The bizarre and unprecedented experience of Brexit is reaching its climax. Living through this rolling carnival of events and clashing opinions is like watching a surreal film — the happenings are wild, nothing makes sense and we have no idea how it’s going to end.

Brexit might be called off altogether; the UK might skid over the cliff and leave the European Union without an agreement; the whole thing might get delayed; or the deal negotiated by Theresa May might be implemented, leading to a sudden flooding back of the reassuring sense that British pragmatism wins out in the end and a workable compromise is always found.

Whatever happens, historians will make it look like the outcome was inevitable. We, in the middle of it, know the opposite is true.

Curiously, considering how sensitive and prone to over-reaction they are, financial markets have been remarkably calm so far. And the way financial players are preparing for the legal and operational changes Brexit will bring is also fairly ordered, compared with the chaos in the political sphere.

Essentially, this is because financial firms have to plan, operationally, for the worst possible outcome — a no deal Brexit. Failing to do so would be grossly irresponsible. At the same time, no one involved wants that scenario, if it happens, to be a disaster movie — so it will not be one.

“This is a one-off seismic event which is unprecedented,” says Etay Katz, financial services regulation partner at Allen & Overy in London. “It creates a need to be accommodating for a period of time. If regulators stick by the letter of the law they will not allow much business to be conducted. They have to flex the rules to allow for an orderly transition.”

Flying without a passport

Every investment bank in Europe’s capital markets has been making sure it has the requisite permissions to carry on business in the EU if the UK leaves without a deal. That would mean the UK losing its passporting rights and becoming a lawless alien, as far as EU regulators were concerned.

“It is very clear that the passport is required for a great variety of so-called investment services,” says Katz. “These are services in securities and derivatives which include underwriting, intermediation, sales, acquisitions, primary and secondary market activities.”

In practice, all firms of any size will need to establish a subsidiary in an EU country, with the relevant licences for the business it wants to conduct, thereby gaining access to the whole EU market through passporting. And this is what they have done. A subsidiary is a separate company, which can be regulated in the country in which it is based. A branch has no legal personality and is just a limb of another entity, which may be overseas and regulated in another country.

A choice of red carpets

Setting up new subsidiaries, or repurposing existing ones, is achievable, though not easy or cheap. Regulators in every EU state are eager to welcome new arrivals. One thing has become much clearer: which cities will benefit from business moved out of London. For virtually all banks, it is one of four cities ringing London: Paris, Frankfurt or Amsterdam, plus Dublin for administrative, rather than front office business. It will not be winner takes all: each will gain substantially.

Luxembourg will increase its existing role as the venue of choice for registering investment funds. One headhunter says Frankfurt is picking up a lot of the administrative jobs that go with this, though, as it is cheaper than Luxembourg.

The next question is much more difficult. How many and which of the staff serving EU clients need to be based in the EU? This is an immensely complex issue, considering the great variety of investment banking services, regulated under different regimes, and the global nature of capital markets.

“There is no hard law that says ‘if you have this sort of business, you must have those sorts of people dealing with it’,” says Simon Gleeson, partner in the financial services practice at Clifford Chance in London. “This is not a point that the European authorities have been particularly interested in.”

All the banks know it is not enough just to put up a brass plate in Frankfurt and move a couple of compliance people there — even if the deal-doers left in the UK now work for a branch or subsidiary of the Frankfurt entity.

“Everybody has the same rules, including the UK,” says Gleeson. “If you are going to have authorisation to operate on my territory, that business has to be run from my territory in such a fashion that I as regulator can monitor it and get my hands on the people doing it if I need to, and ensure that there is sufficient capital in my jurisdiction if something goes wrong. Those principles are common to everyone, so the question for the host supervisor is simply: ‘what does “enough” mean in this context?’”

Bagsy not me

Not even the regulators have a settled answer yet. As for the investment banking world, it is thick with different ideas.

Some believe trading and salespeople are the only ones who need to move — advisory and origination bankers can stay in London. Others say risk-taking executives need to be in the EU; or that client coverage bankers must be. Are debt capital markets bankers client coverage? Or can that role be taken by local corporate bankers, with DCM acting as a team of product experts, flown in from London to advise on details?

The bond syndicate function is a particular puzzle, combining as it does elements of risk taking, product expertise, client advice, deal origination and sales. Some banks are moving syndicate people to the EU, or have a contingency plan to do so; others deny this is necessary.

For the time being, very few bankers are contemplating moving, and even fewer have actually gone. “The assumption is that there’s going to be a deal, so this will be a 2020 issue, not 2018,” says Gleeson. “Every time we’ve looked at it, the view we have come to is that the proposed numbers are getting smaller rather than larger. What the European regulators are saying is the minimum necessary staffing to get and maintain an EU authorised subsidiary. I’m not aware of anybody who’s planning on moving significant numbers of people.”

But regulators certainly have the power to demand more. “A reasonably small European firm, with a disproportionately large and senior staff sitting in London, would be a very unpalatable story to sell to the home regulator,” Katz says.

A desire to avoid this “fat branch” syndrome is why, he says, the big banks have not so far converted their UK operations into branches of their new, much smaller, EU 27 subsidiaries.

There are two reasons why there are no simple answers. First: no country has ever left the European Union before. Even the existing arrangements for non-EU banks operating in the EU do not provide useful precedents. Nearly all have EU subsidiaries or branches, which, in practice, hold most of their staff active in Europe. Some may be dispersed across the continent, but the subsidiary’s host regulator has never minded, since the chain of command ran through the European HQ.

As for staff outside the EU serving EU clients, on a substantial scale, there is little or no precedent for it.

The EU does have an equivalence regime — a system for deciding that a foreign country’s financial regulatory system is equivalent to that in the EU, and hence that services can be provided cross-border. But the only zone in which it has been used is central counterparty clearing — something very relevant now to the fate of LCH, the London clearing house for most swaps. In the MiFID II world of investment firms, no country has ever been declared equivalent.

The result is that regulators are having to decide how many staff are “enough” as they go along.

And here comes the second reason this is confusing. Each EU country has its own regulator, making its own decisions. The result, not surprisingly, is a wide dispersion of outcomes.

Add a dash of politics to the mix — regulators feeling they must be patriotic and woo bankers to their office towers and restaurants — and there are incentives both for regulators to be lenient to firms, to attract them, and later to crack the whip, insisting they bring over more bankers.

Katz says that for more than a year now, the European Central Bank has been trying to get a grip on this process, so as to rein in the regulatory divergence and make sure regulators do not cut banks easy deals. “That has slowed the process of new authorisation down quite considerably,” says Katz. “Any new bank application is processed by the local regulator but is ultimately granted by the ECB these days. There is some leeway, but on concepts like the brass plate and outsourcing, you should expect a level playing field, although it is far from straightforward for the ECB and Esma to achieve that.”

Reluctance to move

This muddle hardly sounds like the orderly transition referred to above. Yet there are two other forces acting on the situation and keeping it contained.

One is inertia. The banks, at this stage, want to move as few people as possible. This is not out of principle (as if!), but to avoid the costly and potentially disruptive fragmentation of activities between different centres. And much more powerful than that is the immense difficulty of moving large numbers of highly skilled and paid staff to another country.

Recruiting locally on the continent is impossible. The local talent pools are much smaller and any suitable candidates were snapped up months ago. But how many bankers want to move, when they have partners with jobs in London, children at school, homes and friends?

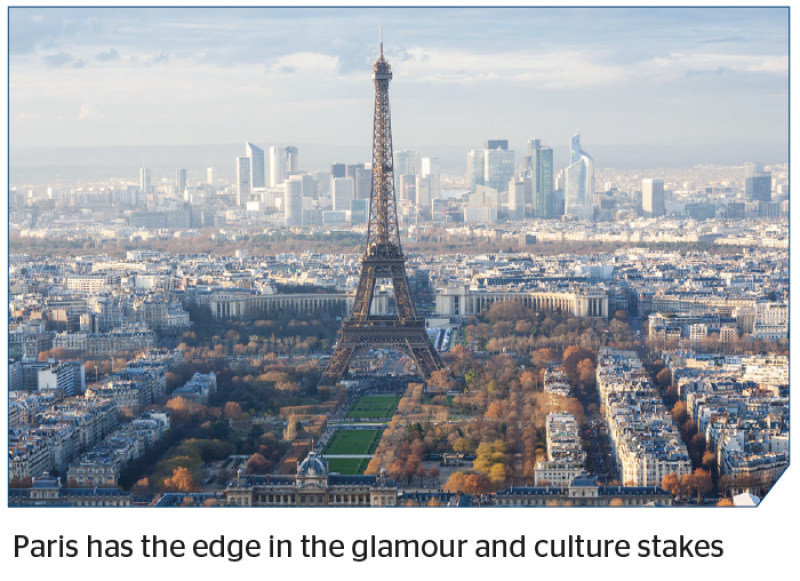

Many will end up being weekly commuters, and this, together with its edge in the glamour and cultural interest stakes for those who do move, means Paris has an edge in the race. Two and a half hours on the Eurostar, with wifi some of the time, are preferable for most to traipsing through miles of departure lounges at Frankfurt or Schiphol.

France, with an investment banker as president, has also been on a charm offensive, offering breaks from France’s high personal tax rates. “Somebody described it to me as ‘trust us, we won’t behave like the French’,” said a capital markets specialist.

Early on, some banks thought they could save money by this process, swapping expensive London bankers for cheaper ones on the continent. With a few exceptions — European banks pulling people back to their domestic HQs — that now seems laughable. Bankers are having to be bribed to move, with hefty relocation packages, including school fees and housing allowances. All of this is pure cost for the banks, with no upside in higher revenue potential. They are likely to claw it back by making job cuts before long.

One tactic banks could try so as to avoid moving staff may be to use an outsourcing model. The Amsterdam entity, for example, could buy in services such as DCM expertise from the London unit, much as banks already outsource business processes to India.

Cards in the hand

Acting against this friction is the second force — the power of national and EU regulators to compel banks to move assets, staff and capital to the EU. They have time on their side, and just about everything else.

But opinions diverge about how this tug of war will play out. Gleeson paints a fairly benign future for London. If a Brexit deal similar to May’s is agreed, the UK will leave on March 29, 2019 with a transition deal, keeping its passport until 2020, or longer if transition is extended.

“If at that point what is agreed is an equivalence regime, then nobody has to go anywhere,” says Gleeson.

Others see serious obstacles to that. “The processes are irreversible — nothing is going to be halted,” says Katz. Even if May’s deal were passed, the best outcome he can foresee for London is that “the migration of activity will be orderly rather than chaotic — a proper transition from where we are now to a position where the passport is no longer available”.

“Equivalence in its current form works only for an insufficient volume of the business, and would need to be expanded very substantially to be underpinning business models,” says Katz. “Even the expansion of equivalence which is potentially on the cards would take years to work out.”

In any case, he adds: “the Europeans are now rethinking the whole concept and whether they need to place further safeguards, rather than relaxing the regime”. Some countries have talked of requiring line-by-line equivalence of legislation, a much more stringent test than equivalence of purpose.

It is not clear what incentive the EU side would have to play ball with the UK, and an equivalence deal would oblige the UK to keep its financial services laws very close to the EU’s forever.

Gleeson sees mileage in it, however. He argues that the political declaration agreed by May with the EU sets down that if an equivalence arrangement is agreed, any change to it would be based on formal consultation, ensuring that it could not be ended arbitrarily, but only after due process and with appeals.

“If the choice is between worrying about an extremely unlikely event [an abrupt end to an equivalence deal] and having to mess up your business by moving hundreds of people around the continent, I can’t imagine many going for the latter,” Gleeson says.

The long withdrawal

The opposite view is that no bank would want to take the regulatory risk of waiting for the equivalence deal to be negotiated and then relying on an arrangement that could be seen as politically fragile. Meanwhile, the regulators in the EU would use their power to gradually crank jobs across the Channel.

Katz delineates three phases. In the first two years, he argues, a skeleton staff will go, to get the EU subsidiary going and show good faith to the regulator.

In the second two year period, “the authorities in Europe will start insisting on more staff being onshore in Europe, as the banks in Europe ramp up their balance sheets.”

What happens after that will depend, Katz argues, on whether local “ecosystems” of talent have developed in Paris, Amsterdam and the others, which “start having their own dynamics”.

In his view, “We are going to land somewhere much more pragmatic than the legal texts suggest. London is not going to be reducing its dominance any time soon.” However, over a long period, chunks of the business will be broken off as it will no longer be feasible to run them from London.

Bankers are, rightly, focused on the short term — on making sure their businesses can continue to function through the coming weeks and months. They are trying to keep things the same as much as possible, and many believe they can get away with only superficial change. In any case, there is little point making plans for what might come further ahead.

But many signs point to a very different investment banking landscape in future. Europe may have five banking cities instead of one — unless Paris or another becomes pre-eminent and acts as a centre of gravity, because all the heads of DCM or investment banking want to be together at the heart of the action.

Ironically, a Brexit enacted at least partly to stem a tide of immigration from the EU looks likely to end with Britain desperate to avoid losing people.