-

Having the last laugh is satisfying — just ask Russia’s Siberian Coal Energy Co (Suek). The firm is on the verge of signing a hugely successful facility after almost all corners of the emerging market loan universe said that the deal would struggle because of its five year tenor — Suek’s third loan of this length since October 2011. The time has come for lenders to accept how things are, rather than grumbling about how they think they should be.

-

Over the last five years I, like many of you, have spent a lot of time engaged in understanding various proposed financial reforms aimed at securitization and preparing industry responses to such proposals.

-

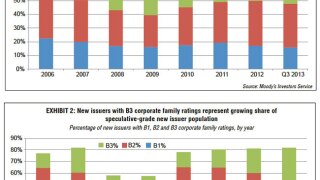

In 2014, the credit quality of new collateralized loan obligations will be strong, characterized by amortization in both the U.S. and Europe and by solid deal structures, a benign macroeconomic environment, and loosening credit in the U.S.

In 2014, the credit quality of new collateralized loan obligations will be strong, characterized by amortization in both the U.S. and Europe and by solid deal structures, a benign macroeconomic environment, and loosening credit in the U.S. -

One lesson the mortgage industry learned during the recent financial turmoil: documentation matters.

-

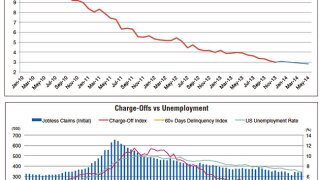

Positive U.S. macro and employment data has finally brought to bear the highly speculated tapering courtesy of the Federal Reserve.

-

Ever since the world’s first rated issuance in 2006, “trade finance securitization” has been a buzzword in the banking industry.

-

The swathe of euro-denominated issuance that has started and is expected to continue in the emerging markets ought to boost the league table positions of some of the European banks that have been breaking into these regions.

-

Conditions for issuing bonds and sukuk in Dubai look great, but mid-way through January there is still barely a glimmer of a deal. Those borrowers that need to come to market this year would do well not to miss their chance.

-

The Luxembourg government’s introduction of a sukuk bill has raised the possibility that it might stump the United Kingdom’s bid to issue the first European sovereign Islamic paper. But rather than causing alarm among UK Islamic finance practitioners, this competition for the limelight should be celebrated as a win-win for the market.