On October 10, the European Commission published its report on the functioning of the EU Securitization Regulation (EUSR) and the reaction appears to have created a consensus of exasperation and despair.

“Pure frustration” was how one market participant put it. “Disappointing,” said another.

The EUSR was described as regulatory “overkill,” while one lawyer said EU regulators “completely ignore” any argument that suggests the EUSR may have something to do with the sector’s stagnant growth.

A major concern, held by many market participants, is that this is not a case of ineptitude, rather that it’s exactly what Commission seeks to achieve. Put simply, participants suspect that regulators do not want to see a growing European securitization market, but they don’t want to publicly admit it.

It’s becoming increasingly difficult to come to a different conclusion.

The Commission says in the introduction of its report that securitization is an “important tool” for capital, liquidity and risk management in banks, but also provides “diversified investment opportunities” for long-term investors.

It goes on to say that creating a “flourishing” market of high-quality securitizations is needed, and that they had committed to “reviving” the EU securitization market following the global financial crisis.

However, as one bank researcher diplomatically put it, it goes on to be quite “contradictory”. Sources have suggested that it continues with some rather bizarre and frankly unrealistic statements.

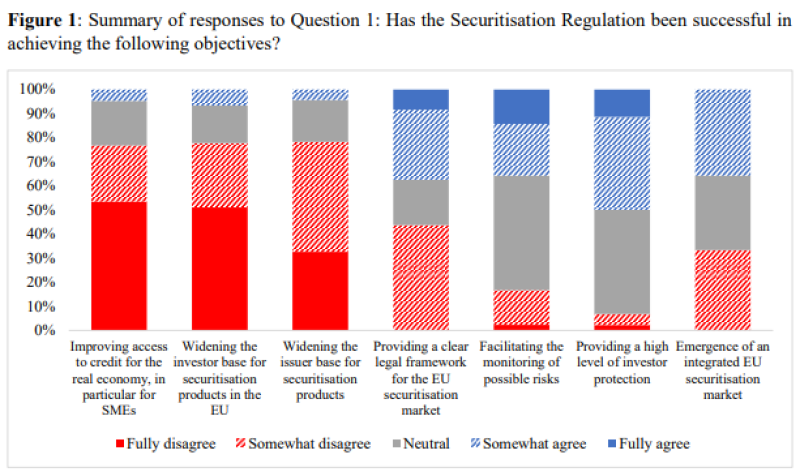

Below is an image from the report. It shows market participant responses to the question of whether the EUSR has been successful in achieving its objectives.

For improving access to credit for the real economy, widening the investor base, and widening the issuer base, the response from the market was a resounding “no” with around 75% of respondents either “somewhat” or “fully” disagreeing.

In fact, the only question where the majority agree with the Commission was in providing a high level of investor protection.

It’s slightly bizarre then that Commission’s report states, without any supporting evidence (that we could fine anyway): “Most respondents to the consultation were generally supportive of the existing legal framework.”

The report goes on to “acknowledge” the “muted” feedback but concludes the EUSR “seems overall to be fit for purpose and does not see the need for major legislative change”.

As the 27-page report continues, it develops a great habit of “acknowledging” concerns and then seemingly ignoring them in its assessments and recommendations.

The report says the outstanding balance of securitization transactions in the EU decreased by 11.9% between 2015 and the end of 2021 (the EUSR came into force on January 1, 2019) but that the US market grew “substantially” in the same period.

To summarise, the Commission, which received 56 replies from European securitization stakeholders in its consultation, is aware that the vast majority of respondents believed it has failed to improve access to credit in the real economy, widen the investor base for securitization or widen the issuer base for securitization.

It is also aware that the between 2015 and 2021, the European market shrunk by 11.9% while the US market grew rapidly. An exact figure is not given but as a guide, but in January 2022 S&P Global said that US new issue volume grew by 209% between 2016 and 2021 — from $373bn to $783bn.

Yet despite this, the Commission concluded: “The Securitisation Regulation seems overall to be fit for purpose and does not see the need for major legislative change at this juncture.” All that’s needed is “fine-tuning”, the report said.

That’s a mind-boggling conclusion to draw and will not address any of the actual issues at stake.

Onerous

The main bugbear for market participants is in just how onerous the EUSR is. It requires huge amounts of data to be provided in complicated (and often unnecessary) templates.

Last week, Allen & Overy partner, Salim Nathoo said the quantity of data required in securitization transactions was "disproportionate".

Meanwhile, the Simple, Transparent and Standardised (STS) quality hallmark for EU securitizations — a flagship regulation from the EUSR — was seen to have provided only limited benefits so far.

Respondents to the Commission cited complexity of STS criteria, restrictiveness and cost as more relevant than every benefit apart from the capital treatment STS transactions get via the Liquidity Coverage Ratio (LCR) rules. This though, brings its own issues.

STS securitizations (and only STS securitizations) sit at the bottom of the levels within LCR, meaning banks required to hold assets under the regulation are inherently encouraged to prioritise the covered bond market over securitization.

Any rise up the LCR levels would be a huge step forward for the securitization industry, although few hold out much hope of that happening. But in any case, the Commission decided not to report on this at all, for that was the preserve of the a separate review which is now overdue.

Time is money

So far, this argument has been constructed almost exclusively on the first eight pages of the report. The remaining 19 pages focus mainly on technical problems where there is legal confusion. Forget missing the wood for the trees, this report misses the Amazon for a twig.

The rationale for not tackling the major issues head-on in the report, made throughout, is that due to the pandemic and the war in Ukraine, the Commission needs more time to get a “full picture” of how the regulation is working.

However, this argument has fallen short with market participants. S&P’s head of EMEA specialised finance told GlobalCapital last week that the rating agency has already been able to discern that European securitization has been very resilient since the pandemic.

There is frustration now, but the real issue is how the Commission’s inaction and lethargy impacts the market going forward, the broader financial markets and SMEs in the real economy.

When quantitative tightening eventually comes into force, securitization could and should be a key financing tool for banks to repay the central banks. With regulations as they are, the sector will inevitably fall short. And as the problems on the horizon approach rapidly, for SMEs it will also be important to access the securitization market to solve their funding needs.

It’s crucial that when the moment comes, the securitization market can respond. In its current guise, EUSR is more of a hindrance than a help.