When the Volkswagen emissions scandal broke last September, market participants struggled to understand the impact it would have on auto ABS. But while spreads widened, the scandal did not dent enthusiasm, and 2015 became a record year of issuance for auto ABS across Europe.

Issuers did not shy away from the primary market. Volkswagen came to market in late October with its VCL 22 auto lease deal, offering the top tranche at triple the spread offered for the equivalent notes in its last issue from the shelf. Nevertheless, it raised €820m from the transaction.

As the year came to a close, the primary market showed no sign of slowing down, with a benchmark German lease deal from BMW joining the pipeline. This followed a well subscribed French auto deal from Socram Banque in November, and two successful Scandinavian auto ABS deals from Santander in October and November.

Upbeat agencies

Rating agencies have taken a cautious approach to the sector following the scandal. Their main concern is the impact on residual values, which could reduce the cash that issuers can realise from used vehicles at the end of a lease or loan.

However, with Fitch affirming ratings of 14 VW auto ABS transactions in November, credit concerns are not weighing on the sector. Moody’s is also cautiously upbeat.

“VW is standing behind the problem,” says Anthony Parry, vice president of EMEA ABS at Moody’s in London. “They are in single-A ratings territory, and they are committed to fixing the problem. This is a strong mitigant which, in our central scenario, should protect auto ABS investors from the fallout of the emissions crisis.

“Nonetheless, tail risks remain and so this is something we consider in our analysis.”

More emissions

The asset class remains an appealing funding option for issuers. A Volkswagen spokesperson described the pricing on its VCL 22 deal as “attractive”, and said the company was looking to expand its ABS programme.

“Auto ABS transactions make up a substantial proportion of the diversified refinancing carried out by Volkswagen Financial Services,” he says. “Within the framework of the strategic tripartite funding (money and capital markets, direct bank deposits and auto ABS), we would like to further expand the emission volume of auto ABS in the global arena.”

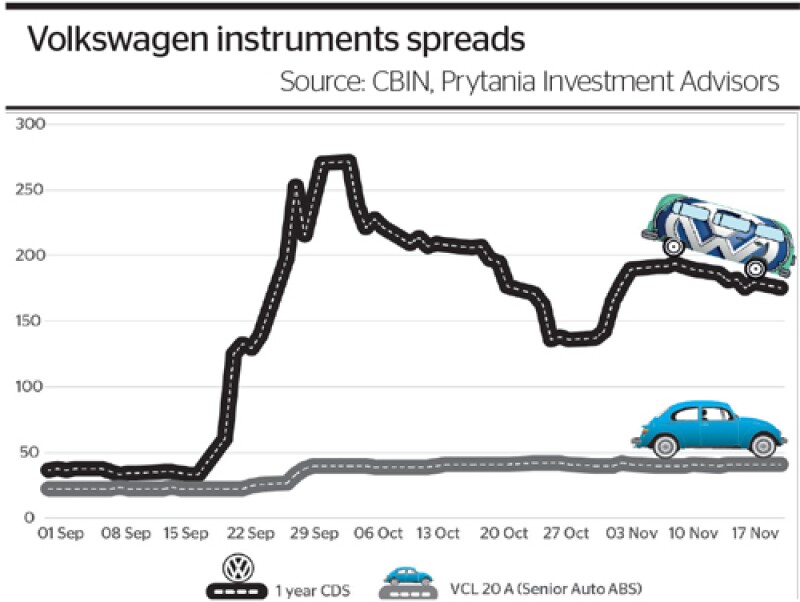

VW has not issued public unsecured debt since the scandal broke. Bankers say this has allowed investors to push ABS pricing wider.

“Any investor looks at what they could be paid,” says Lynn Maxwell, global head of securitization at HSBC in London. “They look at the alternative forms and cost of funding available to the issuer. So in the case of VW, investors see this as an opportunity to pick up some spread on high quality paper, when the company is not issuing other types of debt.”

For issuers, however, the draw of the asset class is about more than just price.

A BMW treasury official tells GlobalCapital that the attractiveness of ABS pricing in comparison to other forms of funding “might differ from jurisdiction to jurisdiction. However, we believe that attractiveness and value is more than just plain pricing”.

The crisis has reaffirmed the role that ABS plays in giving issuers the ability to mitigate the impact of corporate risk on their funding.

This allows companies to access funding when there are headwinds at a corporate level, says Maxwell. “That is one of the reasons why companies have a balance of ABS and unsecured funding. Sometimes, they’ve had to pay quite a premium to stay in the ABS market. But typically they’ve done that because they’ve felt that the diversification is valuable. And it’s at times like this where you really see the value, because they are able to raise liquidity through auto ABS when they are not issuing corporate bonds.”