With US retailers announcing plans to shutter 4,942 stores across the country during the first quarter of 2017, retail space is being vacated at the fastest rate seen since 2008. That’s got mall owners, and the CMBS lenders that finance them, seriously worried.

Those figures, from recent research notes from real estate services firm JLL, underpin the revolution in US buying habits that is finally catching up with one of the most densely retailed nations on the planet.

With the rise of online and mobile retailing, a generation of consumers are steering away from traditional bricks-and-mortar shopping.

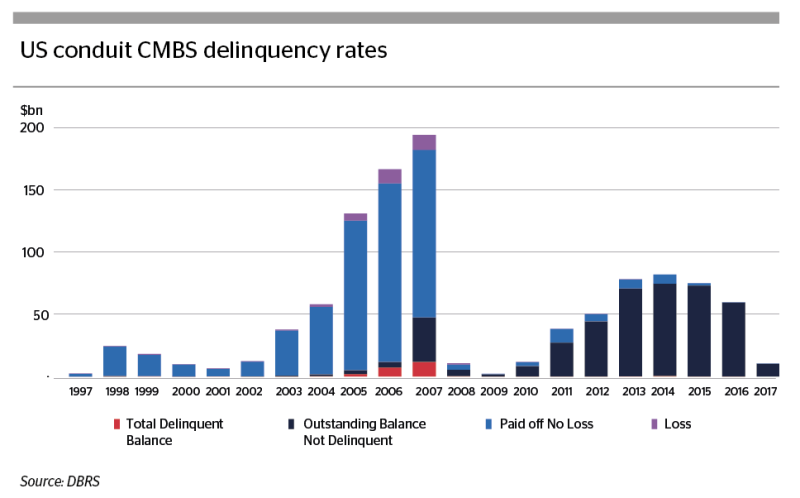

How this plays out in the commercial mortgage backed securities market, which since 2013 has seen an average annual volume of $82bn bonds issued, is contentious.

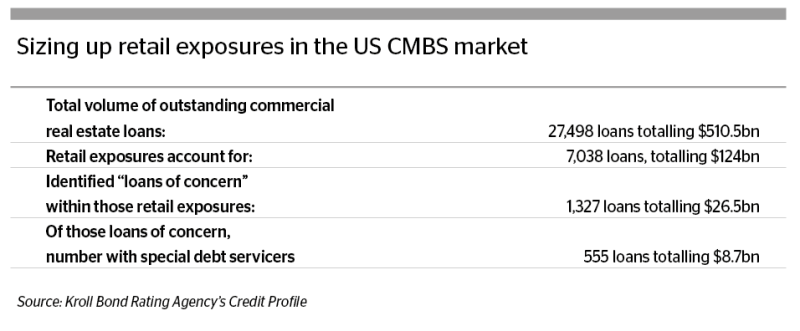

According to data from Kroll rating agency’s Credit Profile product, retail exposures account for roughly 24% of the $510.5bn CMBS universe that the agency surveys — that’s 7,038 loans totalling $124bn.

Of those loans, the agency has identified 1,327 totalling $26.5bn as loans of concern, meaning they are either in default or at heightened risk of default in the near term. While some of those loans may still be repaid, 555 of them totalling $8.7bn are already being worked out with a special debt servicer.

The next Big Short?

These growing pressures have convinced many CMBS players to start shorting the market, via two indices tracking the movement in the price of conduit CMBS bonds issued in 2012 and 2013, which had a higher than average concentration of retail exposure.

The value of the trade is hotly debated. There seems little doubt that weaker malls will struggle in the near term. But analysts disagree on how quickly and how hard this will hit bonds relying on loan repayments from those mall owners.

What is clear however, is that the shake-up in the retail sector will cause a divergence in performance, depending on the underlying circumstances facing each property, stepping up the credit work for CMBS investors.

“It’s fair to say that a good number of CMBS investors are concerned about retail,” says Eric Thompson, senior managing director in structured finance at Kroll in New York. “But some we speak to think it could be overblown to some degree.”

“Undoubtedly there will be some retail credit performance issues, with store closures, but it’s going to be a case-by-case basis. There will be some properties with strong performing retailers that will do just fine,” he says.

Investors are keeping a keen eye on the plans of anchor department store tenants such as Macy’s, Sears and JC Penney. A big concern is that if those anchor tenants pull out of malls, other tenants will follow, leading to a catastrophic domino effect.

Jeffrey Gennette, CEO of Macy’s, warned in the company’s first quarter earnings call in May that the changes facing the retail sector are “secular and not cyclical”. The company announced plans to close around 100 stores out of a total of 730 in August last year.

He said that the US’s saturated retail market was due a correction. “As for the retail industry overall, we’ve known for some time that the United States is over-retailed compared to other markets, so it’s not surprising to see the contraction in retail square footage. And it will take some time to tell how the consolidation and the closure of stores, and in some cases, entire brands will impact us.”

In its 2017 outlook, Green Street Advisors said that malls at the bottom end of the spectrum would certainly struggle, pointing out that 300 ‘C’ class malls are at most risk over the next several years.

But managing director DJ Busch pointed out: “Fortunately, these malls only account for roughly 5% of mall value in the US and most won't be missed.”

Discerning shoppers

The challenge for CMBS investors is to make sure they are exposed to the better quality malls that are still expected to do well. This is largely dependent on key retailers improving their “multichannel” offerings to draw shoppers instore, as well as malls bringing in more food and entertainment offerings to increase the appeal of the shopping destination.

“Retailers are clearly responding to the changing environment, and some have been doing so for several years,” says Larry Kay, director at Kroll in New York, who adds that there has been a “bifurcation” in terms of mall performance.

JLL’s retail outlook for 2017 said that the function of stores would be “redefined” as they react to the challenge of e-commerce.

“Rather than being limited to transactional locations, stores are increasingly serving in a greater capacity as cross-channel fulfilment centres, pick-up stations for online orders, convenient locations for returns, product showrooms and vehicles to boost branding and create buzz. This is clearly illustrated in the number of online retailers opening up physical space, not just to transact sales but to interact with their customers in ways that cannot be replicated online,” the analysts wrote.

Certain segments of the retail sector are also more immune to the challenge posed by e-commerce.

“We’ve seen off-price stores and outlet centres doing fairly well, because they may be less price-sensitive to competition from e-commerce,” says Kay.

But across the board, the sector is underperforming compared to other types of real estate debt. According to a recent default and loss study, the number of annual defaults over the past three years in all commercial property types has been declining, except for retail, where they have been at a fairly constant level.

Focus on office, industrial

The community of conduit CMBS issuers, which bundle a range of different types of commercial real estate assets including retail, office, industrial and hospitality assets into bonds, have taken note.

The proportion of retail loans in conduit deals launched in 2017 is down to around 21%, according to the Kroll analysts. Last year the figure was around 28%, and from 2010 to 2015 it ranged from 25%-50%. “That is indicative of originators being more selective when it comes to the retail sector,” says Thompson.

Investor and originator concerns over retail exposure in conduit CMBS is driving demand for other types of real estate assets.

Industrial assets, such as warehouses, are booming as online retailers hunt for more space to house inventory. And with e-commerce shoppers wanting instant gratification, many are investing in developing fulfilment centres close to major cities in order to facilitate same day delivery.

In their sector outlook, JLL analysts wrote that industrial rents were at record highs, while vacancy rates are at a 17 year low.

Finding pools of those assets is tricky, however.

“Most existing spaces are leased out and new deliveries are hitting the market at steady pre-lease rates. Nationwide, there’s simply little to no industrial product available,” the firm said.

CMBS conduit lenders have increased the proportion of industrial properties in new deals in 2017, up to 6% from the 4% average last year. But the lenders face stiff competition from industrial real estate investment trusts (REITs) that can tap cheaper sources of funding.

Office related debt is taking up the bulk of the slack caused by dwindling retail appetite.

In the first quarter of 2017, office properties accounted for on average nearly half of all collateral pools — the 46% proportion is up significantly from the full year average of 29% in 2016, according to a report from Standard & Poor’s.

This should come with some concern. The rating agency also recently pointed out that maturing office loans have been experiencing the lowest payoff rates in the CMBS market of late, and a large volume of loans coming up for maturity have debt yields below 8%, making them a trickier proposition when it comes to refinancing. Almost half of struggling loans in the CMBS universe that are with special debt servicers — $2.3bn out of $4.3bn — relate to office properties.

“We caution investors to keep their eye on this sector amid the flurry of stories focusing on retail,” wrote S&P analysts in May.

Both sectors are shifting under similar generational pressures, with office spaces evolving according to the differing needs of younger workers. If office building managers don’t stay on trend, credit quality could suffer, say analysts.

“Baby boomers may have wanted a corner office, but millennials can plug in anywhere,” says Kay. “Individual work areas are becoming less about corporate rank and more about functional use. Office properties that aren’t able to adapt to new technology are probably where we’ll see more issues,” he says.

The struggles facing the US retail market may not have the Doomsday effect that hedge fund investors playing the short game would like. Retailers, mall owners and CMBS lenders will adapt. But these long term shifts, as new generations of consumers and workers constitute a bigger proportion of the US economy, will no doubt cause some short term turbulence as markets adjust.