This past year was not predicted to be particularly notable. The two years before were so unexpectedly volatile that 2022 was supposed to provide some respite. Not long into the new year, Russia put this idea to rest when it invaded Ukraine and sent the global economy into disarray. The multiple social and political headwinds that blew in were wholly unwelcome following the impact of the Covid-19 pandemic, but have forced the finance industry to adapt — and adapt quickly.

Unsurprisingly, the impact on investment banks specifically across the biggest markets has been grave. Several have already announced cuts, and more are expected.

The biggest schism of the year came in October, with Swiss bank Credit Suisse.

In January 2022, Credit Suisse CEO Thomas Gottstein promised a return to profitability. What a difference a year makes.

By the end of April, with war in Ukraine raging and inflation soaring, Gottstein lowered his ambitions and pledged instead “a year of transition”.

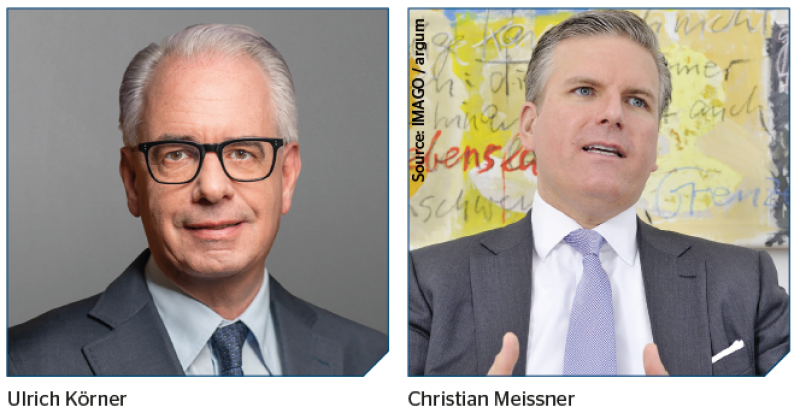

By July he was gone, replaced by Ulrich Körner. And at the end of October the bank unveiled a radical overhaul, selling off prized assets and handing over its investment banking and capital markets business to Michael Klein, a former Citigroup M&A banker who plans to float it as a separate entity by 2025.

Gottstein was right. It was a year that Credit Suisse would ‘transition’ out of investment banking. Indeed, the bank plans to cut 2,700 jobs by the end of the 2022.

The restructuring was a rapid capitulation, but at the same time one that was long overdue as Credit Suisse became the last European bank to adapt to the reality of the global financial crisis. While the decisions made today will reverberate over the coming years, Klein’s plan will really evolve over the next 18 months, with uncertainty stalking the bank’s corridors in London, Paris and Frankfurt.

The ripple effect is already being felt across the industry. Credit Suisse’s retrenchment fed the ambitions of others, as the fight for the crown of leading European bank intensified.

Most notably, BNP Paribas mopped up its prime services division and launched a three-point plan for growth which put expansion in North America at its centre. If everything goes to plan, by the end of 2025, BNP Paribas will have laid to rest the ghost of failed attempts by European rivals to conquer the US, while CS First Boston will be a New York-listed quasi partnership. If Credit Suisse is able to pull this off, Körner will be left reconsidering the deal with Klein earlier in the year.

Problems spun out of control for the bank very quickly as the year progressed. As former heavyweight boxer Mike Tyson once said, “everyone has a plan until you get punched in the face”. This past year was one where grand plans were thwarted for individuals and banks alike — and Christian Meissner, in particular, must be feeling punch drunk.

Having started the year as CEO of Credit Suisse’s investment bank with a remit to grow, he was sidelined in the strategy review and has now left the bank, raising the intriguing prospect of what he will do next.

War does not determine who is right — only who is left

Elsewhere, soaring inflation and war in Ukraine quickly reduced banks’ corporate finance plans to dust — hiring plans were frozen and strategic growth initiatives were put on hold as leveraged buy-outs curdled. Just a week after Vladimir Putin invaded Ukraine, Jane Fraser held her first investor day since being appointed CEO of Citi in 2021.

The event was supposed to be held in person, until Fraser and members of her executive team contracted Covid and moved it online. Paco Ybarra, head of the bank’s institutional clients group, set out his vision that included “leaning in” to leveraged finance. The bank had lost market share to rivals, which according to Ybarra was a result of a conservative risk appetite, something of a hangover from the financial crisis.

With the leveraged loan market freezing as Ybarra ran through his presentation slides, his timing could perhaps have been better, but as one senior banker told GlobalCapital at the time: “The only thing worse than not leaning into leveraged finance is having leant into leveraged finance six months ago.”

The war had a widespread impact. In May the news broke that Frédéric Oudéa’s reign as the longest serving CEO of a European bank was coming to an end, when he announced he would step down as CEO of Société Générale after his current term expires in May 2023. His departure came just a month after his decision to sell the bank’s Russian subsidiary, Rosneft, to Vladimir Potanin, following the invasion of Ukraine.

The succession race that followed featured a small field of internal candidates that set the former political adviser and head of strategy Sebastien Proto against the ‘outside insider’ Slawomir Krupa. Proto’s CV had been enhanced by his work restructuring the corporate and investment bank, which threatened to overshadow Oudéa’s legacy. In the end, Krupa prevailed, much to the surprise — and chagrin — of the French banking establishment. Known for his direct, no-nonsense style, Krupa — who previously ran SocGen’s business in North America — wants the CIB to expand globally, potentially setting it on a fascinating and uncertain journey.

The two-horse race to succeed Oudéa did not prevent the names of several high profile external candidates being bandied about.

HSBC in the crosshairs

One mentioned in dispatches was Georges Elhedery, who announced in January he was taking a six-month sabbatical from his role as co-head of global banking and markets at HSBC. But rather than serving as a precursor to an exit, Elhedery’s sabbatical provided him with the opportunity to recharge and upon his return he climbed the pecking order and was appointed CFO, replacing Ewen Stevenson. Having executed the heavy lifting of HSBC’s restructuring, Stevenson himself stepped down after he was passed over as a candidate to succeed Noel Quinn as CEO.

“Ewen was a great guy but, for all his skills, he was never going to be CEO,” says one former colleague. “HSBC always prefers insiders.”

Elhedery, who joined HSBC in 2005, is now seen as the leading candidate to replace Quinn — who, it is suggested, plans to stick around.

Quinn will have a lot on his plate at HSBC, which has grown accustomed to occupying a unique position in the crosshairs of Sino-US tensions, while navigating the challenges of being a UK listed and regulated bank that relies on the Asia Pacific region for 80% of group profits.

That challenge ratcheted up a notch for HSBC in 2022, when it emerged that its biggest shareholder, Ping An, was agitating for a break-up of the bank. HSBC, advised by Goldman Sachs and Robey Warshaw, quickly came up with a defence plan that involved reinstating the dividend, but it remains convinced its universal strategy is the right one. Ping An has shown no sign of tempering its approach.

Fruits of the loom

While Credit Suisse finds itself at the start of a major rethink, Deutsche Bank’s strategy is coming into focus. Three years after embarking on its own restructuring, the German bank proved this year that its transformation was complete as it posted its highest nine month profits in 11 years.

From being a near-basket case in 2019, the bank has regained its status as a top corporate finance house in its home market. Its progress was admired by Credit Suisse, which picked off the architects of its restructuring, hiring Dixit Joshi as CFO and Louise Kitchen to lead its wind-down unit, a job she performed with aplomb at Deutsche.

The bank was the biggest hirer of talent in 2021 as it plugged gaps. But, despite making progress, it continued to suffer departures from its senior investment banking ranks. Global head of advisory and origination Drew Goldman left to become head of real estate at Abu Dhabi Investment authority (Adia), while in London Richard Sheppard joined JP Morgan as co-head of investment banking. Chris Raff, head of UK M&A, left to join Moelis. Citigroup also hired Deutsche veteran Patrick Frowein as a vice chairman for its banking and capital markets unit in EMEA.

Overall, the pace of hiring eased in 2022 but banks continued to hire senior talent to fill gaps in industry or country coverage. The UK remained a fierce battleground as banks looked to beef up their presence in Europe’s biggest corporate finance fee pool.

While some rebalancing has taken place in other European locations, London has largely retained its status as a magnet for talent. Barclays began the year with a new executive team, following the appointments of CS Venkatakrishnan as CEO and Anna Cross as CFO, and has maintained the commitment to its investment banking business that was a hallmark of Jes Staley’s reign, which ended in November 2021.

Meanwhile, Jefferies, which has been the most prolific recruiter in European investment banking over the past decade, remained on the front foot with a fresh expansion — albeit with a counter-cyclical feel. In November, the bank hired Glen Cronin from Rothschild and David Burlison from Lazard as co-heads for restructuring in Europe, handing the pair a remit to expand the business.

BofA’s title challenge

Bank of America has enjoyed a resurgence in 2022, hiring bankers and winning market share as it looks to deliver on its mantra of being top three across all products and geographies, “with a relentless focus to be number one”.

Despite this lofty ambition, the bank has suffered its fair share of detractors. Last year, one former banker compared Bank of America to Premier League club Arsenal in the scale of its ambition. “In banking you have Goldman, JP Morgan and Morgan Stanley, and the rest. In the Premier League, it’s Manchester City, Liverpool and Chelsea. Arsenal are happy just to be top four.”

No doubt Bank of America will be keen to point out that Arsenal currently sit five points clear at the top of the Premier League, which happily corresponds to the year to November 16 corporate finance fee rankings, where it has leapfrogged both Citi and Morgan Stanley.

In July, Morgan Stanley promoted London-based Simon Smith to the role of global head of investment banking. Smith’s promotion was accompanied by a revamp of its senior banking set-up, as Morgan Stanley redeployed the current investment banking heads, Mark Eichorn and Susie Huang, to executive chairs of the division tasked with leading a newly formed group of senior bankers.

Meanwhile JP Morgan continued to refresh its senior ranks by looking outside its organisation for talent. Along with Sheppard — who joined from Deutsche — the bank hired Charlie Jacob from Freshfields to co-head its UK investment banking business.

Goldman switches

Goldman maintained its stranglehold in M&A, and also doubled down on its commitment to investment banking with an eye-catching revamp of its structure. Junking its distinctive investment banking structure — known across the Street as IBD — Goldman’s new strategy looked more like its rivals. The reasons for enduring years of tradition and creating global banking and markets was, according to CEO David Solomon, simply a reflection of close collaboration of the bank’s corporate finance and trading arms under his One Goldman Sachs strategy.

Solomon’s decision in November to promote 80 professionals to the bank’s coveted partnership pool in October — the highest number since 2016 — points to a shake-up of the established order in 2023. Some suggest that some underperforming members of the old guard will be “de-fanged”, which is Goldman-speak for losing partner status.

After a dire first half for corporate finance activity, when equity capital markets fees plummeted by as much as 80%, some bankers warned of job cuts on a scale with the aftermath of the dotcom boom in 2001. But so far banks have adopted a cautious tone.

In October, Goldman Sachs became the first bank to break cover by cutting underperforming staff, but — with the exception of Credit Suisse — rivals have so far opted to prune and trim rather than slash and burn, for fear of being caught flat-footed when markets turn.

Despite all the gloom and uncertainty, there is a flicker of optimism. But the time to judge what 2022 really meant for the shape of the investment banking industry will be in years to come, as the dust settles on a tumultuous year. GC