What’s most likely to get European bank supervisors’ temples bulging and jaws grinding?

It is probably non-performing loans, which they see as clogging up the arteries of the EU’s banking system like cholesterol.

“First, NPLs are a drag on profits, which are too low anyway,” said Danièle Nouy, chair of the European Central Bank’s supervisory board, in a speech on January 24.

“Second, NPLs divert resources that could be used more effectively elsewhere. And third, NPLs weaken trust in banks, and trust is a core asset of every bank.”

But the drive to clean up banks’ balance sheets does not just come from the supervisors: it is from the very top. With politicians wanting further eurozone integration, a European Deposit Insurance Scheme has been talked of for years.

In return for risk mutualisation, northern European countries would like to see greater risk reduction, so that troubled lenders in the south of the continent pose less of a risk to taxpayers in the north. One plank of that is ensuring fewer NPLs on banks’ balance sheets.

It is in this context that European bodies are pushing banks to reduce their NPL levels. The European Central Bank set out qualitative guidance in 2017 and finalised its addendum in March.

The road to legislation

In July the supervisor said it would like banks to achieve the same level of coverage for legacy NPLs as well, but some banks may be given more time than others to do this.

The ECB currently has no legal heft on this matter though.

The original addendum led to angry accusations that it had overstepped its mark in creating policy rather than simply administering it, illustrating the political controversy around the issue.

“Given the absence of legal framework to organise banks’ NPL strategies, the only thing the SSM [the ECB’s Single Supervisory Mechanism] can effectively do at this stage is work on the basis of so-called supervisory expectations,” says Charles-Antoine Dozin, head of capital structuring at Morgan Stanley in London. The body asks banks to draw up their own NPL reduction plans.

The European Commission has presented a proposal for regulation amending capital requirements and implementing minimum coverage levels for new inflows of NPLs.

However, the legal framework is not expected to come into force until 2020.

“In the interim the SSM will have the option to continue having that dialogue with the banks but will have to be a bit more lenient,” says Dozin.

And the European Parliament, when it has its say, is likely to water down the proposals.

“The outcome of the legislative process will probably take more time and might be more lenient than what the SSM would like to see,” says Dozin.

But in the meantime, banks are still looking to sell off assets.

Pushing banks to sell

“The addendum will greatly speed up sales of NPLs in general, and of the unlikely-to-pay loans in particular,” says Vito Ruscigno, co-head of NPLs at PricewaterhouseCoopers in Milan. The unlikely-to-pay term refers to a middle-ranking subset of NPL, where the debtor remains solvent.

Some policymakers have argued that twisting the hand of banks to offload non-performing portfolios quickly may result in bad sales, and instead they should be able to wait until the economy has grown out of trouble. But others argue that this is not a smart solution.

“If not now, when? The economy is doing very well now, but this will not continue forever,” said Nouy in her speech earlier this year. “So banks that do not resolve their NPLs now will carry them forward into the next downturn, when they will grow and become even harder to handle — maybe even too hard.”

And many banks have taken a proactive approach to offloading assets.

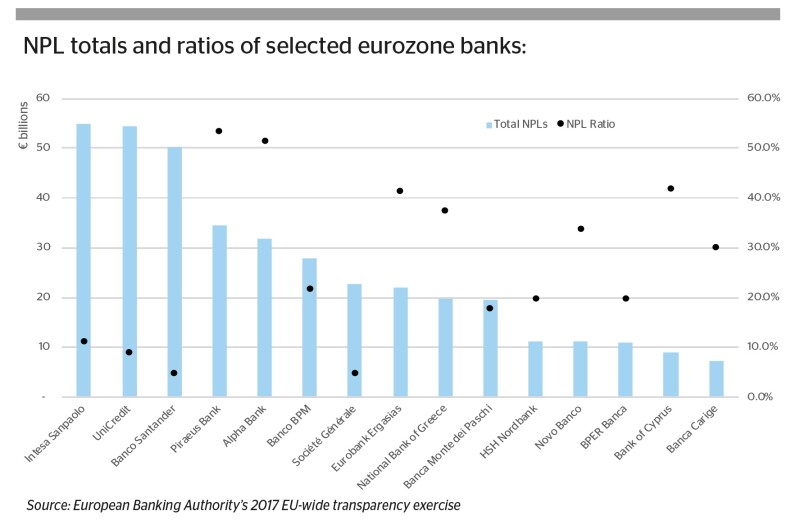

The last 18 months have been notable for large volumes of transactions in Spain and Italy. And now Greece has embarked on the process, with Alpha Bank and the National Bank of Greece both selling multi-billion portfolios of NPLs in individual transactions this year.

While the market started out as one for non-performing loans, banks have also started to sell re-performing assets, as well as ones which have never turned sour but are regarded as surplus to requirements in an age of stricter capital treatment.

“It’s not just an NPL dialogue, it’s much wider,” says Noreen Whyte, CEO of Morgan Stanley Bank International and co-head of its loan solutions group in London.

One reason for banks to dispose of assets is that they have their hands tied when they try to renegotiate customers’ debts.

Those with large loan books do not want to be seen to be giving clients who are not paying bills a favourable deal.

“In many jurisdictions, banks will seek a restructuring solution for problematic customer loans,” says Whyte. “But that process can be especially complicated on high LTV, low-margin and re-performing loans — and runs the risk of contagion across a wider array of loan portfolios.”

In contrast, investors do not face as much contagion risk when taking on the loans, so can more easily reach an agreement with customers to claw back some of the money.

This discrepancy helps to facilitate transactions: the portfolios are inherently more valuable for the buyer than the seller, so it is easier to reach an agreement on price.

It is not hard to make out the drivers behind banks looking to sell assets. But trends in the investor base are also key to their ability to get a better price.

Widening investor base

“There is a wide and ever-widening array of asset buyers coming in” for non-performing and re-performing assets, says Whyte.

Traditional buyers face competition on two fronts. The first is the challenger bank, which acts as a servicing platform with a banking licence. These banks can collect retail funding at a cost of 1%-1.5%

“They have a competitive advantage over the PE funds where the cost of funding is roughly 6%-7%,” says Ruscigno.

The second new entrant is the long-dated investor such as an insurance company or pension fund, interested either in performing or non-performing loans. The low interest rate environment has brought this type of investor into the fold, and the supply of perpetually performing loans has allowed them to avoid taking on excessive risk.

“Previously, insurance companies and pension funds invested cash through private equity funds,” says Ruscigno. “Now they want to invest directly in the market.”

This gives them control and saves management fees.

“Private equity funds will continue to be there but only on the more complex deals where you need creative thinking and speculative lending,” Ruscigno adds. “For the bread and butter NPL deals, challenger banks, pension funds and insurers will play the bigger role.”

And more competition among buyers should benefit the banks selling these assets.

There are other developments. Ruscigno has been approached by two separate funds looking to sell on non-core portfolios they have bought.

“This means first of all that there will be a secondary market starting in Italy, and secondly that investors will be more choosy in terms of what type of deal they want to invest in,” he says. “Being more specialised, they can offer a higher price because they know the product better than the others and so they can extract a higher value from the portfolios.”

In August, Banca Monte dei Paschi di Siena’s sale of €160m of unlikely-to-pay shipping loans demonstrated this specialisation.

SC Lowy, a boutique bank headquartered in Hong Kong, snapped them up, with the deal fronted by its recently acquired Italian bank, Credito di Romagna.

SC Lowy has experience of shipping transactions and beat private equity and investment bank interest to take on the loans.

A specialism allows firms to offer a better deal to sellers.

“If you know something and you understand something well, it allows you to pay a better price,” says Michel Löwy, CEO of the firm in Hong Kong. “If you don’t know the assets really well, you will tend to be more conservative.”

More sophisticated financing options may also boost buyer interest. Investors often purchase secured portfolios on a levered basis.

“As the market has evolved, new financing structures have continued to facilitate an increasing variety of asset sale transactions, which probably wouldn’t have been possible two or three years ago when there were fewer sources of capital and financing options available,” says Jonathan Trup, head of securitization at Morgan Stanley in London.

It is not all smooth sailing for the market, however.

The issue of bad debt in countries ravaged by the crisis brings political confrontation: in Greece, people have stormed the courtroom to protect repossession; in Ireland the Fianna Fail party has pushed to regulate NPL buyers more strictly.

There are other issues. In Italy the slow legal system delays asset seizures. “The length of the Italian legal process is the main factor that affects the price of NPL portfolios for the investors,” says Ruscigno.

Nevertheless, powerful forces in Europe are driving banks’ asset sales, and the investor base is there. Banks will continue to work to unclog those arteries.