An array of securitization market participants told GlobalCapital that they will use Global ABS in Barcelona next week to gauge whether a deterioration in pool performance is likely this year.

High inflation, and hence rising rates and the rising cost of living, has triggered worries that the performance of securitized assets will worsen. Despite all the talk, spreads have tightened in several asset classes so far this year.

For example, Belmont Green priced the first UK BTL RMBS of the year at 150bp over Sonia in January. It also priced the most recent such deal at 115bp over Sonia on May 25.

“It’s going to be really interesting to get people’s takes on underlying pool performance because I think it’s not obvious from the market that people are particularly concerned,” Janet Oram, head of ABS at USS, told GlobalCapital.

Another investor said: “We are meeting a bunch of different originators. We want to understand if they are seeing increased defaults in all the different asset classes. We also want to understand the pressure on LTVs.”

Matthew Jones, S&P’s commercial head of EMEA structured finance, wanted to understand the views of the investors themselves.

“[It will be interesting to see] how investors are viewing the performance of the asset class,” he said. “It’s been extremely robust over the last 15 years from a default and rating stability point of view, but the worst is yet to come from a recession, employment numbers and the expectation of a lot more volatility.”

Oram also thought the period of stability made the possibility of deterioration particularly interesting.

“Getting people’s views on what is coming down the track and how it’s going to impact the market is going to be quite interesting,” she said. “For the last 10 years asset performance has largely been pretty benign. Getting people’s take on how they are thinking about [rising rates], what they’re putting into portfolios and how they’re actually lending will be interesting.”

Most in the market agree that there will be a deterioration of some nature, but there is uncertainty about which asset classes will be affected and how severe that deterioration could be.

Oram said securitization structures are designed to protect senior investors, so even though she expected some deterioration, she thought investment grade tranches would fare well.

“My personal view is that there is going to be a deterioration in [underlying pool] performance,” she said. “We’re already starting to see arrears go up and CPRs [conditional prepayment rates] come down. But then you’ve got to overlay the structures, the tranching and all the various triggers. I think from a credit perspective the transactions themselves (particularly in IG space) will be largely fine.”

Indeed, Duncan Paxman, senior director of European structured finance at Fitch told GlobalCapital, that UK RMBS ratings were unlikely to come under pressure because ratings build in headroom.

“Our ratings methodology has headroom for both defaults and house price decline,” he explained. “The headroom is more than we think is actually going to play out this year [in both cases].

“From a securitization perspective, the real deterioration risk is in the legacy non-prime pools. Those transactions are backed by pre 2009 collateral, all floating rate, predominately interest only. Arrears in those pool are starting to move higher [on average we’ve seen late-stage arrears move up in those pools by 1.4pp in the last year].”

However, Paxman thought that mortgages were less likely to fall to arrears than other asset classes and so the discussion in Barcelona would be focused more on unsecured credit.

“Mortgages are not going to be the first place that the impact [of rising rates and cost of living pressure] is seen and it's not going to be the most significant deterioration," he said. "You're likely to see unsecured consumer [products] for example being impacted first. In Barcelona, we think in conversations around performance deterioration, mortgages will probably be further down the list than some other sectors where you tend to see performance deteriorate more rapidly.”

In contrast to much of the public markets, SRT spreads have widened, but James Parsons, partner in PAG and an SRT investor, told GlobalCapital he still wanted to gauge expectations for asset performance in Barcelona.

“Is recession coming?” he questioned. “Will default rates pick up? When is that likely to occur? SRT spreads have widened over the last nine months, but the question is, have they widened enough? It’s always interesting to get a temperature of people’s expectations. You get a good idea of what people feel [in Barcelona].”

Inflation underestimated

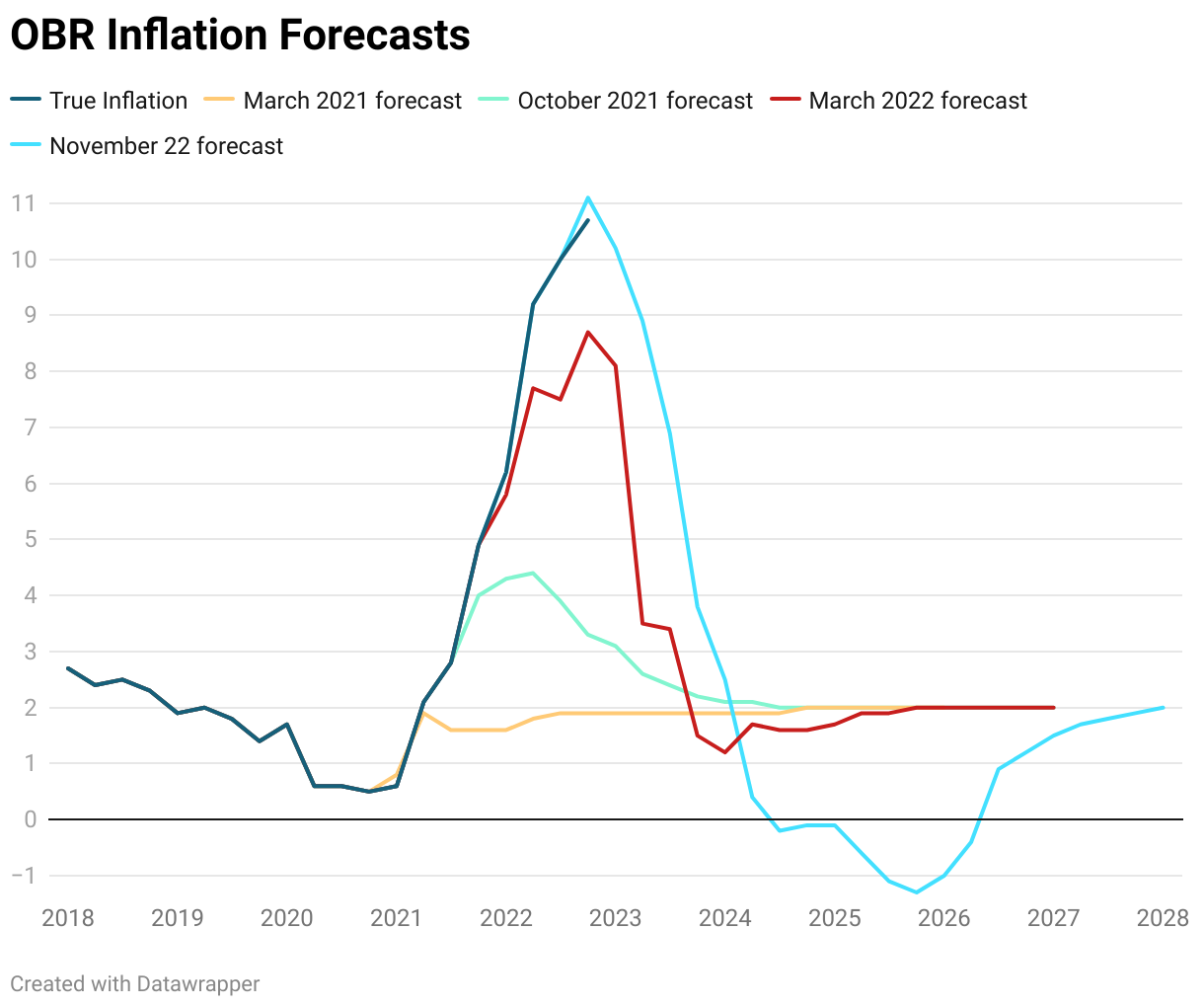

One thing that will add to worries about pool performance is that forecasters have repeatedly underestimated how sticky inflation is and that has meant peak interest rates have also been underestimated. As one example, the graph below shows recent forecast of UK inflation from the Office for Budget Responsibility.

“It looks like interest rates will peak higher than we thought they would two or three months ago,” Paxman said. “That will potentially lead to more deterioration in performance with the worst point coming in 2024.”

Indeed, the scale of the problem is could still be underestimated and that could cause a recession.

“We take the view that inflation is going to be much harder to quell than some of the current expectations,” Parsons said. “Rates will be higher for longer and increase default pressure. We think there will be more than a very soft recession but probably not a hard recession. Somewhere in between the two.”

Many will hope to have a clearer picture of just how likely that is after the conference.