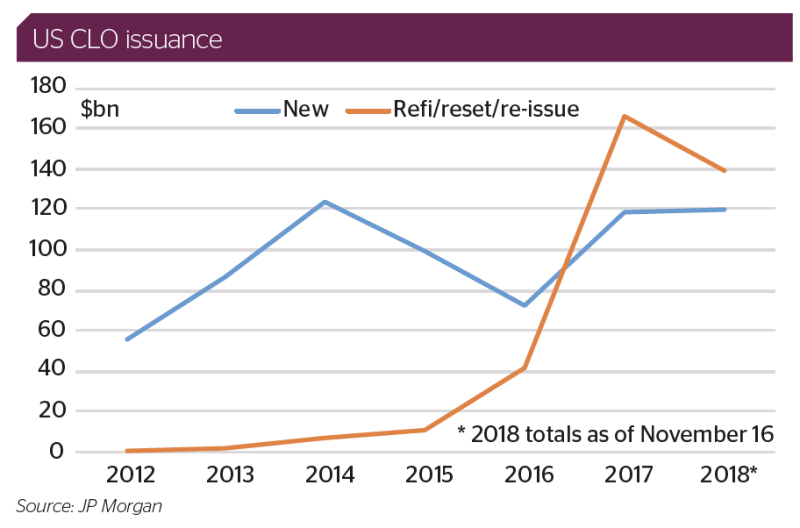

A host of competing factors in 2018 drove CLO activity, in terms of both issuance volume and movement in triple-A debt spreads. A “pig in a python” scenario gave investors a huge wave of CLO reset paper to sort through in the April and July payment date windows, with about $23bn of CLOs reset in each of those periods, according to Gretchen Lam, senior portfolio manager at Octagon Credit Investors. That number dwindled as the year wore on, but the heavy supply helped push triple-A spreads out from near post-crisis tight levels of 92bp over Libor in February to around 117bp toward the end of the year. Octagon tapped the market 14 times in 2018 between true new issue deals and refinancing and reset transactions.

“As we look to 2019, the big question for us is where do triple-A spreads go. That will drive the pace of supply,” says Lam. “CLO issuance is only a function of where triple-As price and do the [equity investors] care at that level. Everything else in between is just a pricing exercise.”

Meanwhile, Japanese investors, who have often anchored the order books for new CLOs at the triple-A level, pulled back as hedging between yen and dollars became more costly in 2018. Many Japanese institutions moved on to European CLOs or US CMBS where net returns were stronger over the course of the year.

Another change in the investor base saw short duration bond funds, which piled into the market in 2017, pull back as deals they were invested in were reset into new five year structures throughout 2018. According to Tom Majewski, managing partner at CLO equity investment firm Eagle Point Credit Management, the five year tenor was not a natural fit for these funds, and this technical change in the buyer base also weighed on CLO spread levels.

“We actually got out of sync over the course of the year, where the loan market was stronger than the CLO market simply because we were paying back a lot of these short term buyers,” Majewski says. “Our outlook is certainly to see triple-As tighter in 2019.”

Macroeconomic factors, such as the pace of interest rate hikes by the Federal Reserve will also have a hand in shaping supply and demand for CLOs. The market is pricing in three increases in 2019. To the extent that changes, that will have an effect on investor appetite, Majewski adds.

Given some of the uncertainty around key issues such as the size and shape of the buyer base next year, the pace of leveraged loan issuance and movement by the Fed, issuance predictions for 2019 are varied. 2018 activity was brisk, with outstanding paper increasing by 11% by the end of November, but the market could have trouble reaching 2018’s volume if macro and market specific factors do not line up.

No covenants, no problem?

But while triple-A debt spreads and overall issuance levels are certainly on everyone’s mind as 2019 kicks off, there is equal attention being paid to the state of leveraged loans, from the standpoint of both pricing and loan covenants.

The proliferation of cov-lite loan documents seen over the past two years intensified in 2018, leading to a deluge of negative press coverage about the state of what some have identified as the trigger point for the next financial crisis. Investors meanwhile have bemoaned the state of loan documentation but have also accelerated the spread of cov-lite loans with their near insatiable appetite for floating rate debt.

One particular ‘bad boy’ loan covenant that received a lot of attention over the past 12-18 months, and which observers say they expect to see more of in 2019, allows borrowers to move assets out of the reach of first lien creditors and pledge them as collateral for new debt. Clothing retailer J Crew has been a high profile example of this practice. However, instead of recklessly overleveraging and spiraling into insolvency, J Crew used the ability to take on new debt judiciously, keeping up with payments and inspiring enough investor confidence to push the price of its first lien debt in the secondary market from 50 cents to over 90 throughout the course of 2018.

“We’re pretty optimistic that covenant-lite will actually delay the onset of the next default cycle… While actual loan prices may be volatile, the actual instance of defaults will be low in 2019,” says Majewski.

The agonizing over deteriorating loan covenants, observers say, has to be taken in hand with the fact that corporate earnings are strong. As long as the economy keeps humming along in 2019, these loans will continue to perform.

Maureen D’Alleva, managing director and head of performing credit at Angelo Gordon, also says that the market is holding the line against the most aggressive practices.

“Credit selection is really the key [for CLO managers] as we navigate through the last innings of the credit cycle. We have inflationary pressures and tariffs that will add another element of costs for companies,” D’Alleva says. “What you see in the press is a change in the credit protections that we’ve had. Documentation has become pretty aggressive but we’ve been disciplined in pushing back.”

Still, cov-lite is problematic enough that most of the market agrees that loan recoveries will be lower when the cycle does turn. This possibility is front and centre for hedge fund Ellington Management, which both invests in and manages CLOs. The firm’s CLO management unit takes a much harsher view of the cov-lite environment that the market now operates in.

Greg Borenstein, portfolio manager in Ellington’s CLO management group, says that while the firm buys lower rated credit to pool in its CLOs, 70%-80% of the loans it buys have stronger covenants and documentation and Ellington is positioning for a turn in the cycle when a wave of triple-C downgrades pressures the market.

“When these downgrades do hit, it will be a slow motion train wreck. We also think there is a some false sense of security in these deals given how short lived the distress was in the loan space during the crisis and given how much room there is to benefit from floating rate product,” Borenstein says. “The lesson learned about how resilient these deals are is the wrong lesson to take away in our opinion.”

Rob Kinderman, partner and head of credit strategies at Ellington, echoes his colleague’s sentiment.

“We are actually more concerned about cov-lite than most of the market and have been for years. The reason we stay in more structurally strong mezzanine paper is that we see the data and the leverage is moving up and documentation continues to get worse. As we see it playing out, we expect recoveries to be a lot lower,” says Kinderman.

Ellington’s strategy is to buy loans in the secondary market that are more seasoned, focusing on paper with maybe three or four years left to maturity.

“Buying these loans in secondary is like taking a time machine back several years to what documentation used to look like,” says Kinderman.

The PE perspective

Private equity firms’ leveraged buy-out activity will continue to drive issuance of the leveraged loans needed for new CLO formation. High profile LBOs, such as Blackstone’s deal to buy the financial and risk unit of Thomson Reuters for $20bn and Carlyle Group’s buy-out of the specialty chemical unit of Akzo Nobel for $12.5bn, were highlights of the leveraged loan market in 2018.

However, rising costs for floating rate borrowers and a more uncertain corporate earnings backdrop generally could eat into new loan volumes.

Angelo Gordon’s D’Alleva says the refinancing and reset opportunity for managers will be much smaller in 2019, therefore CLO issuance will be lower. Additionally, CLOs will be more dependent on LBO activity, as she also expects loan refinancings to be lower over the course of the year.

Still, for private equity firms with a CLO strategy, the sector will remain attractive, particularly at the CLO equity level where returns on those investments since the financial crisis have outpaced other asset classes.

“We think it is a well structured asset category,” says Bharath Srikrishnan, managing director at private equity firm Pine Brook Partners, which invests in energy and financial services related companies.

Pine Brook owns the Dallas, Texas-based CLO manager Trinitas Capital Management, which issued two new CLOs and one reset transaction in 2018.

For Srikrishnan, concerns as 2019 gets underway are similar to those voiced by other participants. He says that the scrapping of the risk retention requirement for CLOs was a negative. From a macro standpoint, the cycle is getting long in the tooth.

“We’re in the eighth inning but we don’t know how long the ball game will be and to what extent external shocks like trade wars and rising rates play into credit performance.”