The year 2020 may be looked back on as a transformational one for fiscal co-operation in the EU, with countries going further than would have seemed possible before the coronavirus crisis to pool resources and fund the recovery. Beyond rhetoric, there was no such breakthrough in the Capital Markets Union project, however.

“The coronavirus crisis has injected real urgency into our work to create a Capital Markets Union,” said Valdis Dombrovskis in September at the launch of a new action plan for the project. It contained a range of measures, but did not herald the start of a new era of market-based finance in the bloc.

It is, however, a pivotal time for the CMU, with the EU losing its biggest capital markets hub to a hard Brexit, which is ironic given the Anglo-Saxon drive the project had before the UK’s vote to leave.

Meanwhile, in a reshuffle prompted by the resignation of commissioner Phil Hogan, Dombrovskis has changed portfolios, and new commissioner Mairead McGuinness now takes charge of the CMU, alongside financial services and financial stability. As she settles into her new brief, she confronts a familiar roadblock: important areas of potential integration relevant to the CMU, notably in insolvency and taxation frameworks, are the remit of national governments. The EU is stuck with a lack of harmonisation.

“For wholesale markets, the UK has an established ecosystem with a single set of legal frameworks,” says Pablo Portugal, managing director for advocacy at the Association for Financial Markets in Europe (Afme) in Brussels. “The EU needs to remove impediments to single market integration and create conditions to expand market capacity.”

Nicolas Véron, a senior fellow at Bruegel and at the Peterson Institute for International Economics in Washington, DC, says national issues encompassing insolvency and taxation but also housing finance and pensions “are not going to be moved in any significant way by the Capital Markets Union project. I’m not saying there will never be any more harmonisation or convergence in those areas — that could happen — but that’s not going to happen because of the CMU impulse.”

A breakthrough on national issues is unlikely soon.

Markus Ferber, a member of the European Parliament and a co-ordinator for the European People’s Party in the parliament’s Economic and Monetary Affairs Committee, says in relation to insolvency, “those questions deeply affect corporate and civil law, which means member states are naturally cagey. However, just doing nothing is not an appropriate solution either. It is the Commission’s duty to see what kind of compromises are possible in the [European] Council and then make an appropriate proposal.”

Finance ministries are often thought to be more supportive of insolvency convergence than justice ministries, yet while the former develop CMU strategy, insolvency laws tend to be the competence of the latter. “Insolvency laws are difficult to converge because they reflect legal and social traditions in each country,” says Portugal. “Some countries give priority to secured creditors, while others are considered more employee-friendly. There are fundamental differences in approaches.”

Over the medium-term, and particularly once the implications of Brexit set in, tension may emerge not just over the topic of harmonisation versus national powers, but also over whether the CMU should be sealed off or porous.

The Commission said in September that the project was not an aim in itself, but essential for executing “key economic policy objectives”, including “open strategic autonomy in a post-Brexit and increasingly complex world”.

As the UK is discovering, autonomy and openness can come into conflict in the realm of global trade and business, especially if you are not the biggest gorilla in the room. The EU is seeking to develop its CMU in an era when there are large financial centres in London, New York and Asia: if it comes down to a hard choice, should it seek greater self-sufficiency in an area where it currently relies on London, or focus on maintaining links overseas?

Some in the industry say that the CMU needs to be open, with strong links to the UK and the US, while other firms, particularly in France, would emphasise more the concept of autonomy and building up self-reliance.

“The objective of building the EU’s internal capital markets resources should be pursued alongside the aim of attracting external capital and maintaining connectivity with markets and infrastructures located in other jurisdictions,” says Portugal.

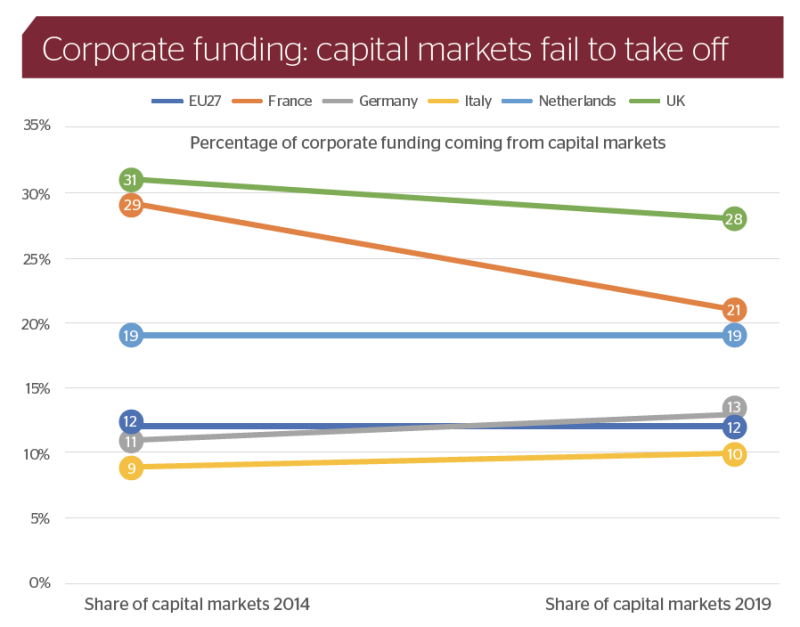

A key idea behind the CMU is broadening out the EU’s bandwidth for financing companies. In this regard, two particular markets stand out: securitization and equity.

Securitization involves packaging up loans and offering them to investors who might not otherwise finance the constituent parts of the package. When lenders offload their loans in this way, it frees up their capacity for new lending.

The new simple, transparent and standardised (STS) securitization framework, in effect since 2019, adds a label to issues that meet certain criteria, giving them a lower capital charge. However, in a report on the CMU in November, the European Court of Auditors said that “the lack of legal clarity, caused by delays in the adoption of secondary legislation and guidelines, negatively affected the STS transactions in the short term”.

It said that while issuance picked up from that level, overall the securitization market did not show signs of growth.

“The potential of the new framework has so far not been fulfilled,” says Portugal. “Part of the reason is that not enough has been done to provide incentives to issuers and investors.”

In the action plan, the Commission said that by the fourth quarter of 2021 it would review the EU’s framework for STS and non-STS securitization. As for equity markets, the action plan said it would try to simplify listing rules, continue its work on creating an IPO fund for small and medium-sized enterprises (SMEs), try to bring about “an appropriate prudential treatment” of long-term equity stakes in SMEs for banks, and propose an “effective and comprehensive” post-trade consolidated tape for equity instruments.

“We need to incentivise the recapitalisation of companies through equity. The crisis is showing how the vast majority of SMEs remain reliant on bank loans for their financing,” says Portugal. “Equity risk capital is very important to financing innovative, high-growth companies.”

He adds: “Part of the challenge of the CMU is to develop a stronger equity culture in parts of the EU.”

What about supervising the EU’s capital markets? In finance, there are three supervisory authorities (ESAs): the European Banking Authority (EBA), the European Insurance and Occupational Pensions Authority (EIOPA), and most importantly for wholesale markets, the European Securities and Markets Authority (ESMA).

“Supervisory architecture is really the central issue in terms of what DG FISMA can do,” says Véron, referring to the directorate-general for financial stability, financial services and the CMU.

ESMA’s board of supervisors is made up of its chair, plus the heads of the national competent authorities responsible for securities regulation and supervision in the countries of the EU and the European Economic Area, and then non-voting representatives from various other bodies.

Ferber says there have been “instances that have raised serious doubts about the independence of the ESAs from their national overlords” and that “changes to the governance and funding model could lead to the ESAs adopting a more European approach”.

ESMA is largely funded through national competent authorities and the EU. However, Véron says that best practice for supervisors is for them to be funded through a fee levied on the industry, with parliamentary oversight. For the purposes of disclosure, Véron points out he is an independent non-executive director of the trade repository arm of the Depository Trust and Clearing Corporation (DTCC), supervised by ESMA.

“To have own resources for ESMA is very important for its future independence,” he says.

Supervision in the balance

However, the ESAs have recently been reviewed and there is scepticism about the utility of re-opening this discussion.

“Supervision is an important but sensitive area as there are different views on the right balance between national competences and direct EU-level supervision,” says Portugal. “It can quickly become the focus of political attention, we fear to the detriment of making progress on other areas.”

Instead, he thinks for the time being the focus should be on other aspects of the CMU, and when it comes to supervision, on convergence of supervisory practices and appropriate application of existing frameworks.

Overall, should we have expected less from the CMU project? The ECA said that while “the launch of the CMU and the communication around this flagship project were perceived by market participants as a substantial commitment by the Commission to induce a significant positive impact,” in fact “the communication on the project raised expectations that were higher than it could realistically achieve with the measures it proposed and that are within its remit”.

Part of the problem appears to be that the Commission has only grouped certain aspects of what actually matters for a capital markets union under the umbrella of the CMU. For instance, as well as issues related to insolvency and taxation, Véron says the CMU has also left out topics related to capital markets infrastructure and financial reporting and accounting. “The Commission from the beginning has adopted a narrow framing of capital markets union,” he says.

The upshot is that it is important to distinguish between progress on the official CMU, and in the broader capital markets in the EU. Unfortunately, at present there is too little in both cases. GC