want to see in the future, right? We used to be a self-sustainable country. We got financing from the international markets and we had transparent and credible relationships with investors. And we want and will need to rely on market financing in the future.

So any hostile or market-unfriendly steps with our debt actually go against this logic. We view the private sector as a key supporter, not only of our sovereign financing, but also our private sector and its borrowers. So the country in general needs to have good relations and access to the market.

Because of this, we will not look at solutions that go against our desire to be present in the market as soon as it is practically possible.

GlobalCapital: But you must think a debt restructuring at some stage is inevitable?

Butsa: We don’t know. To answer this question you need to have at least some sort of view on the macroeconomic framework for some prolonged period of time. We quite recently did some work on extension of our planning horizon from three months to a year, which was itself subject to multiple assumptions.

So, how can we credibly come and say, ‘OK guys, that’s the framework for five years’ if nobody can model the framework for five years for Ukraine?

One important thing to note is that it took us two years to return to the international markets after the first active phase of war with Russia in 2014. So if in the positive scenario we regain market access within the same timeframe, we have the experience of how to proactively manage our debt in a market-friendly manner. So that’s how we think about it.

GlobalCapital: Are you happy with the financial support you have received from the international community so far?

Butsa: Are we happy with the commitment? Yes. But we cannot be 100% happy with the way disbursement has been happening this year — not fast enough and not predictable enough. The predictability is really important.

But our partners, including our biggest ones in terms of size of support, such as the US and EU, have recognised the seriousness of the problem and have redesigned their solutions in such a way that will give us visibility for the whole of next year. We have seen the EU announcing an €18bn financial support package for us for the next year and the US proposal to continue budget support for the first three quarters of next year. It’s great that we have been heard and that the redesign is happening.

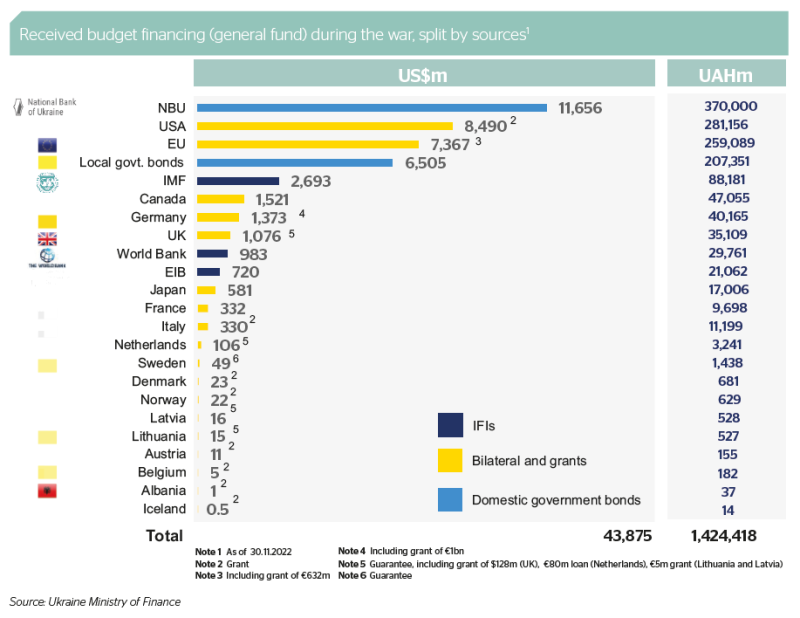

Marchenko: And, you know, because of the unpredictability, which meant we did not have stable financing for this year, we found it necessary to use monetary financing as a tool to cover our budget deficit. This year we have already issued about $11bn of government bonds bought by the National Bank of Ukraine.

This is something we are not happy about, because it means that we are in danger of creating an inflationary spiral which could harm our economy. That’s why it’s so important to have predictable money supply, because otherwise we will be just another state with huge damages to macroeconomic stability, which can be avoided with simple solutions.

So, it’s much more efficient to commit $3bn per month to support Ukraine than to look for the ways to solve multiple economic problems in the future, as happens now in some other countries.

GlobalCapital: In your budget you have basically achieved fiscal consolidation by reducing the monthly deficit from $5bn to $3bn. How have you managed that in the middle of a war?

Marchenko: First, and most importantly, we have decreased our expenditures by reducing all unnecessary spending over several stages. At first, the budget deficit was almost $7bn but we have cut our costs effectively.

Meanwhile, our capacity to collect taxes has returned. For example, at the beginning of the war, customs was collecting only about 30% of pre-war taxes — now it is collecting up to 80% of the pre-war tax amount.

However, we are also battling inflation. This year inflation could be around 30% — it’s now at 26.6% — and next year it could be 28%. Of course, it’s the price of war. It’s the price put on the ability of our people to earn high enough salaries to support their families and lives.

But another price is poverty — the level of poverty could increase from 5% to 25%. It’s a huge, huge jump in the number of people living below the poverty line.

GlobalCapital: How much of your budget is going on military expenditure?

Marchenko: Up to 50%. This year, it could be 30% of GDP. Next year, it could be 18% of GDP.

GlobalCapital: And that presumably means you will continue to cut back on civilian spending?

Marchenko: Yes.

GlobalCapital: We have noticed with interest the C$500m Ukraine Sovereignty Bond being issued by the Canadian government. Is it a template you hope can be replicated next year?

Butsa: The mechanics are interesting because it ticks a couple of boxes. First of all it provides us with the necessary financing, but it also helps to channel the support from the regular people — retail investors, in this case, in Canada.

One of the things that our domestic war bond issuance showed was that there was a lot of interest from outside our country — not just from the Ukrainian diaspora — from different people asking if they could buy them.

Unfortunately, there is very little cross-border access to domestic markets for retail investors pretty much anywhere in the world. So what the Canadian ministry of finance has done is really that — they have given bond market access to its citizens who want to support Ukraine. We hope it will be successful.

The question is: where can we replicate this? It’s still a loan, though, and of course we do not want it to replace the grants we receive from other countries with the loans. But we will look at the demand for the Ukraine Sovereignty Bond issued by Canada and see whether we can replicate it elsewhere if there is demand in other countries.

GlobalCapital: You mentioned earlier reparations and that you very strongly believe Russia should pay for this war and all the damage it has inflicted on Ukraine. But what mechanism can you use to ensure that they pay what some are estimating could be $1tr of damages?

Marchenko: It is very much our desire for Russia to pay for the damage. One source, of course, is an amount of approximately $400bn of frozen Russian assets seized around the world.

However, I understand that it will take a lot of time, even if we have full support from our international partners. Maybe we can work on a way to use those frozen assets as a down payment on any reconstruction financing we receive in the short term. I believe we can seize this money, but the timing is unclear.

Butsa: In mid-November the United Nations General Assembly adopted a resolution that calls for Russia to pay reparations to Ukraine, which was very helpful. We are very committed to continue to work on the legal mechanics because we believe that those who created the damage have to pay for it.

Obviously, if Russia voluntarily agrees to repay then it’s much simpler than to force them. But if not, we will go all the way down the legal route to force them.

GlobalCapital: When I spoke to you in April, Yuriy, you mentioned that you had a large team of people accounting for the damage. Is that still the case?

Butsa: The damage is so much more than it was, but the team is much more sophisticated. The first report of its kind was published by the World Bank, which they did in co-operation with the team in Ukraine, including the Kyiv School of Economics, some NGOs, etc, who used satellite images of each and every building and quantified the damage based on the level of destruction of the buildings and businesses.

They identified $105bn of just physical damage, without economic loss, etc. Including economic loss and everything else, the number reached almost $350bn. Now, the more territories we liberate, the more damage we see.

Our army liberated Kherson recently and there is no electricity there — the Russians blew up everything, including the TV tower. So the number is going to go up, unfortunately.

But what we are doing now is a very precise calculation of what has been damaged, and verifying it so that we have a bill we can present to Russia to compensate us in full for the damage they have caused.

But such calculations can also help us to understand how we can prioritise what needs to be rebuilt. We know that there will not be a magic day in the future when we have all the money in place so that we can start reconstructing the whole of Ukraine. It will be a question of priorities.

We liberated the east of the Kharkiv region and of course people want to come back to their homes but they cannot return safely if they don’t have roads, electricity, running water or basic health services.

So, we use the scarce resources from the budget to do the basic repair work, such as to replace the bridge that was blown up for them to get back into their homes. This is happening right now because it’s important for these areas to be livable. So we need to constantly work on the damage assessment and prioritise the most crucial areas to channel the funds from the budget. GC

Bond market offers support

When Russia invaded Ukraine on February 24, members of the global financial community were shocked and appalled. Since then they have been searching for ways to help Ukraine and its people. GlobalCapital knows of individual debt capital markets bankers who assisted first hand — for example, by driving to Poland and Ukraine to deliver items such as nappies, toilet roll, chocolate, medicines and blankets amid the sudden influx of refugees. They also worked with NGOs and charities on the ground to help raise money for new transport to take aid into the country — and bring people out.

Another way the financial community has helped Ukraine’s cause is through bond markets. In August investors consented to a two year moratorium on repayments on $20bn of bonds, enabling Ukraine to avoid default and save money.

However, bond markets have also been used to raise new money too, often in imaginative ways.

In November the Canadian government issued a C$500m ($372m) five year Ukraine Sovereignty Bond, a first-of-its-kind deal designed to allow Canadian retail investors to show their support in denominations of $100.

The deal was in fact sold as a wholesale transaction, but with retail investors getting access to the bond via Canadian bank dealers and brokerages and their investment account platforms.

In the end, C$50m of the bond, which was fully backed by Canada’s AAA credit rating, was sold to individual citizens in one tranche, with the rest picked up in a second tranche by institutional investors, including bank treasuries, provincial central banks, pension funds and asset managers.

Overall, about 70% was sold to Canadian retail and institutional investors, while a large proportion, 40%, went to official institutions in Canada and in other countries, including central banks. Some investors told GlobalCapital that they treated it like a use-of-proceeds labelled bond, since it had documentation language about how the cash could be used by Ukraine.

The bond has a semi-annual interest payment of 3.245% and matures on August 24, 2027, Ukraine’s Independence Day. The Canadian Department of Finance will lend the proceeds to Ukraine through the International Monetary Fund Administered Account for Ukraine.

The country’s deputy prime minister and minister of finance, Chrystia Freeland, said at the Rebuilding Ukraine Business Conference on November 23: “Canada remains unwavering in our commitment to support the people of Ukraine in their fight against Putin’s illegal and barbaric invasion, and we will continue to do everything we can to ensure Ukraine has the resources it needs to win. Now, through a bond designated for Ukraine, Canadians can contribute to this critical effort through a new federally backed investment.”

Speaking to GlobalCapital, Adrienne Vaupshas, press secretary at Freeland’s office, added: “The Ukraine Sovereignty Bond was introduced to give Canadians an opportunity to directly support the brave people of Ukraine. The funds will assist the government of Ukraine so it can continue to provide essential services to Ukrainians this winter, such as pensions, the purchasing of fuel and restoring energy infrastructure. The deputy prime minister and the Canadian government are in frequent and regular contact with the government of Ukraine. As is widely reported, Ukraine continues to need financing and liquidity and this was a latest idea, from Canada, to assist in that regard. It also follows numerous loans on the part of Canada and G7 partners to address Ukraine’s urgent financing needs.”

Although Ukraine will be obliged to pay interest, the loan will respect the spirit of the debt service suspension agreed by Ukraine’s international creditors in August.

Fully subscribed

“Canada and its population want to help Ukraine,” says Alex Caridia, head of public sector markets at RBC Capital Markets in Toronto, and one of the bankers who helped design and execute the deal. “The transaction managed to attract a significant amount of retail investors, which was one of its key aims. Overall it was fully subscribed. It sends a really strong message to Ukraine that Canada is supporting it.”

Raising C$500m from the Canadian private sector, including directly from its citizens, will surely be seen as a success by Ukraine, although as Yuriy Butsa, Ukraine’s commissioner for public debt management, points out in the accompanying interview, he does not want foreign governments to replace grants with debt, even if it is priced at concessional levels.

As to whether Canada’s Ukraine Sovereignty Bond could be copied by other governments keen to help out, Caridia is optimistic: “This is certainly a model that other governments can build on, depending on the market they are active in and retail appetite in the respective market. It sets a good template.”

GlobalCapital understands that several other sovereign DMOs have since approached Canada’s Department of Finance for more information on the Sovereignty Bond.