Private equity firms in Europe, and by extension CLO managers, are in a pinch.

Sponsors are sitting on heaps of assets that they are meant to exit, by selling them to companies, other PE firms or public equity investors through an IPO.

The CLO market is ready and eager to support leveraged buyouts. Enormous demand for the relatively attractive yield of CLO tranches is driving issuance, and squeezing spreads on new deals — last week to a new two year tight for triple-A notes of 134bp over three month Euribor.

But raising cash, at the moment, is the easy part. CLO managers are struggling to find assets to fill their portfolios.

New leveraged loan issuance is slow and the secondary market has become expensive, with around half of the European Leveraged Loan Index trading above par.

Leveraged loan bankers say they are having intensive discussions with private equity clients behind the scenes, but they have not yet translated into deals.

While CLO issuance could break the 2021 record of €38bn this year, leveraged buyout activity and other M&A by private equity-owned companies is still significantly lower than at its recent peak during the long spell of zero interest rates.

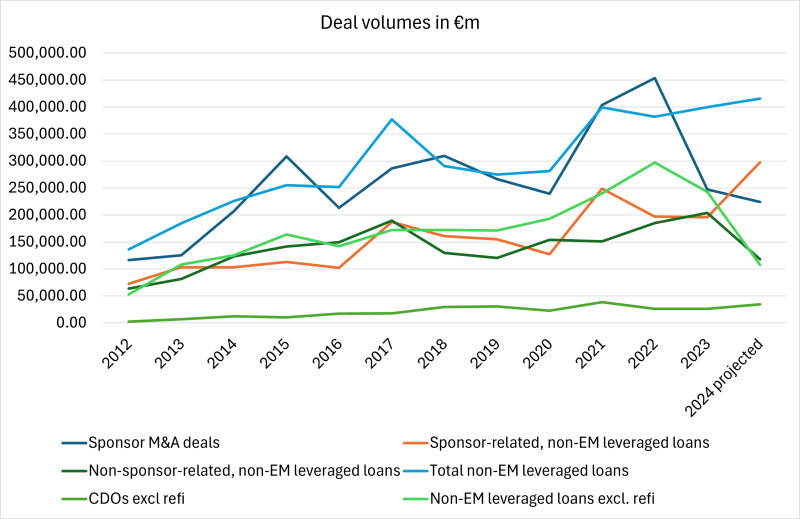

(See graph using Dealogic data. GlobalCapital reached the projection for 2024 by doubling the figures for this year to June 24 — admittedly not the most sophisticated modelling. But as bankers’ predictions for an LBO revival have been wrong for the past two years, it seemed as good a guess as any. Data analysis by Jon Hay and Victoria Thiele)

At the moment, when a private equity firm tries to sell a company, it tends to attract fewer investors than before, and prospective buyers are quicker to drop out of the process.

That is partly because other sponsors are cautious about deploying capital. One banker said firms were nervous to close a major deal and read in the press the next day that they had overpaid. Private equity buyers are spending more time on due diligence, and are more concerned about being able to make their own exits in a few years' time.

Add in an oversupply of sellers, and it becomes hard to negotiate a price that works for both sides.

It is a tough situation for private equity firms, M&A bankers and the CLO market. But it offers some relief to the wider ecosystem of companies and their employees.

“For the first time in a very long time, the situation feels balanced in the M&A landscape between private equity and corporates,” said a senior debt banker in London. “In 2021, PE had access to cheap funding. They were willing to really pay up for assets, so they constantly outbid corporates. Then things got trickier in the leveraged finance markets and PE couldn’t raise the financing, so corporates didn’t have much competition from PE buyers. Today, for the first time in a while, it is relatively balanced in terms of competition between corporate and PE.”

Companies tend to acquire other firms because they see long-term, strategic value in the acquisition. They understand the industry, they can create value through synergies and innovation and they have an interest in the companies they buy as real businesses. They also usually pile less debt on to their new purchases.

But to a private equity firm, the most relevant aspect of the company is to generate the highest possible return upon exit after three to five years. The pressure to grow rapidly for external profit’s sake can come to the detriment of the employees’ daily experience, especially when they are not given equity to align their interests with their owners’.

Arguments that private equity is beneficial to economies are weakened by the fact that the favourable tax treatment of carried interest — fund managers' incentive payments — as capital gains rather than income has enabled the largest firms to pay light taxes on more than $1tr of earnings since 2000, according to a recent Oxford University study.

A corporate acquisition is not necessarily better than a takeover by private equity. The PE owner can have better incentives to maintain and invest in the original brand, at least for the time of its holding, and to lead it on a disciplined, focused growth path.

A merger with another company from a similar industry means job cuts are likely as certain roles are duplicated, and it can be difficult to combine cultures.

But it is good for a stable and diverse economy if the different kinds of buyer compete on a more level playing field. Private equity will always be the right choice for some companies, especially if they are not ready to be a strategic target or to float on the stockmarket. But it should not be the no-brainer option because sponsors can pay inflated valuations in a spiral of PE-to-PE sales fuelled by cheap money.

Fortunately, there are signs that private equity firms are also adapting their strategies to the new economic cycle.

A leveraged loan banker said sponsors were increasingly trying to pursue buy-and-build approaches with longer timeframes, in which the annual income they can generate from portfolio companies plays a bigger role.

As GlobalCapital reported in an article on this shift in April,

KKR created KKR Strategic Holdings in November, a new business that will hold assets with a long duration and lower leverage over time. In an investor presentation in April, KKR said it aimed to generate at least $1bn of annual operating earnings by the end of 2023.

CVC has had funds with holding periods of around six to 15 years for a while, but it activated its Strategic Opportunities III fund on May 3, the earlier end of the estimated mid-2024 timeframe.

Partial exits where private equity owners retain a minority stake in a company may also become more common. One recent example is Permira’s sale of a majority stake in Universidad Europea to EQT in April. This allows an owner to realise some returns but keep benefitting from the company’s future development.

Both trends would incentivise private equity owners to balance the swift maximisation of a company’s potential with a longer term vision.

Short-term pain for sponsors that bought companies at peak valuations in 2021 seems unavoidable, since for the time being, central banks show no inclination to cut interest rates back to nothing.

But prices could not have gone up forever anyway. At the very least, today’s set of circumstances allows private equity firms to transition to a more diverse and sustainable range of business models.

And when they choose to use debt, they can count on the support of a CLO market dying for deals.